On March 24, the New York Stock Exchange announced the signing of a memorandum of understanding with tokenization platform Securitize to jointly develop a digital trading platform for tokenized securities. Just six days earlier, the SEC had approved Nasdaq's rule amendments to trade Russell 1000 component stocks and major index ETFs in tokenized form. The two largest stock exchanges in the United States each unveiled their own tokenization plans within the same month.

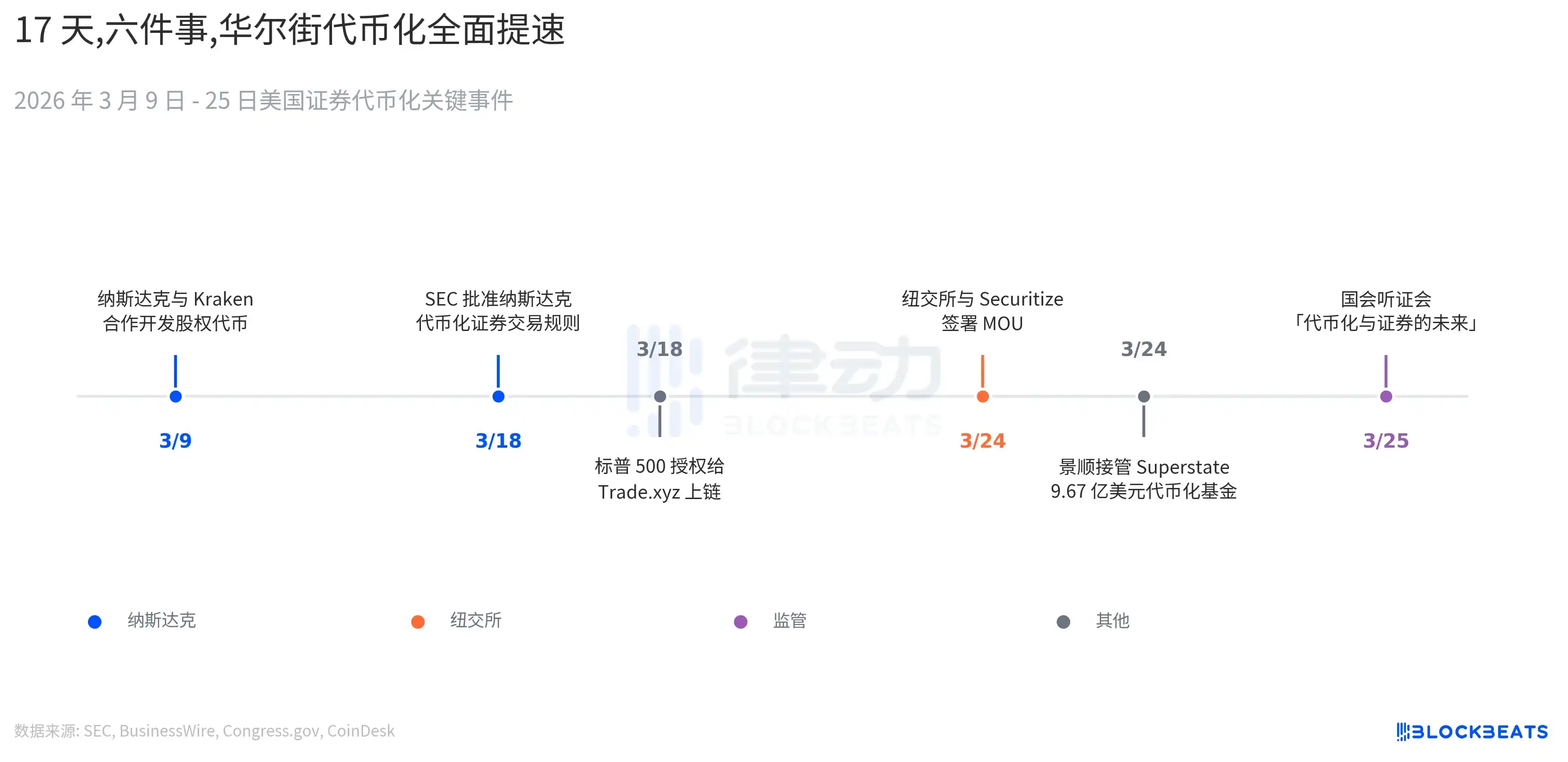

This is not an isolated move by one or two institutions. Spreading out the calendar for March reveals a rare density of activity.

On March 9, Nasdaq partnered with Payward, the parent company of crypto exchange Kraken, planning to provide a distribution channel for tokenized stocks to non-U.S. users. On March 18, the SEC approved Nasdaq's rule amendments; on the same day, S&P Dow Jones Indices licensed its flagship S&P 500 index to the on-chain protocol Trade.xyz to issue perpetual contracts on the decentralized derivatives platform Hyperliquid.

On March 24, the NYSE signed with Securitize; on the same day, Invesco, which manages $2.2 trillion in assets, announced it would take over the USTB fund from on-chain treasury management company Superstate, with a size of $967 million. On March 25, the U.S. House Financial Services Committee held a special hearing, "Tokenization and the Future of Securities: Modernizing Our Capital Markets." According to FinTech Weekly, attendees included Kenneth Bentsen Jr., CEO of the Securities Industry and Financial Markets Association (SIFMA), and Summer Mersinger, CEO of the Blockchain Association.

Six events in 17 days. Two major exchanges, three traditional asset management firms, one SEC approval, one congressional hearing. Among these events, the plans of Nasdaq and the NYSE are the most worthy of closer examination. The two are following different technical paths, and the divergence is greater than most realize.

Nasdaq is taking a compatibility route. According to the approval document (34-105047) released by the SEC on March 18, Nasdaq's tokenized securities trading will still be settled through the existing clearing system of the Depository Trust Company (DTC). Traders select a tokenized asset when placing an order, specify the blockchain and wallet address, and the DTC handles verification and settlement on the backend. Tokenized shares share the same CUSIP number as traditional shares, are matched on the same order book, and have identical execution priority. If the DTC determines that a participant is ineligible or the specified blockchain is incompatible, the transaction is automatically reverted to traditional settlement methods. In this setup, the blockchain is an optional wrapper; the underlying clearing pipeline remains unchanged. According to an analysis by the legal website Free Writings & Perspectives, eligible assets include Russell 1000 index components and ETFs tracking the S&P 500 and Nasdaq 100. The first tokenized trades are expected to launch in the third quarter of 2026.

The NYSE is taking a different path. According to a BusinessWire press release, the NYSE has designated Securitize as its first "Digital Transfer Agent," responsible for minting blockchain-native securities on-chain, maintaining ownership records, and handling corporate actions like dividends. According to CoinDesk, the NYSE is collaborating with Bank of New York Mellon and Citigroup to integrate tokenized deposits and stablecoin payments, aiming to enable 24/7 trading and near-instant settlement. This path is not about adding a layer on top of the existing clearing pipeline but about building an independent on-chain settlement infrastructure. The wording of Lynn Martin, President of NYSE Group, in the press release skipped "exploring" and "piloting," directly stating that the development of the new infrastructure must "preserve the trust, transparency, and protection that investors expect."

The core of the divergence is this: Nasdaq is adding functionality to its existing order book, maintaining unified liquidity, and can launch once the DTC updates its systems. The NYSE is building a separate digital trading platform that will run in parallel with the existing exchange, prioritizing 24/7 trading and instant settlement, though a specific launch date has not been announced according to CoinDesk. Securitize is the core technical support for the NYSE's plan. According to PRNewswire data, it currently manages approximately $4.6 billion, representing about 25% of the tokenized RWA market share.

It is also the technology provider for BlackRock's BUIDL fund. According to public data, BUIDL reached a size of $2.38 billion within 15 months of launch, making it the world's largest tokenized treasury fund. According to CoinDesk, Securitize's revenue for the first three quarters of 2025 grew 841% year-over-year to $55.6 million, and according to PRNewswire, it is going public via a SPAC with a valuation of $1.25 billion. By choosing Securitize as its first Digital Transfer Agent, the NYSE is entrusting the minting authority for tokenized securities to an infrastructure company on the verge of an IPO.

The regulatory side is also advancing. According to CoinDesk, the CLARITY Act, previously stalled for months due to stablecoin yield provisions, recently reached an "agreement in principle," and according to FinTech Weekly, the Senate Banking Committee has set a markup target for late April. In December 2025, the SEC issued a No-Action Letter to the DTC; according to a DTCC official announcement, this letter authorizes the DTC to provide tokenization services under a regulated framework, which is the prerequisite for Nasdaq's plan to proceed.

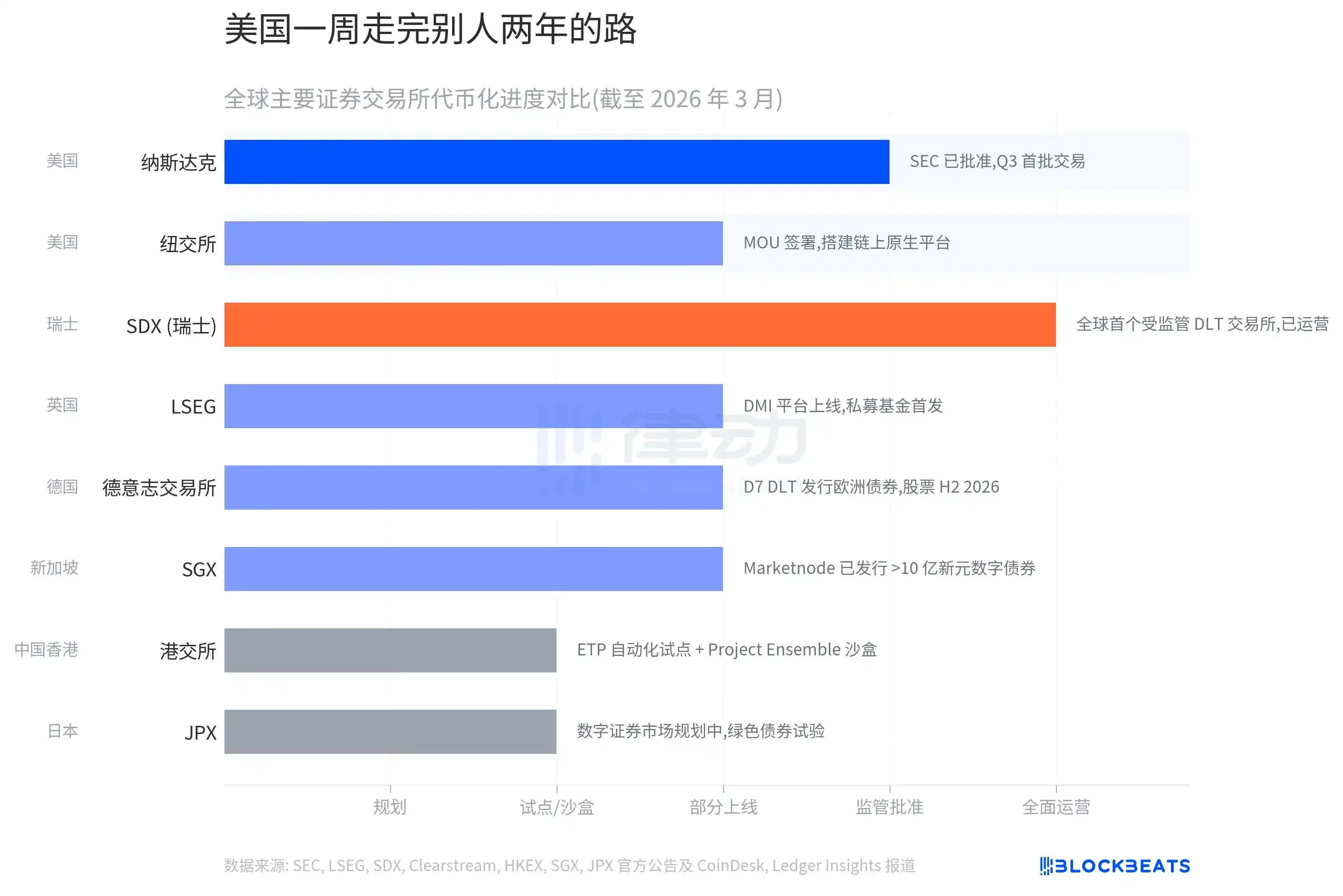

All of this happened within one month. What does this pace mean globally?

Switzerland's SIX Digital Exchange (SDX) was the world's first fully licensed DLT exchange, launching in 2021. According to Ledger Insights, it has issued over CHF 400 million in tokenized bonds, but its daily trading volume is only CHF 2-5 million, with influence largely confined to Switzerland. The London Stock Exchange Group (LSEG) launched its Digital Markets Infrastructure (DMI) platform in September 2025; according to an LSEG official announcement, the first transaction involved private fund tokenization, and it is currently applying for a Digital Securities Depository (DSD) license.

Deutsche Börse's Clearstream began issuing tokenized European bonds on its D7 platform in Q4 2025; according to the Clearstream website, tokenized equities are expected to launch in the second half of 2026. The Singapore Exchange (SGX), through its joint venture with Temasek, Marketnode, has issued over SGD 1 billion in digital bonds according to SGX website data. The Hong Kong Exchange (HKEX) and Japan Exchange Group (JPX) are still in the pilot and planning stages.

Most of these exchanges took two to three years to move from pilot to partial launch. Nasdaq went from SEC approval to its first expected trades in just over a quarter. The NYSE moved from signing an MOU directly to targeting on-chain native settlement. What took SDX five years to achieve, the two major U.S. exchanges have reached their respective starting lines for in a month. Nasdaq added a layer on the existing foundation; the NYSE is pouring a new foundation right next to it.