Author: Prathik Desai / The Token Dispatch

Compiled by: Deep Tide TechFlow

Deep Tide Introduction: This article uses data to clarify a commonly confused issue: non-USD stablecoins are not a monolithic block; euro stablecoins and other local currency stablecoins are on completely different paths.

EURT was directly killed by MiCA regulations, but this forced the entire market to rebuild—its supply has nearly tripled since 2023.

A more critical finding is: 90% of non-USD transfer volume is contributed by euro stablecoins, while other local currencies are currently almost only used for payment settlement. DeFi integration is the next stage, not now.

Full text as follows:

Money is only truly useful when it reaches its destination. Wages earned overseas must pass through banks, foreign exchange counters, payment partners, and local compliance reviews before they can return home to pay for rent, tuition, utilities, and food. Until then, it is just value in motion, not yet a medium of exchange.

The same problem now appears on-chain. Stablecoins move funds globally with code, but their utility depends on where they can connect, who is allowed to use them, and which rules govern their reserves and redemptions.

This concept struck me while I was researching Dune's report "Beyond De-dollarization: The Rise of Local Currency Stablecoins".

In today's quantitative analysis, I will explain the factors affecting the growth of non-USD local currency-pegged stablecoins.

The Teeth of Regulation

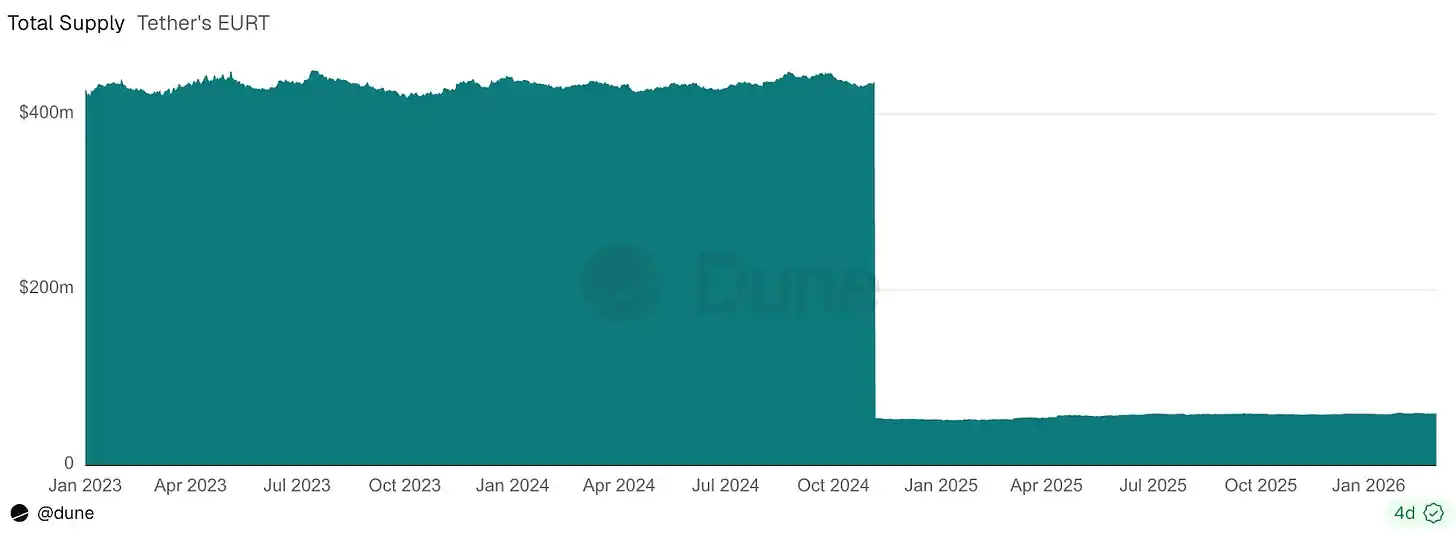

The clearest case of regulatory impact happened to Tether's euro-pegged stablecoin. The European Union's Markets in Crypto-Assets Regulation (MiCA), which came into full effect in 2024, almost immediately pronounced a death sentence on Tether Euro (EURT).

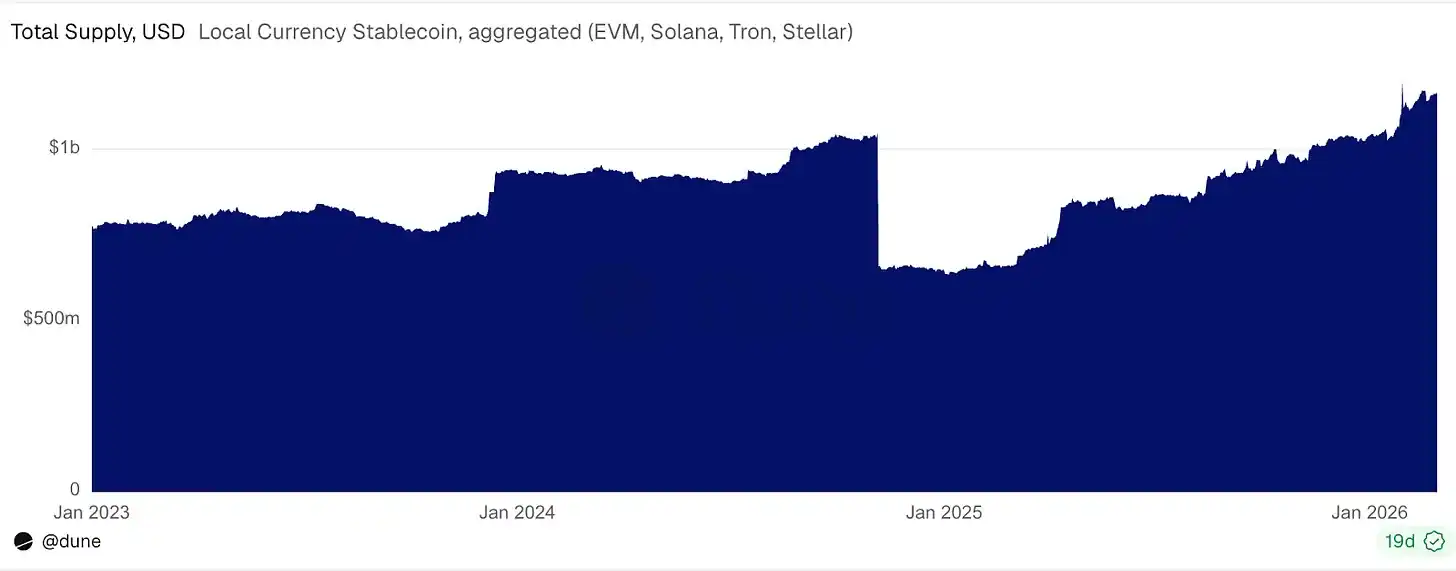

EURT was once one of the earliest and largest non-USD stablecoins, with its circulating supply dropping from over $400 million to about $50 million. The total supply of local currency stablecoins consequently fell from $1 billion to $350 million.

Crypto enthusiasts often assume the code is enough. They create a token, inject liquidity, and expect the market to do the rest. But non-USD stablecoins are not just abstract internet money. They attempt to be better digital versions of local currencies like the Euro, Yen, or Thai Baht, capable of flowing on public rails unrestricted by bank hours. Yet they operate within domestic financial systems, subject to reserve requirements, licensing norms, payment networks, and redemption expectations.

The shutdown of EURT reminds us that first-mover advantage and largest scale are not enough. One change in the domestic rulebook can erase all the advantages of the pioneer.

But regulation is not always detrimental to stablecoins. If it were, non-USD stablecoins might have stalled after EURT's exit.

If EURT is excluded, the total supply of non-USD stablecoins grew from about $350 million in January 2023 to $1.1 billion in February 2026, nearly tripling.

The Market is Expanding

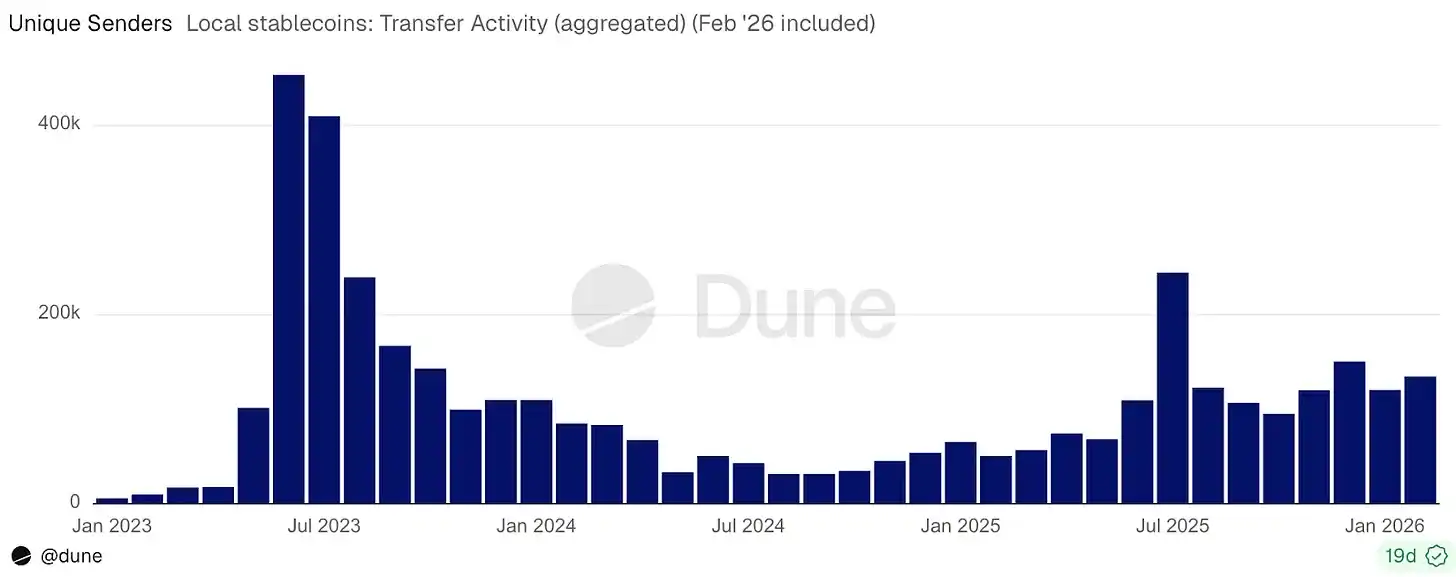

While the supply grew, the number of addresses holding balances of such stablecoins grew from about 42,000 to over 1.2 million in the same period.

Monthly transfer volume increased 16-fold, from $600 million to $10 billion. The monthly number of sending addresses grew 22-fold, from about 6,000 to 135,000.

The growth rate of holders and senders was faster than the growth rate of the supply, indicating the market expanded through increased participation.

Therefore, regulation is not always harmful to the market as it was for Tether Euro; here it actually attracted more stablecoin issuers and users.

Where Non-USD Funds Are Flowing

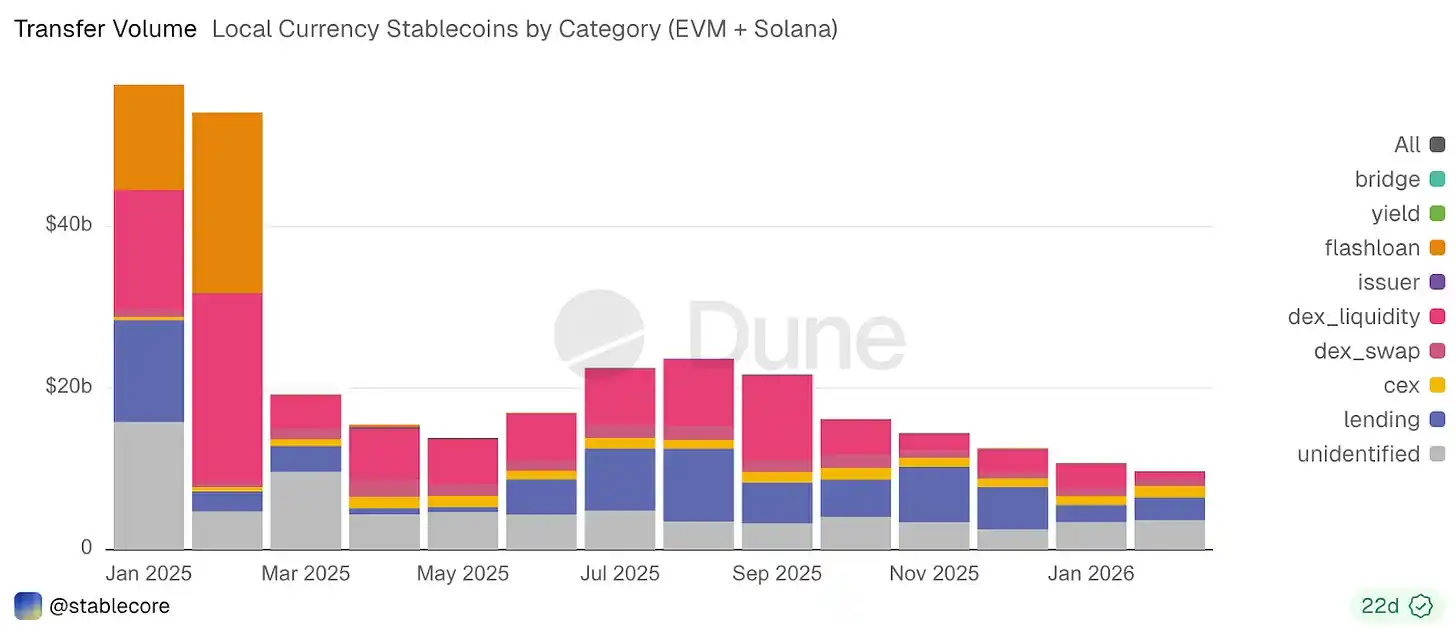

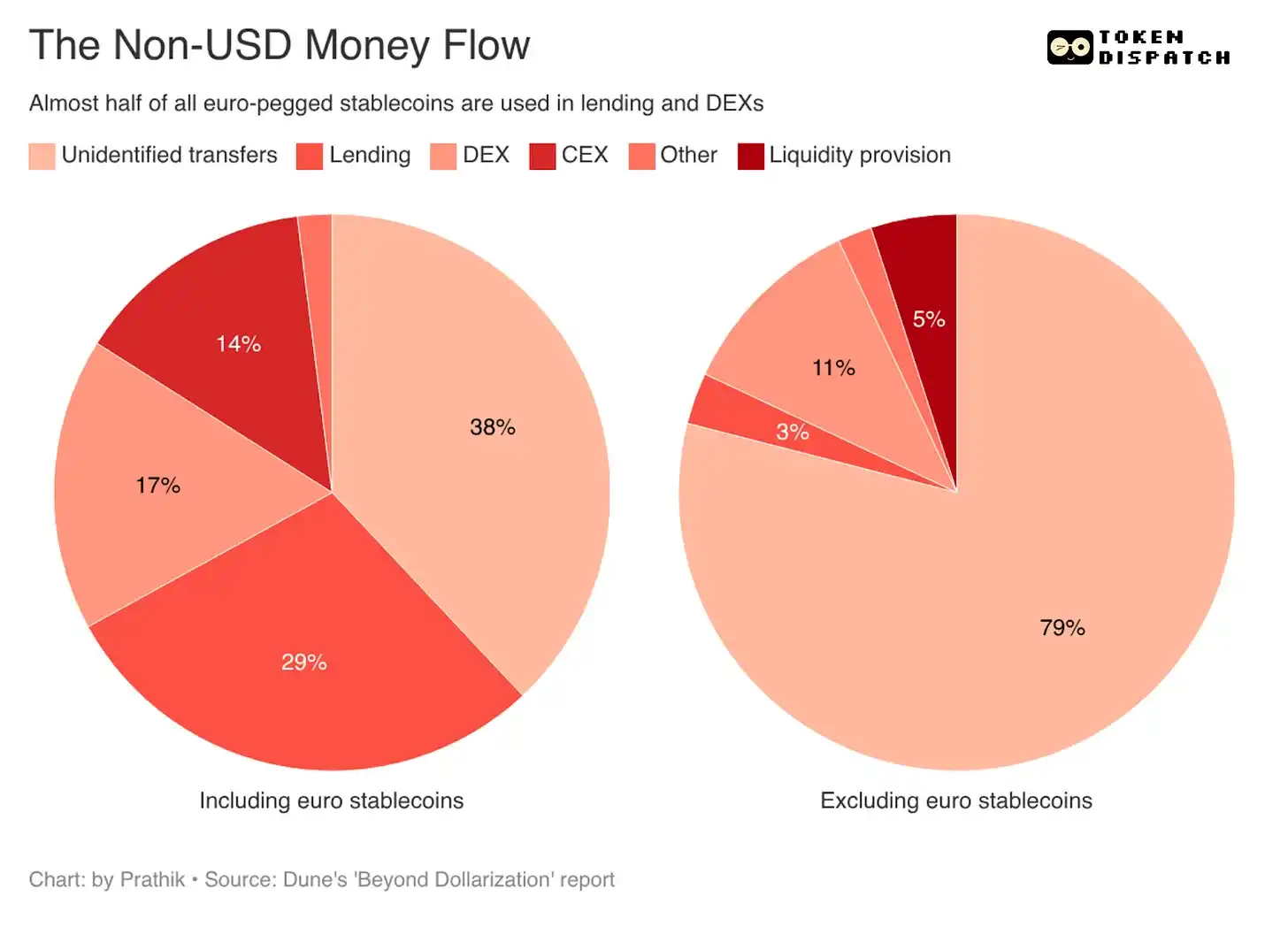

By early 2026, unidentified transfers accounted for 38% of total local currency stablecoin transfer activity. This likely reflects payment and settlement activities, including peer-to-peer transfers and transfers from self-custody wallets to payment service providers.

Next was lending, accounting for 29%; DEX activity accounted for 17%; and centralized exchange-related flows accounted for 14%.

This categorization shows that non-USD stablecoins are primarily used on-chain for two types of scenarios: one is for payments, or as funds flowing between individuals or businesses; the other is for basic DeFi operations, such as lending and trading.

But there is a caveat in the data. If euro-pegged stablecoins are stripped from the data, the market shows a completely different trend.

Euro stablecoins account for over 90% of the transfer volume and are being used as financial assets themselves. Users deposit them into lending markets, use them on DEXs, treating them more as on-chain cash that can earn yield, serve as collateral, and be cycled through DeFi. This makes local currency stablecoins appear more mature.

EURC, along with EURS, EURm, and EUROe, has entered yield-generating DeFi venues like Aave, Morpho, and Fluid.

After removing euro stablecoins, the remaining non-USD digital currencies are primarily used for settlement infrastructure.

Nearly eighty percent of non-USD, non-euro stablecoin transfers fall into the unidentified transfer category. This likely covers wallet-to-wallet fund transfers, business debt settlements, remittance-style transfers, and payment flows circulating through service providers.

The dominance of euro-pegged currencies among non-USD stablecoins indicates that the next phase of growth is more likely to be concentrated in basic DeFi operations. Beyond the euro, non-USD stablecoins will first expand as infrastructure for domestic funds flowing on digital rails, before they can be used for basic DeFi operations.

This growth is crucial because it will come from stablecoins used for payroll, treasury management, merchant settlements, remittances, and foreign exchange (FX).

These areas are more heavily regulated than basic DeFi operations because operating funds tolerate far less ambiguity than speculative assets. If a token is expected to operate within domestic payment systems, treasury workflows, and environments with strict compliance requirements, it will need predictable reserves, clear redemption processes, and legal clarity. Therefore, regulation will play a key role in the adoption of non-USD stablecoins.

This also explains why growth is concentrated in regions with mature financial systems. The report notes that the activity of the Brazilian Real (BRL) and Japanese Yen (JPY) accelerated after improvements in local regulatory frameworks; while markets lacking specific regulatory regimes, such as Indonesia, lagged behind.

I also found the economic rationale for non-USD stablecoins.

Cross-border payments still bear high conversion costs, with remittances losing a considerable portion to FX spreads and intermediary steps. More local currency stablecoins can reduce the amount of value that needs to detour through the US dollar before reaching its destination. This can lower foreign exchange costs, eliminate settlement friction, and allow businesses and individuals to hold value in the currency they earn, spend, and save.

Its potential is far greater than DeFi itself. Euro stablecoins have already set a strong precedent for integrating local digital money into the financial system. However, the bigger win would be reducing the cost and speed of global cross-border fund flows and reducing reliance on the US dollar globally.

Issuers who can make local currencies easier to send, settle, and embed into existing payment infrastructure will benefit from the huge potential of non-USD stablecoins. If they can create favorable conditions for better adoption, DeFi integration will naturally follow.