While dealing with the Iran war, placing 3,642 orders in a US stock account.

This is Trump's Q1.

At the same time, he was also handling tariffs, negotiating trade deals, and signing executive orders. Last Thursday, a 113-page document was publicly posted on the US Office of Government Ethics website. A handwritten note was on the cover, stating the filer had paid a late fee. The world's most scrutinized transaction disclosure was finally released.

In the same week, the US Congress was advancing bills to ban officials from stock trading. According to Axios, related proposals have garnered support from over 120 lawmakers, with versions in both the Senate and the House, and public support polls exceeding 70%.

But the biggest loophole in these bills is that they don't cover the president.

The White House response is also familiar. The president's assets are managed by his children, trades are executed by account managers, fully compliant with all requirements of the STOCK Act, and no conflicts of interest exist. This statement has been repeated many times over the past year. Every time new details emerge, it's recited again. The repetition itself has become a form of information.

A person who can influence tariffs, trade, industrial subsidies, crypto regulation, and market sentiment, while retaining a massive US stock portfolio.

The disclosure document says the trades are compliant. What the market really wants to see is what he actually bought, how much he made, and whether these stocks are moving in the same direction as his policies.

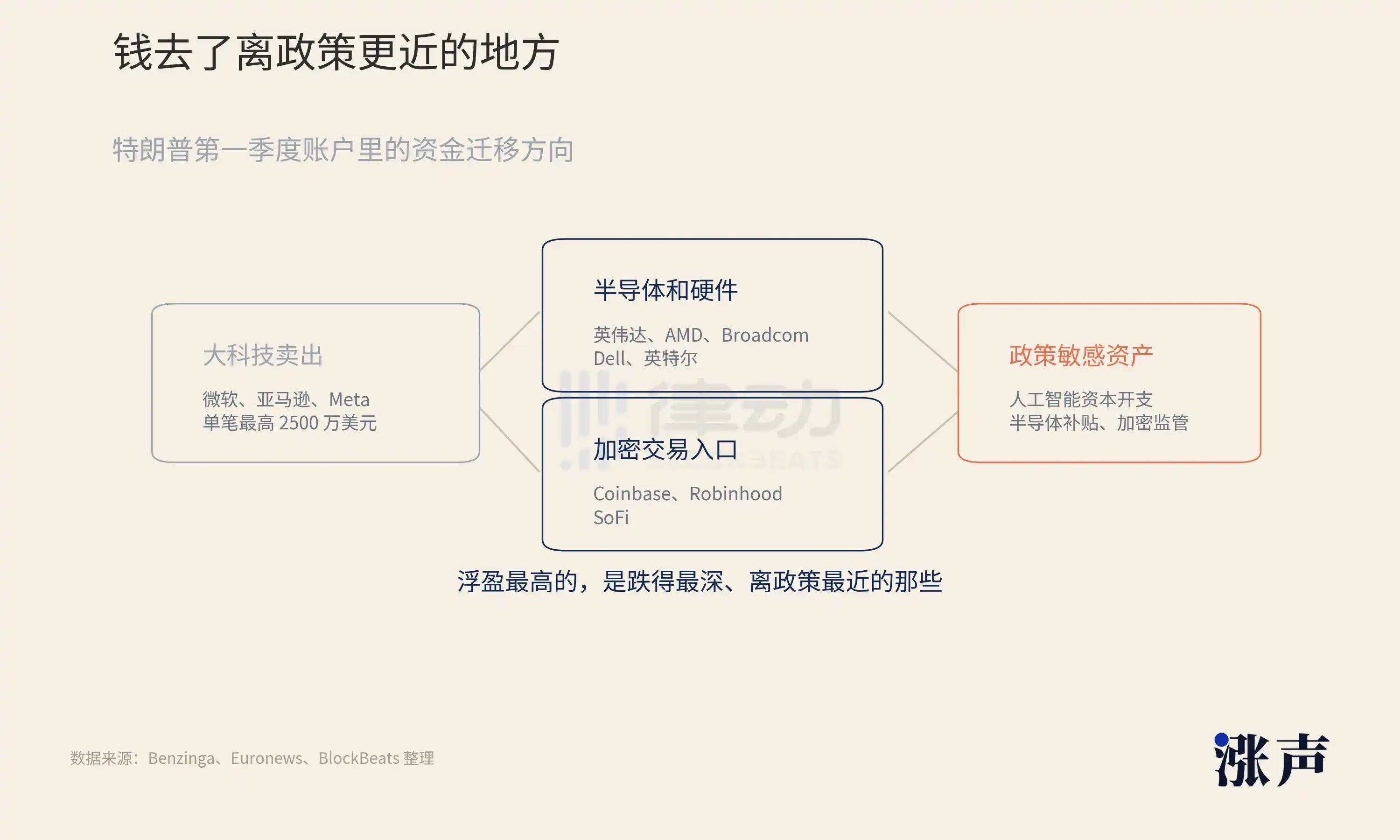

Money Moving Out of Big Tech, Heading Towards Policy-Proximate Areas

Federal disclosure rules only require reporting amount ranges, not exact prices or actual profits/losses.

After page-by-page verification of Trump's scanned document by Benzinga, estimates show NVIDIA purchases of approximately $2.4 million to $6.6 million, Microsoft about $2.4 million to $8.1 million, Amazon about $2.5 million to $8.3 million, and Oracle about $2.2 million to $10.6 million.

For Big Tech, it was a different set of actions.

The largest sell orders were in Microsoft, Amazon, and Meta, with single transactions reaching up to $25 million. For the same batch of companies, holdings were present in the first part of Q1, sold off in the latter part, with buys and sells alternating in the statements. Money moved out of Big Tech and went into the semiconductor and AI hardware supply chain.

NVIDIA, AMD, Broadcom, Dell, and Intel were the most frequently appearing names in this line. Also Coinbase, Robinhood, SoFi. The timing of these positions coincided with the window of federal Bitcoin reserve discussions and the successive announcements of the 'Trump Account' retirement plan.

According to Euronews statistics, if the holdings were maintained until the disclosure date, paper gains exceeding 100% included AMD, Intel, Marvell, SanDisk, Seagate, etc.

The highest paper gains were in those that had fallen the most and were closest to policy.

In this set of trades, Big Tech remains the core holdings. Microsoft has enterprise software and cloud services, Amazon has cloud computing and advertising, Meta has advertising cash flow and AI recommendation efficiency, Oracle has databases and cloud infrastructure. They are the most convenient names when US market funds flow back into risk assets.

The growth is in the hardware chain.

NVIDIA is the center of GPU supply, AMD is the second option, Broadcom makes custom chips and datacenter networking, Dell delivers AI server whole machines. Every additional GPU cloud providers buy, companies on this chain get one more order. Big Tech money bets on the valuation logic of platform companies, hardware chain money bets on the first ones to get paid when AI capital expenditures materialize.

In comparison, Dell is the cleanest timeline case here.

February 10, 2026, the Trump account opened a position in Dell, amount range $1 million to $5 million. May 8, Trump publicly praised Dell's hardware products at a White House event, Dell rose about 12% that day. Six days later, the transaction disclosure came out.

On the same line, there's another background. The Dell family had previously pledged $6.25 billion to the 'Trump Account' retirement plan. Each link, viewed separately, is legal, confirmed by the STOCK Act.

And, no one is under investigation.

This is also what makes the Trump account different from ordinary politician trades. For ordinary officials' stock disclosures, readers look to see if they anticipated a policy direction. Trump's disclosure adds another layer. He's not just placing bets from the sidelines; his public activities, policy initiatives, and industry relationships themselves become part of market pricing.

The Dell timeline is short and complete.

Account buys first, White House speaks later, company stock rises that day, family funds then enter Trump policy projects. It doesn't need to prove any link illegal to be sufficient for the market to treat it as a sample of politician trading.

Intel Bought Into an 'American State-Owned Enterprise'

There is one trade in the US stock portfolio not in Trump's personal account.

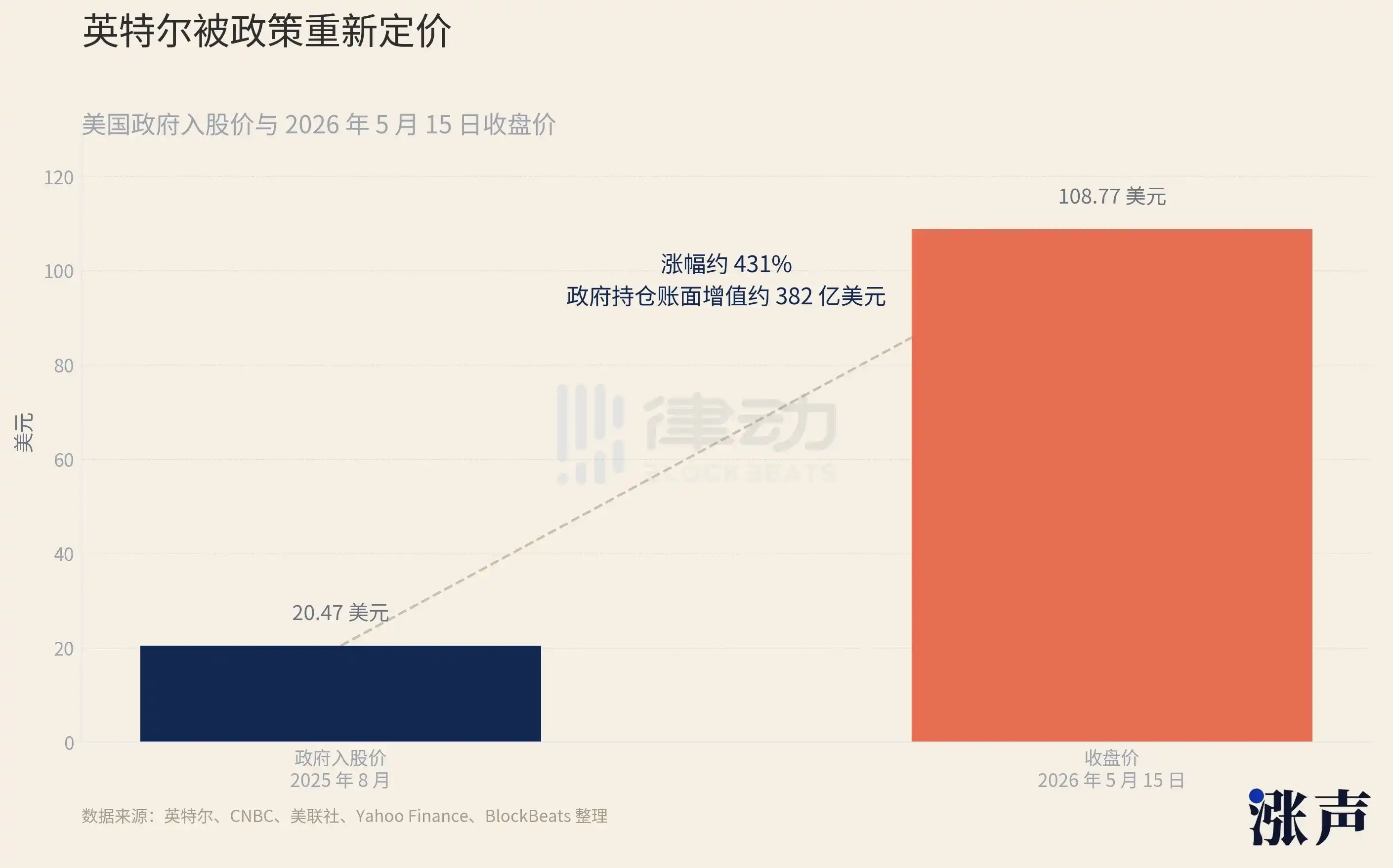

In August 2025, the CHIPS and Science Act still had $5.7 billion in subsidies for Intel unallocated, plus $3.2 billion for the 'Secure Enclave' project, totaling $8.9 billion.

The Trump administration converted this subsidy into equity. 433.3 million shares of Intel common stock at $20.47 per share, acquiring approximately 9.9% equity. The US government became Intel's largest shareholder, officially designated a 'passive investor,' not requesting board seats.

This was a provision not designed into the CHIPS and Science Act. Subsidies were deliberately designed as non-equity forms with a clear purpose. The government gives money but doesn't intervene in governance. Take the money, not the stock. Because with stockholding, the government gains a financial stake in the company's future, making it difficult to remain neutral.

Trump changed the rules.

Before this transaction, Intel's stock had been languishing below $20 for nearly a year, revenue declining persistently, process technology lagging, the market's verdict being a company losing competitiveness. After the government stepped in, a new variable entered Intel's valuation: the US government would not let this company die.

This judgment doesn't fit into a DCF model, but the market prices it.

Chip manufacturing is a national strategy, the largest shareholder won't stand idly by, Intel's tail risk was cut off by policy from this moment. Trump's personal account's Intel position appeared in early March 2026, six months after the government completed the transaction.

By then, Intel had exceeded earnings expectations for six consecutive quarters, AI inference demand drove CPU order recovery, Apple foundry rumors persisted, and the narrative of fundamental recovery began to hold water. By May 15, 2026, Intel closed at $108.77. From the government entry price of $20.47, a gain of about 431%, with the government's stake's paper value increase of about $38.2 billion.

First use taxpayer money to backstop, then follow up with one's own money. This sounds harsh, but the sensitivity of the Intel case lies here.

Public information already exists, Trump's personal account buying Intel may not involve non-public information. The issue is, when the government has already pushed a company to the center of national strategy, the president's personal account appearing next to the same company makes it difficult for the market to see it as just an ordinary investment.

The community calls Intel the 'American state-owned enterprise.' Behind the joke is a very real judgment.

It differs from traditional SOEs, but when the government buys a 9.9% stake with $8.9 billion, Intel is placed within the policy framework of American manufacturing, supply chain security, AI compute sovereignty, and semiconductor subsidies. What investors buy, besides Intel's next quarter profits, is the expectation that the US government won't let it fail.

This is also why Intel is more important than Dell.

Dell is a clear single-stock timeline.

Intel is an institutional timeline. It starts from converting subsidies to equity, linking industrial policy, government financial interest, personal holdings, and market pricing together.

In recent years, the market tracking Pelosi family trades followed only one logic. Policymakers knew something in advance, so they bought early. That's a one-way causality: policy generates information, information brings trading opportunities, officials front-run.

Intel is different. The key here goes beyond knowing a policy in advance; the government itself becomes part of the trade. Subsidies, equity, manufacturing reshoring, AI compute, personal accounts, all converge on the same company.

This case explains why that batch of AI hardware and semiconductor assets in the Trump account is important.

NVIDIA and AMD are compute chips, Broadcom is networking and custom chips, Dell is server whole machines, Intel is the US government personally stepping in to backstop domestic manufacturing.

These targets seem scattered but point in the same direction. The US market is buying AI capital expenditure, the US government is buying domestic semiconductor capability, and the Trump account also appears alongside these assets.

The Closed Loop: Portfolio and Policy Push Each Other Forward

The market has tracked politicians' US stock accounts for many years.

Pelosi family trades have been tracked for years, the logic always simple. The policymakers knew something in advance, so they bought early. Policy generates information, information brings trading opportunities, officials profit from the time lag.

This logic has a legal framework to handle it, for which the STOCK Act was created.

Trump's US stock account adds another layer, and one that's harder to address.

He holds Intel, so he has a financial motive to maintain semiconductor subsidies. He holds Coinbase and Robinhood, so he has a motive to advance crypto legalization. He holds the AI hardware chain, so he has a motive to keep datacenter capital expenditure expanding. He holds broad index funds and Big Tech, so he has a motive to keep overall US market risk appetite high.

The account and policy move in the same direction, the two reinforce each other. Over time, it's hard for outsiders to tell which is pushing which.

Policy influences holdings, holdings in turn influence policy inclination, then policy pushes up holding values. Once this cycle spins up, outsiders find it difficult to judge, on any specific decision, whether financial interests played a role, and how big a role.

Successive presidents insisted on using blind trusts, the core meaning lies here. Money goes in, one doesn't know what is held, so when making policy, there is no financial bias. Severing this feedback loop is a basic assumption of institutional design.

Trump doesn't have this system.

The CHIPS Act initially designed subsidies as non-equity precisely to prevent the government from becoming a shareholder and losing neutrality. Trump changed it to equity, the government took 9.9%. Six months later, his own account also entered Intel. Now, the direction of semiconductor subsidy policy and the market value of his two accounts point in the same direction.

The STOCK Act regulates officials trading on non-public inside information.

Most information here is public. The problem is, when decision-making power and financial interests are tied to the same person, current rules have no means to constrain this bundling, only requiring him to report the results.

On April 9, 2025, he posted that now is a great time to buy. Less than four hours later, Trump announced a tariff pause, the S&P 500 rose 9.5%. Washington University law professor Kathleen Clark later said, 'He's sending a signal that he can blatantly manipulate the markets.'

One year later, the account comes out.

The Dell family put $6.25 billion into the 'Trump Account,' Trump opened a Dell position in Q1, publicly endorsed Dell from the White House in Q2, Dell rose about 12% that day, six days later transaction records entered the public file.

Everyone on this chain got what they wanted.

The market got a story to explain the stock price. The company got exposure from the White House. The Trump account got paper gains. The policy project got corporate family funds.

The 113-page disclosure document can tell you what he bought. What it doesn't tell you is: policy influences holdings, and holdings, in turn, influence policy.