Sui’s mainnet suffered three separate outages across May 28 and May 29 after the network’s 1.72 release exposed edge cases in gas charging and validator restart logic, according to a postmortem from the Sui Foundation. The foundation said the issues have since been resolved, network activity has resumed, and “no user funds were at risk.”

The incidents began on Thursday, May 28, when Sui’s mainnet halted at around 7 a.m. PT and remained down until roughly 1:30 p.m. PT. A second outage followed on Friday morning, starting at about 5 a.m. PT and ending around 8:30 a.m. PT. The third halt began Friday afternoon at approximately 1:30 p.m. PT and was resolved around 7:20 p.m. PT.

According to the foundation, the first two outages stemmed from crash bugs involving the interaction between gas charging logic and Sui’s 1.72 upgrade, which introduced address balances. The third outage was separate, triggered during a scheduled epoch change after validator restarts exposed a latent bug in how randomness state was preserved.

“During the outages, no user funds were at risk, and the network did not revert any committed transactions when it resumed,” the Sui Foundation said. “As of now, validators have fully addressed the known issues caused by both the original gas-charging bug and the randomness-state bug, and network activity has resumed.”

Sui Gas Charging Bug Triggered Initial Halts

The first problem centered on Sui’s new address balance feature, which allows users to store funds and pay for gas without relying solely on coin objects. Transactions on Sui can pay gas through address balances, coin objects, or a hybrid structure combining both.

The edge case emerged in that hybrid gas path. When a transaction attempted to spend from an address balance that could not cover competing transactions, the scheduler correctly cancelled it with an InsufficientFundsForWithdraw error. But later, during gas smashing — the process of combining input coins into a single gas-paying coin — the same reservation could still attempt to debit funds again.

In the foundation’s explanation, the crash did not occur directly during gas smashing but during settlement, when balance deltas were reconciled by a system transaction. A negative delta applied to a zero balance caused an underflow.

The immediate fix was conceptually straightforward: avoid gas smashing when a transaction is cancelled with InsufficientFundsForWithdraw. Validators adopted that fix on Thursday, bringing the network back online. But the foundation acknowledged that the patch was an interim measure, chosen to restore the network while engineers developed a more complete solution.

“Changing gas logic is a delicate operation,” the foundation wrote. “As explained above, there are complicated interactions between address balances and coins. Other than fixing bugs, gas logic changes must preserve all previous behavior or use appropriate version gating.”

That interim patch contained a known weakness. If a transaction had multiple cancellation reasons, another error could mask the InsufficientFundsForWithdraw condition. When that happened Friday morning, the original underflow path could still be reached, causing a second halt.

Epoch Change Exposed Randomness-State Bug

The third outage came after the network had resumed normal operation Friday morning. At the next scheduled epoch change, validators failed to complete the transition because of a bug tied to Sui’s distributed key generation protocol, or DKG, which bootstraps randomness for transactions that depend on on-chain randomness.

During the earlier restart cycle, participation was not high enough for the next epoch’s DKG process, so randomness was disabled as designed. The problem was that the failure verdict was not written to disk. As validators restarted again, they came back up without remembering that DKG had failed.

“With validators no longer remembering DKG had failed, neither could happen, the paused queue grew, and end-of-epoch logic — which must drain that queue before closing — was left waiting on DKG that would never come,” the foundation said.

The fix had two parts: persisting DKG status across restarts and adding a mechanism that allowed validators to close the stuck epoch at a coordinated point. That mechanism was used once to close the affected epoch, after which the network moved into the next epoch and randomness was restored.

The postmortem framed the outages as a broader engineering lesson for Sui. The foundation said end-of-epoch resilience needs further investment, particularly around graceful degradation and operational force-close mechanisms. It also said gas charging deserves the same level of rigor as the Move VM or Mysticeti consensus, given its interaction with settlement, conservation checks, and scheduling.

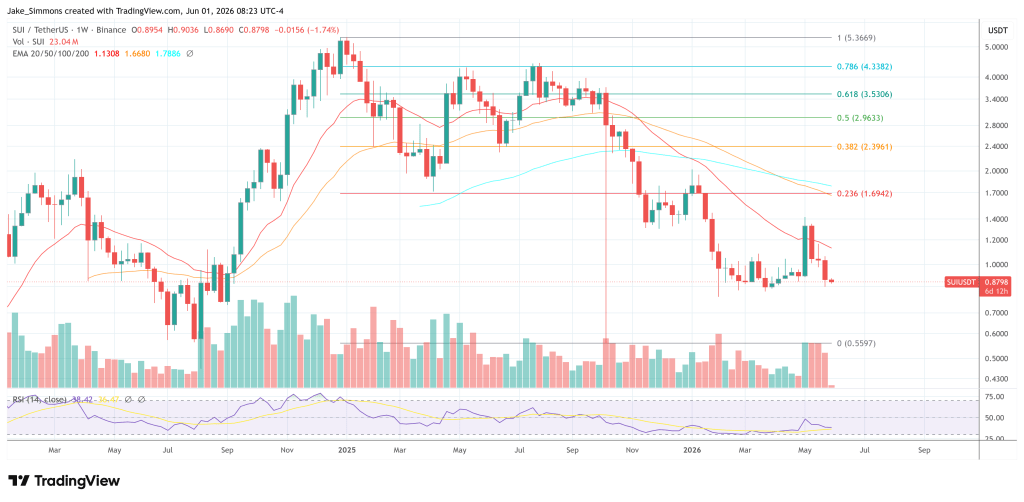

At press time, SUI traded at $0.8798.