Written by: Cointelegraph

Compiled by: AididiaoJP, Foresight News

The CLARITY Act proposes a clear division of functions between the U.S. Securities and Exchange Commission (SEC) and the Commodity Futures Trading Commission (CFTC), aiming to clarify how digital assets, exchanges, information disclosure, and regulation should operate within the U.S. cryptocurrency market.

Key Points

- Clarifying Definitions and Division of Labor: The bill aims to resolve years of regulatory ambiguity with a structured framework, defining what constitutes a digital asset, the roles of intermediaries, and the information that needs to be disclosed.

- CFTC and SEC Each Have Their Own Responsibilities: The spot trading of most qualified tokens will fall under CFTC regulation, while the SEC will continue to oversee primary market issuance, information disclosure, and investor protection.

- Regulating Both Assets and Behavior: The bill focuses not only on the assets themselves but also on standardizing market behavior, establishing registration and conduct standards for exchanges, brokers, and dealers to enhance market integrity and transparency.

- Complementary to the Stablecoin Act: Stablecoins are primarily governed by the GENIUS Act; the CLARITY Act only plays a supplementary role in related areas, such as information disclosure and reward functions involving stablecoin use.

The CLARITY Act (Digital Asset Market Clarity Act of 2025) attempts to break the legislative deadlock in the industry through a dual approach: on one hand, clearly defining digital assets, and on the other, allocating regulatory authority based on their actual functions in the market. This legislation seeks to shift from a model of case-by-case enforcement to providing a comprehensive framework for asset classification, intermediary roles, and mandatory information disclosure.

This article will explain what the CLARITY Act is and why it is important, outline its objectives, and explore how it intends to regulate stablecoins. It will also cover the concept of a mature blockchain, the main arguments against the bill, and its legislative progress.

Why the CLARITY Act is Important

The CLARITY Act addresses a long-standing problem in the crypto space: regulatory uncertainty.

For years, digital asset companies have faced the dilemma of unclear jurisdiction between the SEC and the CFTC. The SEC often treats many tokens as securities, while the CFTC classifies them as commodities. This gray area has slowed the pace of innovation, complicated compliance efforts, confused investors, and caused significant trouble for crypto businesses.

The goal of the CLARITY Act is to break this deadlock by clearly defining digital assets and allocating regulatory responsibility based on asset type and related activities. With a preset, clear framework, market participants will know from the outset which rules to comply with, rather than facing the uncertainty brought by reactive enforcement actions.

Main Objectives of the CLARITY Act

The bill primarily establishes the relevant regulatory system in the following three ways:

More Precise Definition of Asset Classes

The CLARITY Act introduces the concept of a "digital commodity," referring to digital assets whose value primarily derives from the use of their underlying blockchain system. This definition excludes traditional securities and stablecoins. As a result, the spot trading of many eligible tokens will fall under CFTC regulation. Considering the actual operation of crypto networks, this definition particularly emphasizes the functionality of the blockchain and the degree of network decentralization.

Clarifying Regulatory Boundaries

The bill divides regulatory authority by function:

- The CFTC gains primary authority over digital commodity trading, particularly in secondary markets, spot markets, and on trading platforms.

- The SEC retains authority over primary market issuance, investor protection, necessary information disclosure, and initial sales.

- The bill also encourages the two agencies to jointly formulate rules in overlapping areas such as information disclosure.

Establishing Unified Information Disclosure and Conduct Standards

To protect investors and maintain market fairness, the bill requires developers and issuers to provide standardized information. This information needs to cover the technical details of the blockchain, the token economic model, and major risks, allowing market participants to have comparable information to evaluate different projects. Intermediaries such as digital commodity exchanges, brokers, and dealers also need to meet registration, reporting, and regulatory requirements, with trading-related activities primarily overseen by the CFTC.

In summary, the CLARITY Act attempts to replace ambiguity with clear rules, supporting industry innovation while protecting investors and maintaining market integrity.

The debate over cryptocurrency market structure is influencing policymakers' thinking on how to regulate AI models, as both involve issues of difficult-to-define liability and rapid iterative innovation.

How the CLARITY Act Regulates Stablecoins

The GENIUS Act, passed in 2025, has already established a federal regulatory framework for payment stablecoins. It stipulates that eligible stablecoins, provided they meet strict reserve, redemption, and regulatory requirements, are not classified as securities or commodities.

The CLARITY Act will not cover or duplicate this stablecoin regulatory system. Instead, its provisions only play a supplementary role, particularly concerning rewards related to stablecoins, information disclosure, and how they interact with the broader digital asset market.

Regarding "Mature" Blockchains

Acknowledging that assets can evolve, the CLARITY Act sets a path for a blockchain to be recognized as "mature" once it meets certain decentralization and other functional criteria.

Once the "mature" standard is met, the associated tokens will transition to being considered "digital commodities," falling under CFTC regulation. As long as the project meets other conditions, this can significantly reduce its regulatory burden, for example, potentially eliminating the need for registration.

The concept of a "mature blockchain" reflects the idea that as networks become more decentralized and widely distributed, the regulatory approach should adjust accordingly. It provides projects with a clearer path to potentially lighter compliance requirements in the future.

In past regulatory disputes, courts have sometimes cited decades-old securities law precedents to judge the nature of crypto tokens, highlighting how existing legal frameworks have been awkwardly applied to entirely new digital markets.

Ongoing Criticism of the CLARITY Act

Although the bill aims to provide clarity, skepticism remains. Critics argue that its definitions may still have loopholes, especially in the decentralized finance (DeFi) space, as these projects are often difficult to fit into traditional regulatory models.

Others argue that the investor protection offered by the bill falls short of existing securities law standards. Other concerns focus on potential jurisdictional overlaps, such as how the SEC's anti-fraud powers will apply in areas primarily overseen by the CFTC, especially for tokens that possess multiple characteristics.

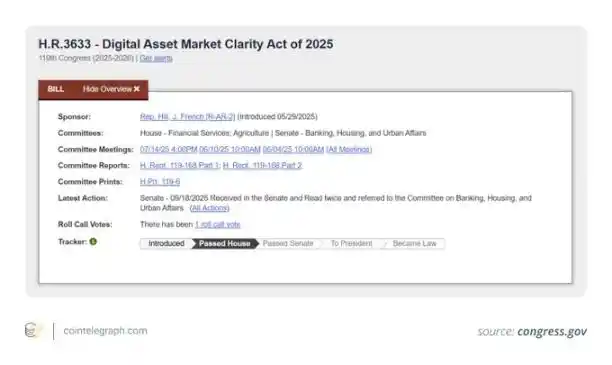

Legislative Progress of the CLARITY Act

The U.S. House of Representatives passed the CLARITY Act (H.R. 3633) with bipartisan support in July 2025. As of January 2026, the bill is awaiting action in the Senate, where it has been referred to the Senate Committee on Banking, Housing, and Urban Affairs for consideration. The legislative process also involves the Senate Committee on Agriculture, Nutrition, and Forestry providing input on matters related to CFTC regulation.

As of January 2026, relevant Senate committees have held hearings, released discussion drafts, proposed amendments, and advanced some versions of broader market structure legislation. However, due to disputes over issues such as stablecoin yields and investor protection, the work of revising and perfecting the bill has faced delays and adjustments. Coordination between the Senate draft and the House-passed bill is ongoing, and the Senate has not yet held a final vote.

If ultimately passed in a coordinated form, the CLARITY Act would become the first comprehensive federal legal framework for the digital asset market structure in the United States.

Some blockchain networks now publish real-time transparency dashboards showing validator concentration, token circulation speed, and governance participation. Regulators sometimes refer to this data when discussing whether a network is "sufficiently decentralized."

Perspective on the CLARITY Act's Blueprint

At its core, the CLARITY Act aims to solve a persistent problem in the crypto field: unclear regulatory boundaries, which have hindered innovation and led to reactive enforcement rather than proactive compliance.

By clarifying asset classes, mandating unified information disclosure, and delineating the分工 between the SEC and CFTC, the bill seeks to create a more predictable regulatory environment where market participants know from the start which rules they need to follow.

Of course, legislation is only the first step. Subsequent implementation, the formulation of specific rules, and potential future adjustments will be key to determining the actual effectiveness of the CLARITY Act. Whether it ultimately delivers the promised clarity will profoundly impact the direction of U.S. crypto policy and industry competitiveness in the coming years.