Author: Chloe, ChainCatcher

In the world of traditional finance, stock buybacks are often seen as a "shot in the arm" for market confidence. When a company announces a share repurchase, it usually signifies that management believes the stock is undervalued or that the company has ample cash flow. However, applying a similar strategy to Web3 projects fails to yield positive results.

Recently, Jupiter co-founder SIONG initiated a discussion on X, proposing to halt the $JUP token buyback plan. He stated that Jupiter had invested over $70 million in token buybacks over the past year, but the token's performance has been lackluster. Meanwhile, Helium founder Amir Haleem directly announced the cessation of token buybacks, describing it as "throwing money into a black hole."

Why can tens of millions of dollars in real money not create even a ripple in the crypto market? Is the problem with the underlying design of the buyback strategy? Below is a summary of the performance data of project buybacks last year and market perspectives on project buybacks.

Data Performance: The Collective Waterloo of 2025's Buyback Projects

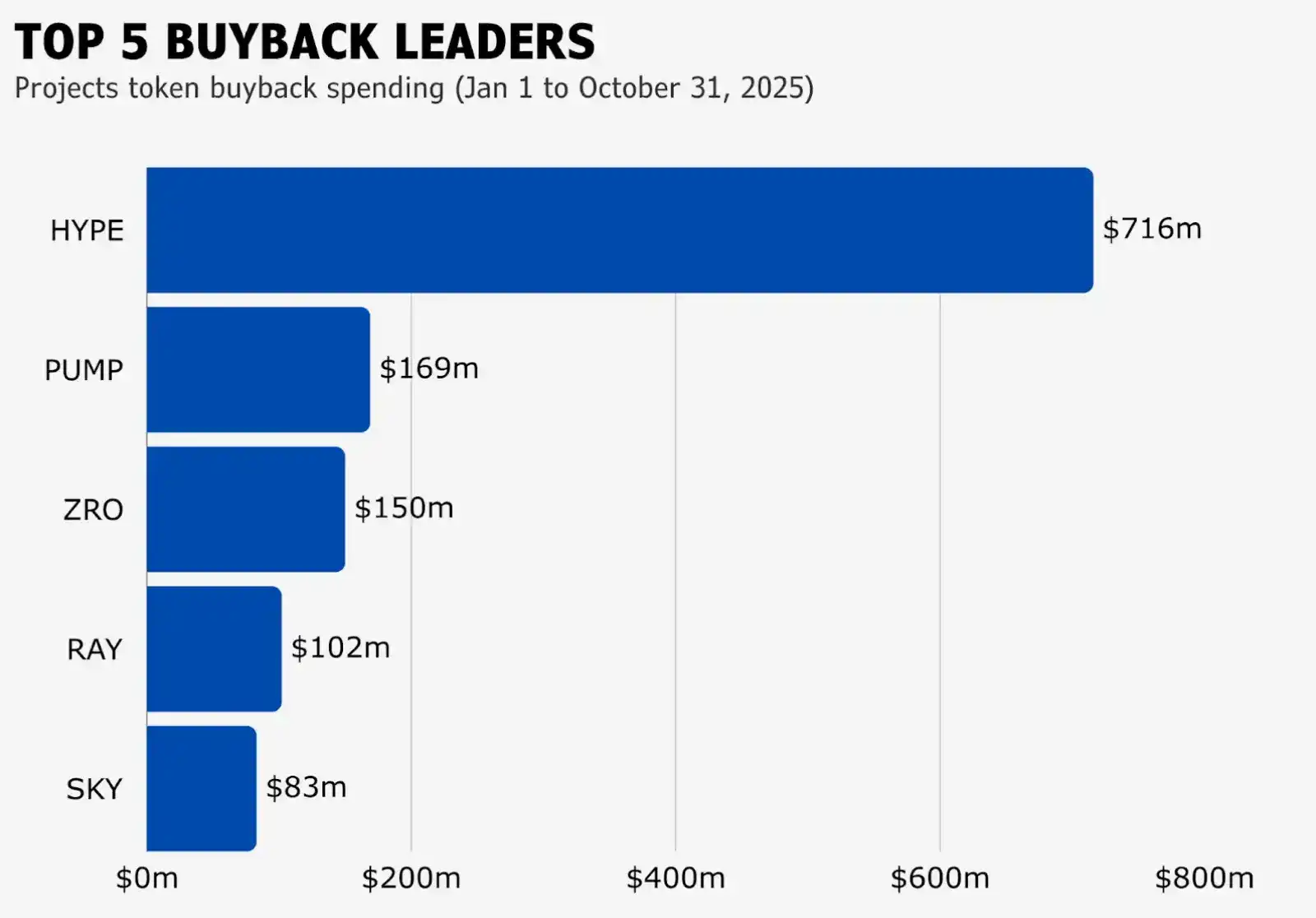

According to market research agency blockmates' tracking of buyback projects from January to October 2025, the top five projects were Hyperliquid, Pump.fun, LayerZero, Raydium, and Sky. Among them, Hyperliquid's buyback amount reached as high as $716 million, while Sky, at the bottom of the list, also invested $83 million.

However, the capital input did not yield proportional returns. Except for Hyperliquid's token price, which remained strong in the first three quarters (it has since fallen from $45.5 at the end of October to $25.94 at the time of writing), almost all other projects experienced continuous declines. This phenomenon has led the market to question: if buybacks cannot enhance token value, is this money essentially wasted?

Viewpoint Debate: The Trade-off Between Buybacks, Staking, and Growth Incentives

Regarding whether projects should stop buybacks, there are starkly different voices in the market:

The founders of Jupiter and Helium lean towards stopping token buybacks and instead using the funds to "acquire users," potentially through subsidizing transaction fees, rewarding new users, or enhancing product features to strengthen fundamentals. However, this shift still faces challenges: tokens will continue to unlock, and users might choose to sell due to a lack of long-term confidence, creating sustained selling pressure and risking a further significant drop in token price.

DeFi OG CM stated that the core meaning of buybacks lies in reducing the circulating supply and establishing a "regular deflation" model. Token price ultimately depends on market supply and demand and project fundamentals, not the buyback action itself. Buybacks are necessarily beneficial for token holders but are not equivalent to a short-term "guaranteed rise." Project teams should not easily halt execution due to low token prices or high buyback costs.

Helius CEO Mert Mumtaz expressed that buybacks are inherently a pessimistic mechanism, implicitly signaling that the project team cannot find a better use for the funds than short-term price boosting, attempting to initiate a growth cycle through price reflexivity rather than product growth. Buybacks are not the optimal strategy in a highly competitive market; the only effective edge case is opportunistic buybacks during market crashes (when equity is irrationally undervalued), combined with aggressive reinvestment during normal times. This is a judgment from a founder's perspective, not an investor's.

Ajit Tripathi, former Head of Institutional Business at Aave and FinTech Partner at ConsenSys, stated that the buyback narrative is the most value-destructive play after meme coins. This logic was initially a marketing tactic by Solana to boast its superiority over Ethereum, but it ended up harming all tokens, even those with revenue, forcing everyone to play pure financial games in the end.

Many other viewpoints have proposed alternative solutions. For example, Selini Capital founder Jordi Alexander observed that the failure of many projects lies not in the mechanism but in the "execution timing" of token buybacks. Some star projects of this cycle (e.g., HYPE, ENA, $JUP) executed large-scale buybacks during the market's most frenzied period when token valuations were most unreasonable. When the price-to-earnings ratio of tokens inflated due to excessive hype, project teams continued buybacks, essentially buying at the peak for sellers, which was a wrong decision. Therefore, Jordi suggests that project teams need more complex "financial engineering," and an ideal model should be dynamic buybacks based on the price-to-earnings ratio.

Solana founder Anatoly believes that projects should not pursue short-term price stimulation (buybacks) but should learn from traditional finance and establish a capital accumulation process spanning 10 years. He favors staking mechanisms more, allowing long-term lockers to obtain more shares, thereby diluting short-term speculators. He believes profits should be stored as "future token claims" rather than consumed in market fluctuations.

Represented by Selini Capital founder Jordi Alexander, some believe the buyback itself is not wrong, but the "amateur execution" is. Projects should hire professional financial advisors to adjust buyback strategies based on the token's price-to-earnings ratio and market cycles, rather than blindly repurchasing, leading to the dilemma of depleting the treasury at the bull market peak and having no funds to protect the price when entering a trough.

Evolution from "Blind Buybacks" to "Strategic Value Management"

Token buybacks are essentially a "deflation tool," not a guarantee of price increase. Amid various market fluctuations, buybacks more often play a role of "passive defense." They can reduce supply and establish a bottom support for the token price, but they cannot single-handedly reverse complex trends formed by macro conditions, unlocking pressure, or market sentiment.

The path to token value growth should evolve from单一的 buyback actions to strategic value management. First, projects need to establish execution strategies with better financial judgment, such as following the logic of "buying low valuation, reserving high valuation": firmly executing buybacks when the token price is far below intrinsic value to maximize capital return; and halting buybacks when market heat is excessive and valuation is unreasonable, instead depositing profits into the treasury as reserve funds or using them to fuel product growth.

Furthermore, buybacks can only address the "supply" issue but cannot create "demand." A project must give users a reason to hold tokens continuously. These reasons may come from the expectation of protocol revenue distribution, the power of ecosystem governance, or the irreplaceable competitiveness of the product itself. Without solid fundamental support, any form of buyback will ultimately become an exit channel for arbitrageurs.