On March 25, Meta notified approximately 700 employees to leave, affecting five departments including Reality Labs, Facebook social media, recruitment, and sales. On the same day, the SEC disclosed an executive stock option plan, where six core executives will receive stock options tied to a $9 trillion market cap. This is the first time Meta has issued options to executives since its IPO in 2012.

Laying off employees while rolling out the most aggressive executive incentive plan in Silicon Valley history. These two actions taken by Meta on the same day are not contradictory; they are two sides of the same strategy. The AI race doesn't need more people; it needs more expensive people and more machines.

Fewer People, Each More "Valuable"

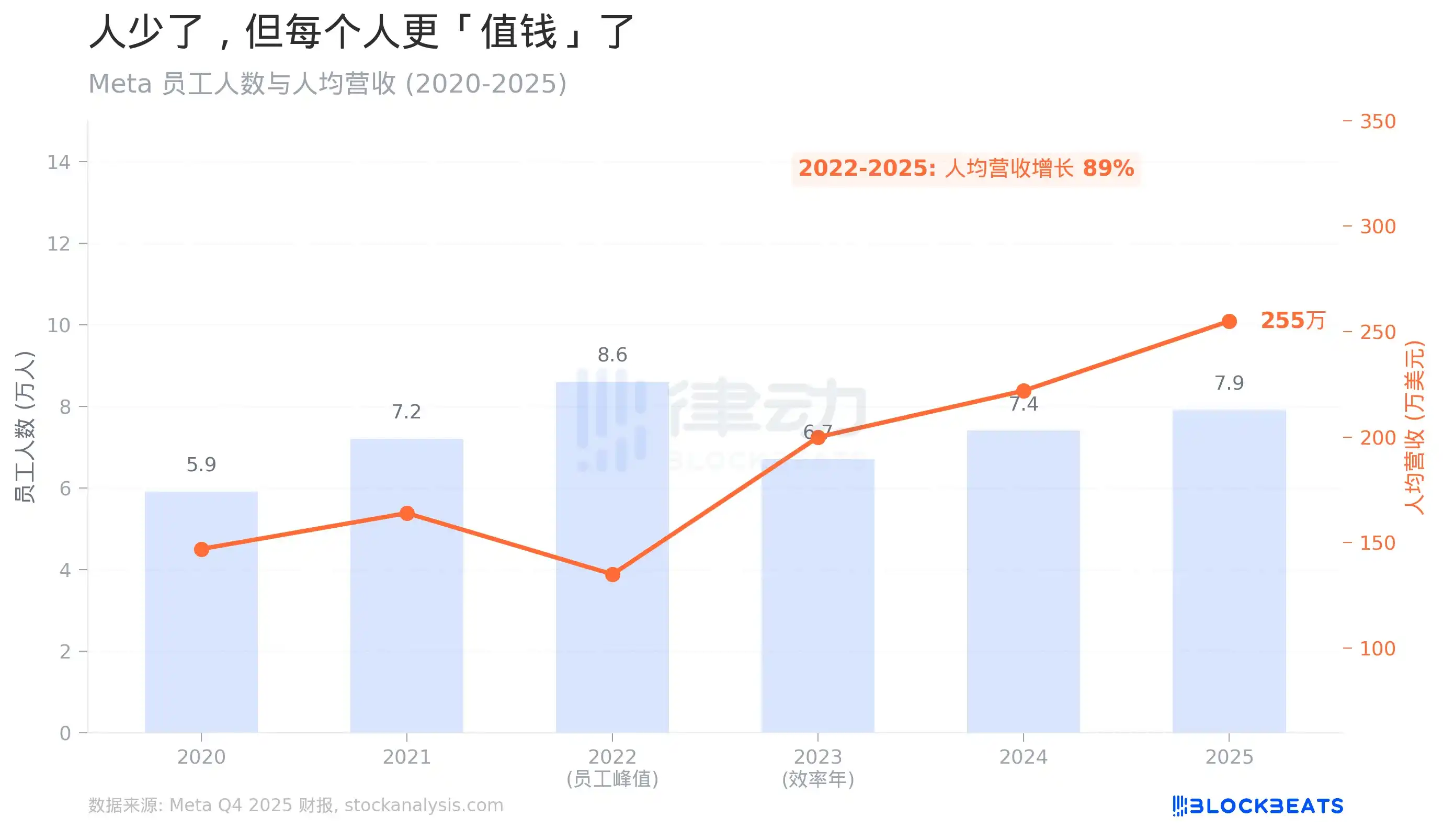

2022 was Meta's peak year for employees, with 86,482 people company-wide. That year, Zuckerberg bet heavily on the metaverse, hiring frantically, only to see annual revenue drop from the previous year's $117.9 billion to $116.6 billion. Revenue per employee fell to a trough of $1.35 million.

What happened next is known to all. In November 2022, 11,000 people were laid off, followed by another 21,000 in 2023, cutting a quarter of the company's workforce. Zuckerberg named 2023 the "Year of Efficiency".

The results of efficiency are written in the numbers. According to Meta's Q4 2025 earnings report, by the end of 2025, the company had 78,865 employees, nearly 8,000 fewer than the peak. However, annual revenue grew from $116.6 billion to $201 billion during the same period, an increase of 72%. Revenue per employee soared from $1.35 million to $2.55 million, an 89% increase.

The meaning of these numbers is straightforward. Meta is making more money with fewer people. In 2022, the marginal revenue brought by each additional employee was declining. By 2024 and 2025, the revenue increase corresponding to each employee reduction was expanding. This is the typical scale effect of a technology company, but Meta accelerated this process through layoffs.

This is the background for this round of 700 layoffs in March 2026. According to The Register, this is already Meta's second round of layoffs this year, with about 1,000 people cut from Reality Labs in January. NBC News, citing informed sources, reported that there may be larger cuts later, potentially involving up to 20% of the total workforce, or about 15,000 people, which would bring Meta's total employee count back to 2021 levels.

Zuckerberg's exact words in the January earnings call were plans to "flatten teams," allowing excellent individual contributors to complete projects that previously required large teams. Meta's spokesperson's response was also templated, saying "teams periodically undergo restructuring or adjustments to ensure they are in the best position to achieve their goals."

Continuing to Bet on the AI Arms Race

Where did the money saved from the laid-off employees go? A look at capital expenditures makes it clear.

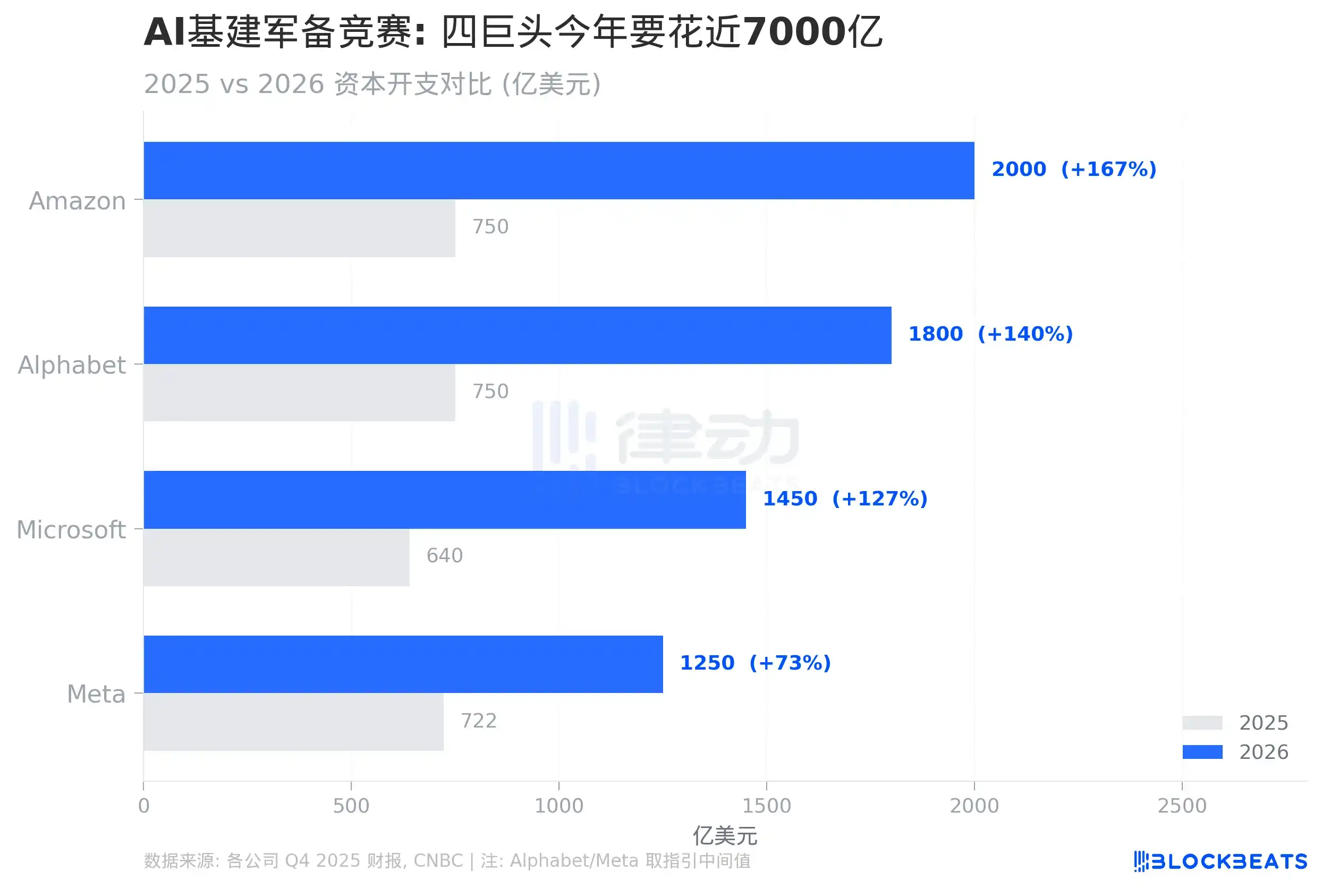

According to Q4 2025 earnings reports and public guidance from various companies, the combined capital expenditures of Amazon, Google, Microsoft, and Meta in 2026 will reach approximately $650 billion, a year-on-year increase of about 130%. This includes Amazon at about $200 billion (up 167%), Google at about $175 to $185 billion (up 140%), Microsoft annualized at about $145 billion (up 127%), and Meta at $115 to $135 billion (up 73%).

According to CNBC, this is the largest single-year capital expenditure in the history of the tech industry. The four companies' investment in AI infrastructure in one year exceeds Sweden's annual GDP.

Meta's absolute value ranks fourth, but relative to its own size, the density of this investment is staggering. Calculated at the midpoint of $125 billion, Meta's AI infrastructure investment per employee is about $1.59 million, close to 62% of the revenue per employee ($2.55 million). Put another way, for every $100 Meta earns, it invests $62 into data centers.

The cost of this money is also direct. According to CNBC, citing Barclays analysts' estimates, Meta's free cash flow in 2026 will decline by nearly 90%. Amazon is even more aggressive; Morgan Stanley expects Amazon to have approximately negative $17 billion in free cash flow in 2026. All four giants are doing the same thing: trading today's cash flow for tomorrow's AI infrastructure.

The $9 Trillion Bet

Now look at the option plan. According to the SEC disclosure documents and analysis by Motley Fool, this plan covers 6 executives, including CTO Bosworth, CPO Cox, COO Olivan, CFO Susan Li, CLO Mahoney, and Vice Chairman McCormick. Zuckerberg is not on the list; his super-voting shares already make additional incentives unnecessary.

The option's exercise conditions are designed with tiered price thresholds. According to Motley Fool, the lowest exercise price is $1,116 per share, requiring the stock price to rise 88% from the current ~$615. The highest tier is $3,727 per share, corresponding to a market cap of about $9 trillion, six times the current $1.5 trillion. There is a five-year window for vesting before 2031. If Meta actually reaches a $9 trillion market cap, according to Motley Fool's calculations, the top four executives (Bosworth, Cox, Olivan, Susan Li) could each see potential gains of approximately $2.7 billion.

The signal of this plan is clear. Meta is not giving executives a bonus; it is using options to tie the core team to an extremely aggressive growth target. The current market cap is $1.5 trillion, the goal is $9 trillion. The difference of $7.5 trillion – Meta is betting that AI can create this value.

For a sense of scale: $9 trillion is roughly equivalent to the combined current market capitalization of Apple and Nvidia. No company in the world has ever reached this market cap. Meta has given its core executives five years to try and reach a number that doesn't exist in human commercial history.

One Formula

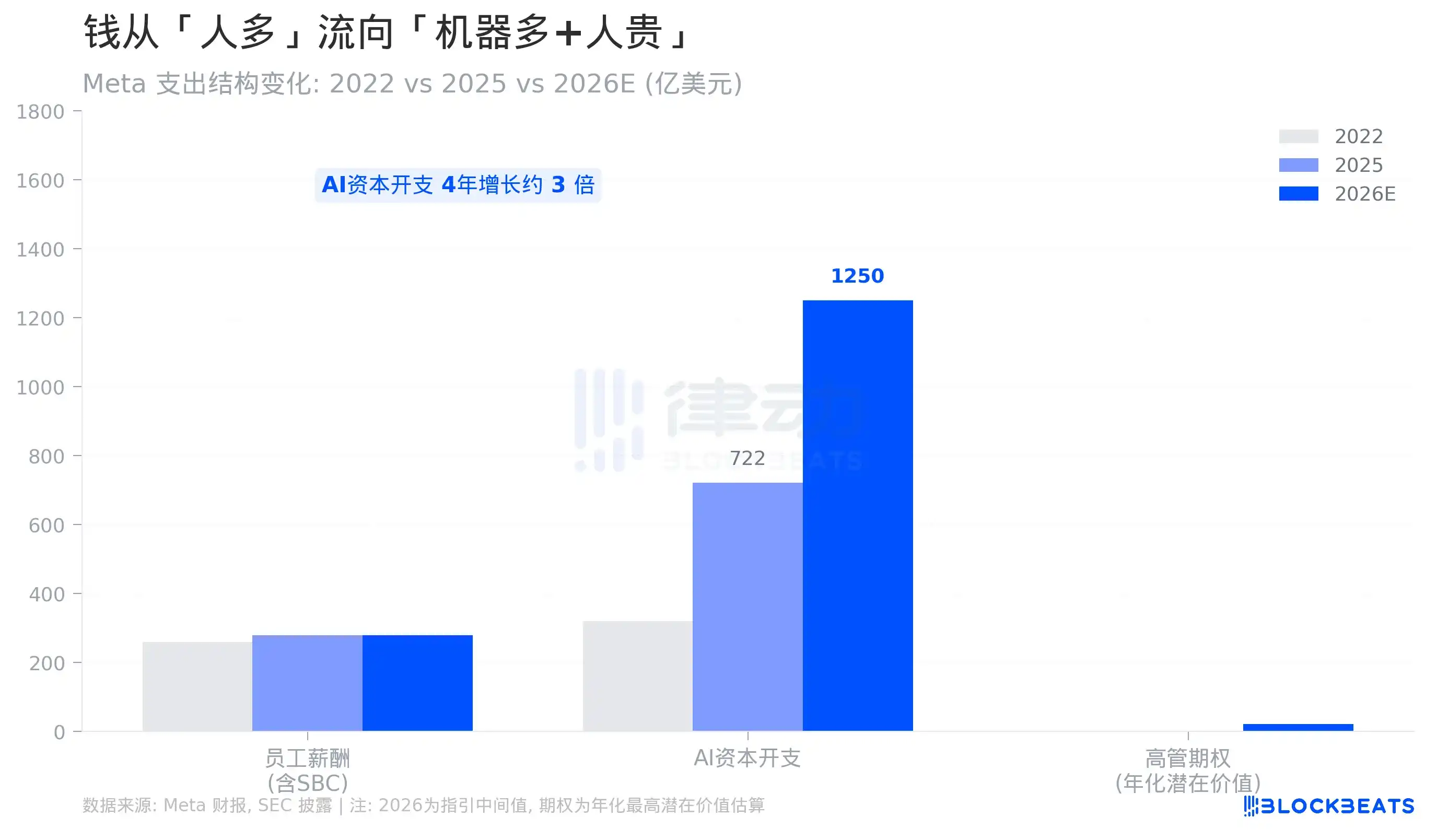

Looking at these three things together, Meta's logic is a simple resource allocation formula. Total employee compensation (including equity incentives) remained largely flat between 2022 and 2026, around $26 to $28 billion. But AI capital expenditures soared from $32 billion to $125 billion, a roughly 3-fold increase in four years. At the same time, a brand new executive option pool has appeared, locking the six most core people into the next five years.

According to Benzinga, Meta's stock-based compensation expense in 2025 was approximately $42 billion, already consuming most of its free cash flow. Signing bonuses for AI researchers have reached nine figures, with reports of researchers poached from OpenAI receiving packages in the $100 million range. The contrast between these numbers and the 700 laid-off employees makes Meta's pricing logic for "people" clear without any need for commentary.

The money saved from laying off 700 people is roughly equivalent to a day and a half of Meta's AI infrastructure spending.