Author: Claude, Deep Tide TechFlow

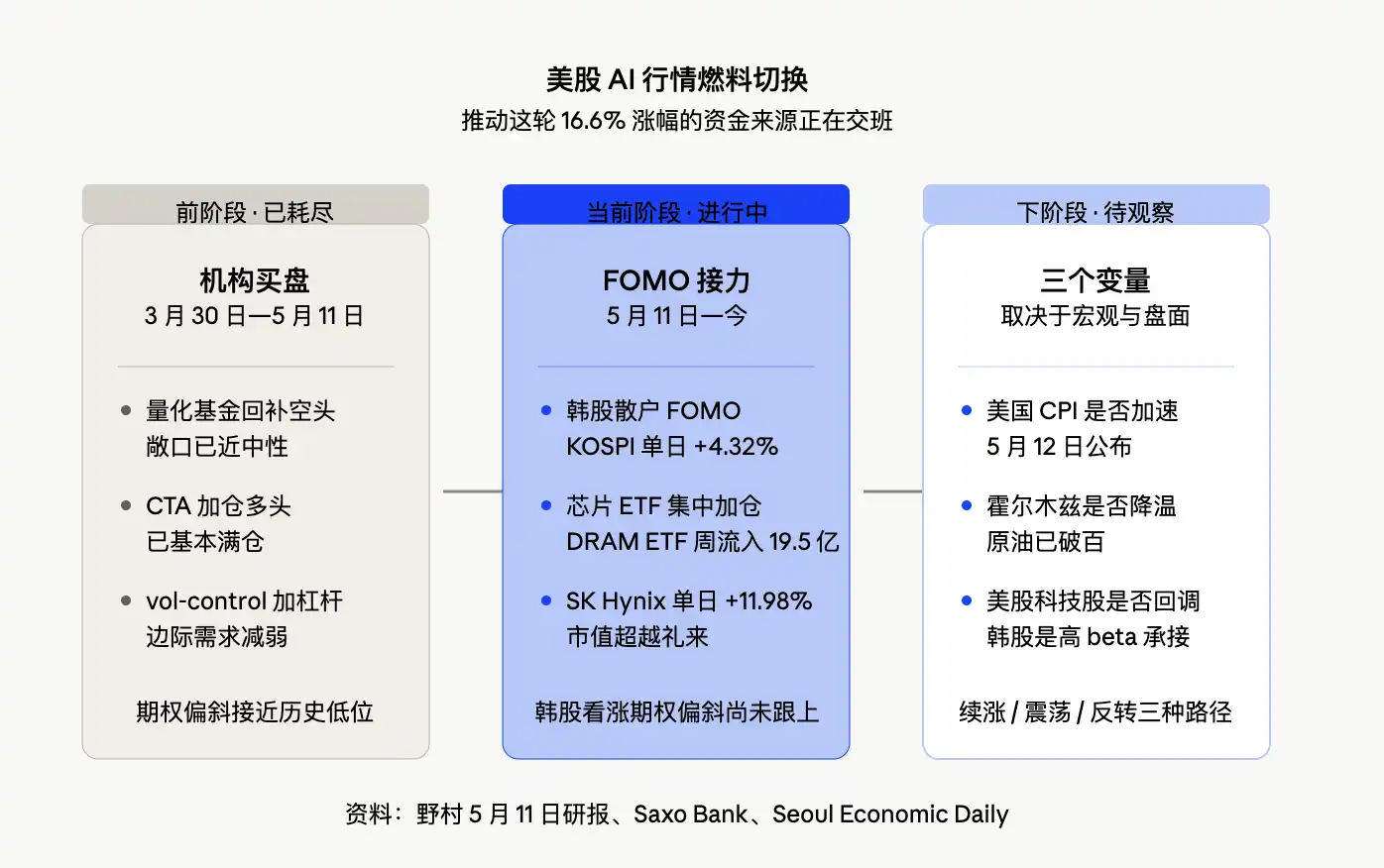

Deep Tide Introduction: A key judgment in Nomura's May 11th research report stated: "At least for U.S. stocks, the AI rally may be taking a breather." On the very same day, the KOSPI surged 4.32% in a single day to 7822.24 points, triggering a buy-side sidecar during the session. SK Hynix soared 11.98%, with its market cap surpassing Eli Lilly for the first time, becoming the 14th largest globally. The report's call that "the next leg depends on Korean FOMO" occurred almost simultaneously with the Korean stock surge. The driving force behind the U.S. stock AI trade is shifting from a "short squeeze" to "retail FOMO."

The U.S. stock AI rally is not over. The S&P 500 accumulated gains of about 16.6% over 28 trading days. However, the source of the funds lifting the index and the remaining fuel for the rally are undergoing subtle changes. Nomura's assessment is that the phase driven by short covering and institutional positioning is nearing its end. For the AI trade to continue, a new wave of capital must take the baton. The Korean market provided a sample case on the very day the report was released, with the KOSPI crossing the 7000, 7400, and 7800 levels within a week, retail investors falling into "hynix FOMO," and foreign capital concentrating on chip stocks via DRAM ETFs. The narrative is shifting from the Nasdaq to the KOSPI.

U.S. Stocks Appear Normal, But the Anomalous "Spot Up/Volatility Also Up" Combo is Flashing

The surface readings of the U.S. stock AI trade remain strong. Saxo's options briefing on May 11th showed the VIX closing at 17.19, up 0.64% for the day. This level is below its historical average, but the VIX rising while the index hits record highs is itself an anomalous signal. The CBOE SKEW Index rose to 138.21 (+1.54%), the VVIX (measuring VIX volatility) rose to 96.78 (+3.39%). The simultaneous rise of these three indicators suggests institutional investors have not abandoned hedging even as the index hits new highs.

Nomura's May 11th report described this combination as an "anomalous state" for U.S. tech stocks. The report noted the Nasdaq exhibited a pattern of "spot prices rising, but volatility also rising," with the VIX continuing its decline while the VXN (Nasdaq volatility) rebounded noticeably. The option skew for U.S. tech stocks (the difference between the implied volatility of 1-month 25-delta puts and 25-delta calls) has rapidly fallen to near historical lows, back to levels around October 2025. A declining skew means the premium for put protection relative to calls has been compressed, indicating more crowded pricing for tech stock upside.

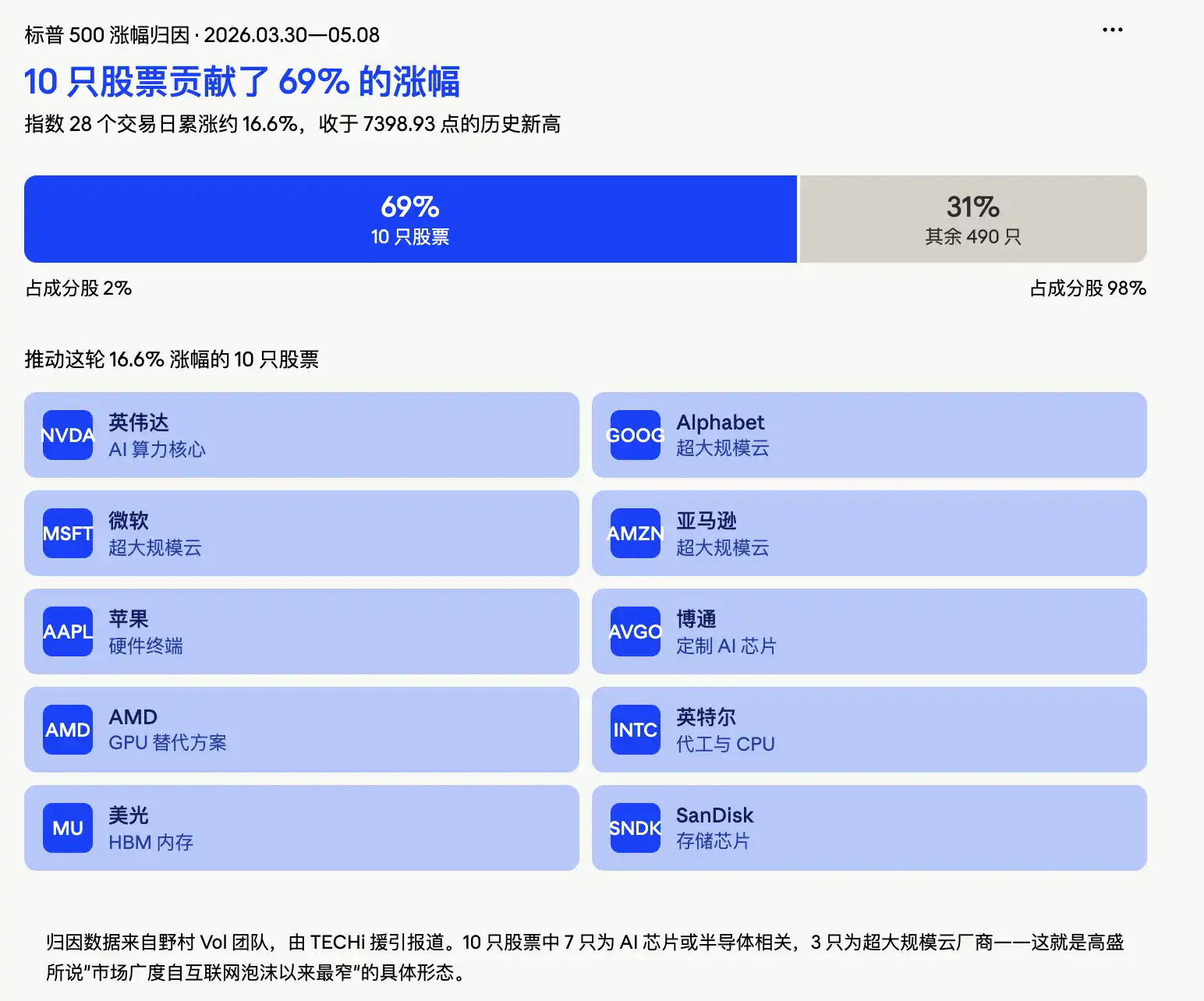

More concerning is the structure of this rally. According to a return attribution chart from Nomura's Vol team cited by TECHi, of the S&P 500's roughly 16% gain since March 30th, 10 stocks contributed 69%: Alphabet, Nvidia, Amazon, Broadcom, Intel, Micron, Apple, AMD, Microsoft, SanDisk. The remaining 490 constituents contributed only 31%. Goldman Sachs' U.S. equity strategy chief Ben Snider also pointed out that current market breadth has fallen to one of the narrowest levels since the dot-com bubble era. Goldman lists "AI Megaprojects" and "Iran Conflict" as the two clearest stock market risks for the coming weeks.

The Shorts Have Been Squeezed Out, Who Will Push the Next Leg?

The real killer judgment in Nomura's report isn't the "anomalous combo" itself, but its dissection of fund flows: Quant funds' equity exposure has recovered to near neutral, and the process of forced buying and short covering is largely complete. CTA (Commodity Trading Advisor) funds have largely returned to full long positions, and the marginal incremental demand from volatility control strategies is also waning.

In other words, the three main buying forces that drove AI stocks higher in recent weeks—shorts being squeezed, CTAs adding positions, and declining volatility prompting vol-control funds to add leverage—are all nearing their limits. If AI stocks are to continue rising, they can no longer primarily rely on the "short squeeze" buying force.

It's important to note that Nomura's estimates of quant fund, CTA, and macro fund positioning are based on model calculations, not actual measured holdings. This makes them better suited as a temperature gauge for marginal changes rather than a precise positioning table. Even so, the direction is clear: Programmatic buying from the institutional side is nearing its limits, and subsequent upward momentum must rely more on retail and sentiment-driven capital.

Goldman's trading desk largely agrees with Nomura's assessment. Goldman's One-Delta trading desk head Rich Privorotsky recently described the current pace as "semi-irrational chasing," drawing a comparison to 1999, when overflowing telecom equipment orders provided a "physical bottleneck narrative," similar to the current logic of AI compute scarcity. Goldman's volatility trading desk characterized recent dynamics as "spot up, volatility up," which limits the space for systematic strategies to add further positions.

This assessment means the U.S. stock AI trade isn't breaking, but the script of "pushing higher by squeezing shorts" is nearing its end.

Korean Stocks Provide the Answer: On the Day of Nomura's Report, KOSPI Surges 4.32%, Triggering Buy-Side Sidecar

Another judgment in Nomura's report was: For the AI trade to have another leg, the true signal for continuation would be to watch for a resurgence of FOMO in Korea.

The Korean market responded with an extreme outburst on the very day the report was released. The KOSPI closed at 7822.24 points, up 4.32% for the day, touching 7899.32 points during the session, which triggered a buy-side sidecar. SK Hynix surged 11.98% to 1.888 million KRW, with its market cap surpassing Eli Lilly for the first time to become the 14th largest globally. Samsung Electronics rose 6.33% to 285,500 KRW. The combined market cap of the two companies exceeded 3,000 trillion KRW, accounting for nearly half of the KOSPI's total market cap. The combined market cap of the Korean stock market (KOSPI and KOSDAQ) exceeded 7,000 trillion KRW for the first time, just 8 trading days after breaking 6,000 trillion KRW on October 27th.

During the May 12th session, the KOSPI further broke above 3900 points (the 7900-point level), setting another new all-time high. However, data from the same day revealed the other side of FOMO: Of the 948 stocks on the KOSPI, only 186 rose while 696 fell; approximately 30% of the index constituents have fallen year-to-date. Gains were entirely concentrated in the two semiconductor heavyweights, Samsung and SK Hynix.

A retail FOMO has already spawned new market vocabulary. Korean financial media uses "hynix FOMO" to describe the psychological divide among retail investors: on one side, the regret of missing out ("I should have bought at 800,000 KRW"), and on the other, the anxiety of "should I jump in now?" and "a correction is coming soon." Retail communities are flooded with discussions about "Samjeon-nix" (a portmanteau of Samsung + Hynix). This is a typical retail-driven chasing pattern, highly consistent with the "FOMO signal" Nomura defined.

The flow of foreign capital is even more telling. According to a Seoul Economic Daily report on May 10th, the iShares MSCI Korea ETF (EWY) saw net outflows of $1.0145 billion between May 1st and 7th, a signal of passive fund withdrawal from the Korean market. However, during the same period, the Roundhill Active DRAM ETF saw net inflows of $1.9538 billion. This ETF has a 25.94% weighting in SK Hynix and 21.62% in Samsung Electronics, totaling about 48%. Foreign capital isn't selling Korea, they are selling broad-based ETFs and buying chips, a precise overweighting of the AI theme.

One detail warrants caution. Nomura's May 11th report pointed out that the KOSPI 200 also showed "spot up, volatility up," but the call skew didn't rise alongside it. This doesn't look like volatility expansion driven by call-buying chase demand. In other words, as of the report's release, the Korean market had not yet entered a typical "fear of missing out, scrambling for calls" state. Whether this signal reverses quickly after the KOSPI's surge that day will be key to judging the sustainability of the FOMO.

Korean Stocks are an Extension of the U.S. AI Capex Chain; How Long the Next Leg Lasts Depends on the "Pyramid's Apex"

The Korean FOMO is not an isolated event; it's essentially a high-beta extension of the U.S. stock AI capital expenditure story.

Data directly anchors this transmission chain. According to Bridgewater estimates, Alphabet, Amazon, Meta, and Microsoft are projected to collectively invest around $650 billion in AI-related infrastructure in 2026. Goldman Sachs cites data showing that the consensus estimate for the largest cloud infrastructure companies' 2026 capex jumped by $130 billion last quarter to $670 billion, equivalent to over 90% of these companies' projected operating cash flow. Microsoft's Q3 capex reached $31.9 billion, Alphabet's Q1 property and equipment purchases were $35.7 billion, and Meta raised its 2026 capex guidance to a range of $125-145 billion.

This money flows into data centers, GPUs, memory, networking, power systems, and cloud capacity. SK Hynix and Samsung sit at the core of this money flow, with HBM4 memory and high-bandwidth memory being snapped up by hyperscale cloud providers. According to a Reuters report, SK Hynix recently received "unprecedented" order proposals from major tech companies, with some customers proactively offering to help finance new production lines and ASML lithography machines. Chip capacity is essentially sold out. This is why the KOSPI's single-day 4.32% surge is narratively coherent—Korean stocks are essentially the "second derivative" of the U.S. AI story.

But this linkage also implies vulnerability. If U.S. tech stocks experience a full-scale reversal, Korean stocks would be the most direct high-beta asset to bear the selling pressure. Another risk path mentioned by Nomura is a resurgence of inflation forcing global central banks to be more hawkish. This week's (May 12th) U.S. CPI is a key event, yet the premium in options markets for this event remains low; the market hasn't paid a high insurance premium for this risk yet.

There's one more variable in the macro backdrop: The Strait of Hormuz. WTI crude closed at $100.09 on May 8th (+4.89%), Brent crude at $105.66 (+4.31%). Conflict near the Strait of Hormuz continues to escalate. Nomura's judgment is: As long as the Strait remains obstructed and the U.S. and Iran remain divided on ceasefire terms, the AI-dominated market environment may last longer than expected. Energy price shocks will lift inflation expectations but could also make the market even more reluctant to leave "the AI story that's making money."

Layering these clues together: The phase of the U.S. stock AI rally driven by "squeezing shorts" is nearing its end. Korean FOMO has been ignited, with retail and foreign chip ETFs adding positions in sync, but the option skew hasn't caught up yet. How long the next leg lasts depends on whether U.S. tech stocks correct, whether U.S. CPI signals accelerating inflation, and whether the Strait of Hormuz ultimately cools down. Nomura's report's judgment framework is being validated one by one by market action. Seoul is becoming the latest epicenter of this AI trade.