Author: SpecialistXBT

Original Title: Citrini's Echo Lingers

An excellent article can lead the market to confuse "scenario projection" with "real prophecy".

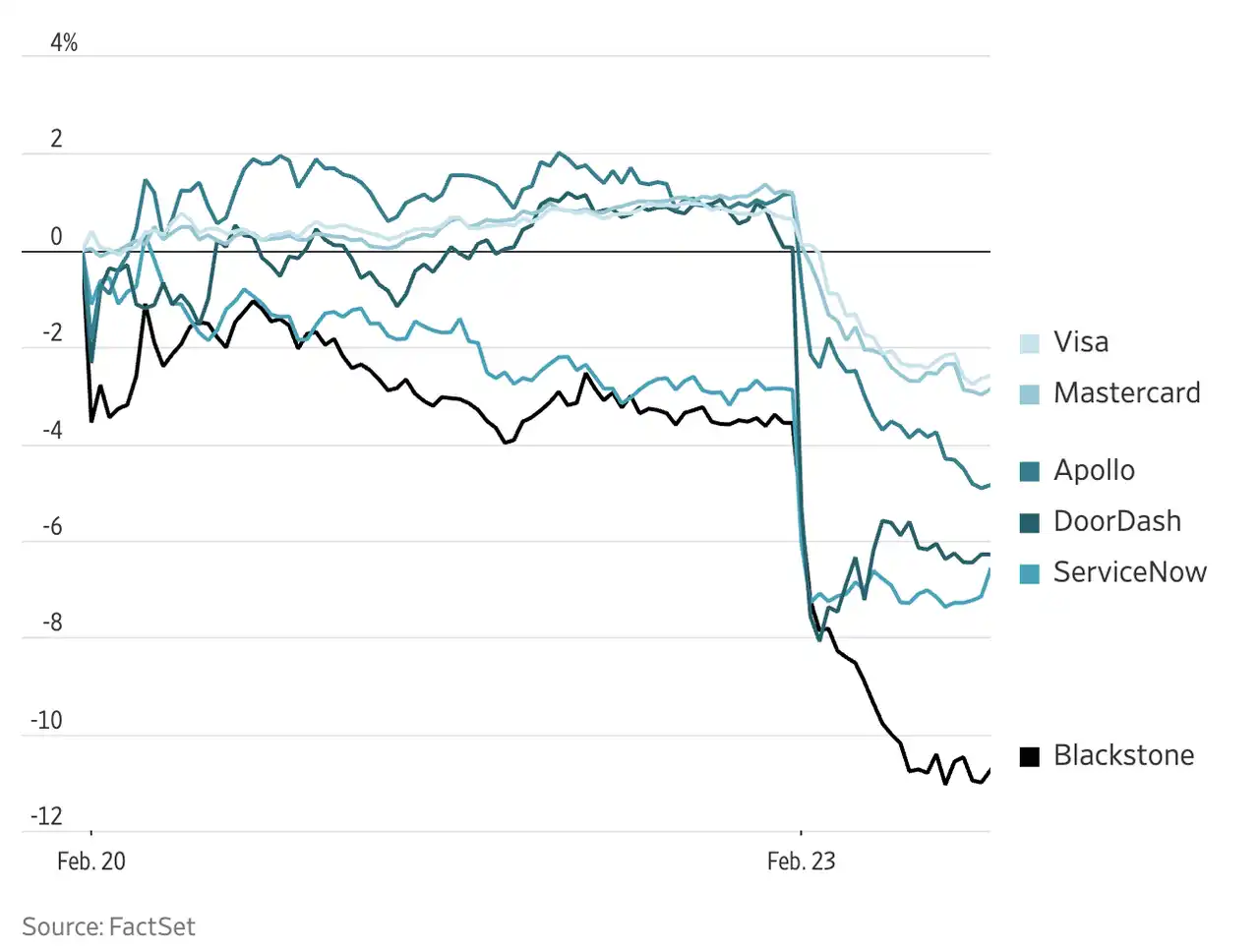

On February 22, 2026, a report titled "The 2028 Global Intelligence Crisis" exploded on social media and financial markets, with page views exceeding 27 million. On the day of the report's release, IBM plummeted 13%, while stocks of companies like DoorDash, American Express, and KKR all fell by more than 6%.

This report was written by James van Geelen, the founder of Citrini Research. This 33-year-old researcher has over 180,000 followers on X, and his Substack ranks first among financial authors, focusing on thematic equity investments and global macro research, known for its cross-asset, lateral thinking style. His real investment portfolio has achieved returns of over 200% since 2023. The report, in the form of a scenario projection, fictionalizes a future set in 2028: AI massively replaces white-collar labor within just two years, triggering consumption contraction, software asset defaults, credit tightening, and ultimately pushing the economy into a畸形 state of "technological prosperity" and "social recession." Van Geelen noted at the beginning: "This article is about a possible scenario, not a prophecy." But the market clearly had no patience to distinguish between the two.

However, more noteworthy than the brief market panic is the widespread discussion this article has sparked over the past few days. From academia to investment circles, from Wall Street to the Chinese internet, more than a dozen response articles from different perspectives have emerged. Rather than trusting only one extreme conclusion, perhaps we can piece together a clearer future from the "disagreements and overlaps" of various viewpoints.

What Citrini Said

The logical thread in Citrini's article is not complicated: leaps in AI capabilities lead to large-scale replacement of white-collar jobs → rising unemployment triggers consumption expenditure contraction → structured financial products with SaaS as the underlying asset face a wave of defaults → credit tightening spreads to the broader financial system → the economy falls into a畸形 state of "technological prosperity" and "social recession."

Every link in this causal chain is not without basis. But connecting them end-to-end and projecting them seamlessly into a crisis requires a series of rather radical assumptions.

There are many ways to deconstruct this chain. We might as well expand on three core sub-points: the speed and scale of labor replacement, the transmission mechanism of demand collapse, and the possibility of a financial crisis, and see what different voices are actually debating around each link.

No Break, No Build

Citrini's starting point is the large-scale replacement of white-collar labor by AI. In his narrative, this process accelerates dramatically between 2026 and 2028, with practitioners in law, financial analysis, software development, customer service, and other fields being the first affected.

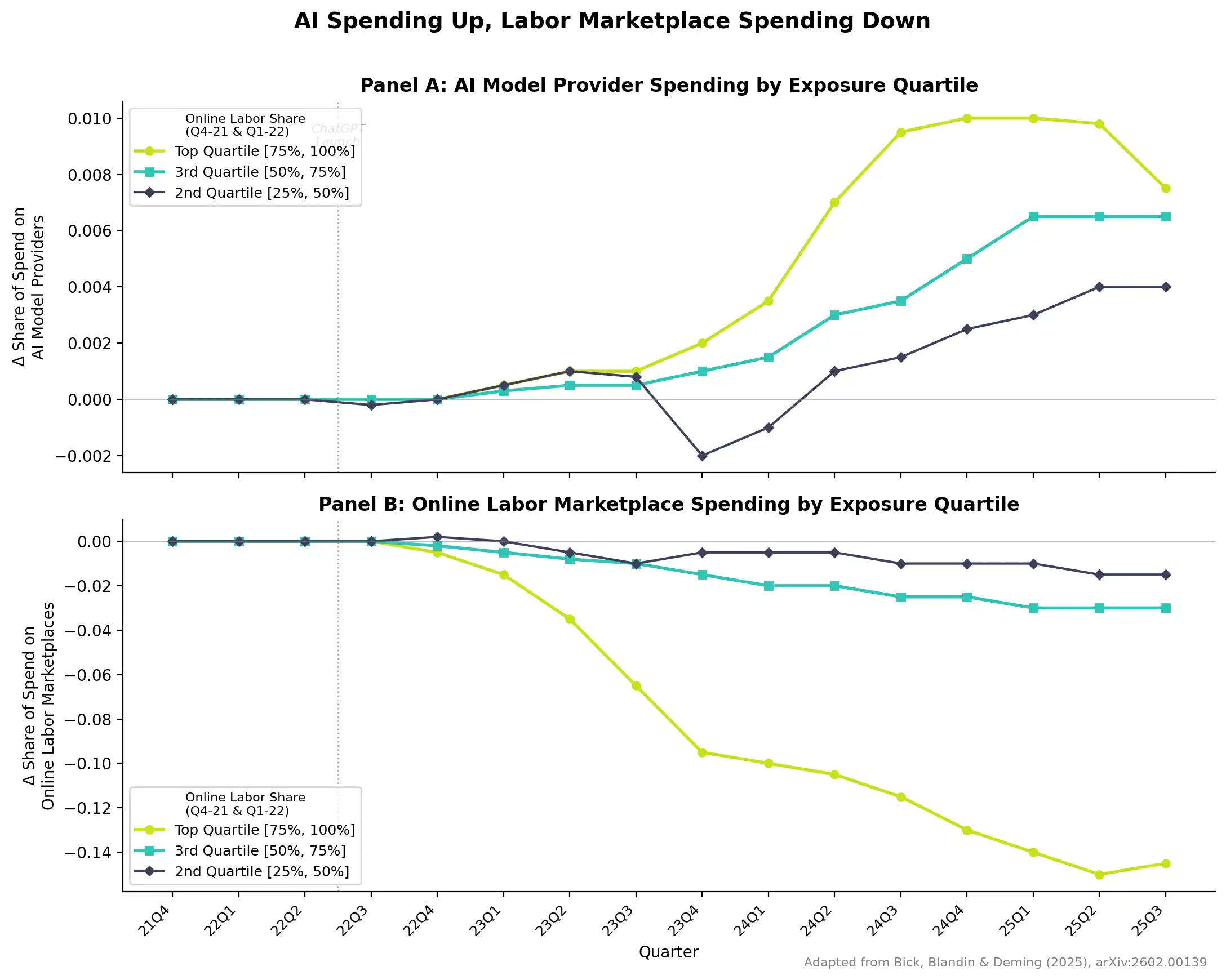

Changes in the proportion of enterprise spending on AI model suppliers and online labor platforms, grouped by industry's AI exposure

There is evidence supporting Citrini's view. An empirical study by Bick, Blandin, and Deming based on corporate spending data shows that after the release of ChatGPT, companies with the highest AI exposure (i.e., those with the largest share of spending on online labor markets) significantly increased their spending on AI model providers while reducing spending on online labor markets by about 15%. It is worth noting that this substitution is not "dollar-for-dollar"—for every $1 reduction in labor market spending, companies increased AI spending by only $0.03 to $0.30. In other words, AI is performing the same work at a far lower cost than human labor.

But Citrini may have overestimated the speed of this transformation. A critic cited the example of the U.S. real estate agent industry: despite technology having long had the capability to drastically reduce the number of agents, the industry still employs over 1.5 million people today. Institutional inertia, regulatory barriers, and internal industry利益博弈 form a line of defense far stronger than technology. He believes Citrini seriously underestimated the resistance of "institutional momentum."

Another critic cited a 1998 study by Kimball, Basu, and Fernald, pointing out that technological shocks in history have often been positive stimuli on the supply side—short-term adjustments in employment structure may accompany them, but in the long run, the output space they create is far greater than the jobs they destroy.

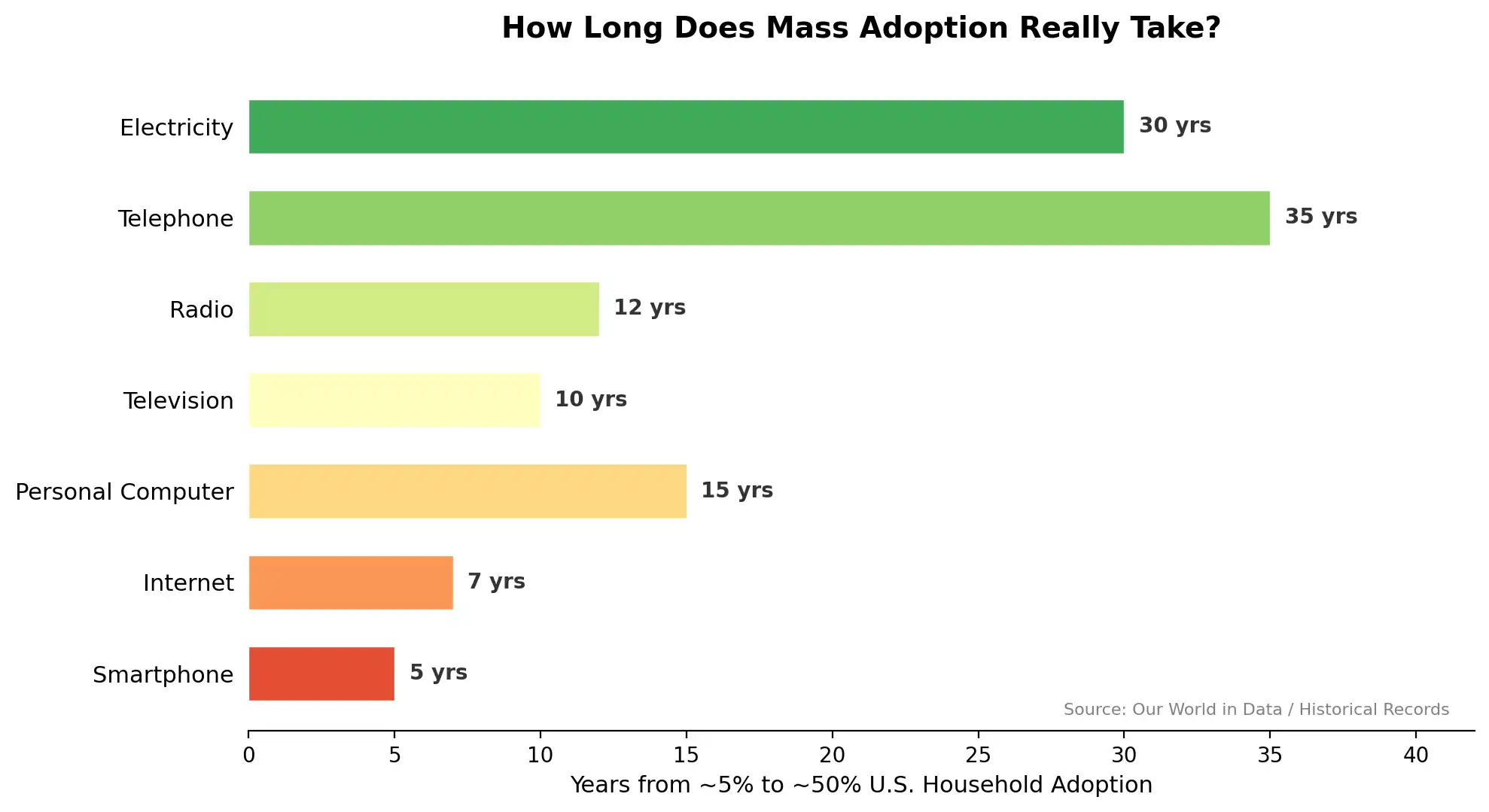

In fact, reviewing the diffusion of every round of General Purpose Technologies (GPTs) in history, the process from the laboratory to large-scale penetration has always been much slower than the maturation of the technology itself. Electricity took 30 years to go from a 5% household penetration rate to 50%, the telephone took 35 years, and even the fastest-diffusing smartphone took 5 years. AI's technical capabilities may be sufficient to颠覆 many industries, but the gap between technical capability and institutional absorption has never been bridged by capability alone.

The second key link in Citrini's narrative is the downward spiral on the demand side: unemployment → reduced income → consumption contraction → declining corporate profits → further layoffs.

Citrini混淆了 demand-side deflation and supply-side deflation in this link. The former means a萎缩 in consumers' purchasing power, while the latter is technological progress压低 production costs—the price decline driven by AI is essentially closer to the latter, similar to the price trajectory of electronic products and communication services over the past few decades. Some analysts believe that Jevons Paradox will still hold: when AI大幅压低 the cost of services like legal advice, medical diagnosis, and software development, demand that was previously excluded due to high prices will be unleashed, leading not to contraction but explosive growth in total volume. At the same time, Moravec's Paradox will also come into play. For machines, what is truly difficult is often not profound logical reasoning or massive data retrieval, but rather the physical movement, sensory perception, and emotional communication that humans take for granted. This means that manual labor and service industry jobs requiring fine perception may be more resilient than we imagine.

But Jevons Paradox could also fail. University of Chicago economics professor Alex Imas pointed out that if AI automates the vast majority of labor, and labor income's share of total income drops sharply, then who will buy these efficiently produced goods and services? This touches the distribution mechanism itself. When output capacity tends towards infinity and effective demand tends to concentrate, what we face may not be a recession, but an imbalance not fully discussed in economics textbooks—material abundance that remains out of reach.

A Glimpse from a Tube

The part with the biggest leap in Citrini's projection is the transmission from employment shock to financial crisis. In his narrative, structured financial products with SaaS revenue as the underlying asset (he calls them "Software-Backed Securities") encounter widespread defaults in the wave of AI transformation, triggering a credit crunch similar to 2008.

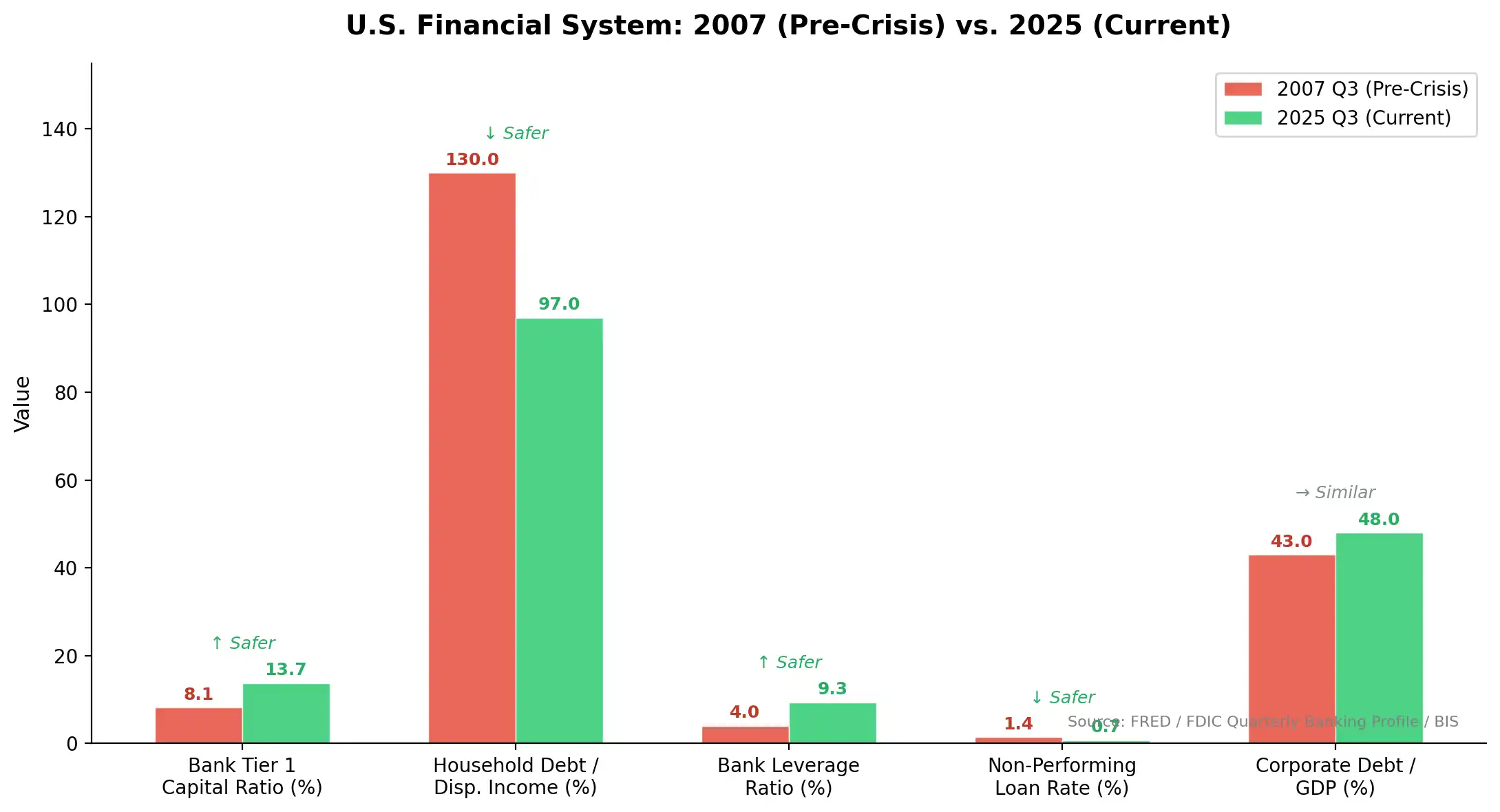

However, commentators point out that compared to 2008, the leverage ratio of the current U.S. corporate sector is much healthier, and the banking system, after undergoing Dodd-Frank reforms and multiple stress tests, is far more robust than it was then.

Relative to the eve of the 2008 economic crisis, various resilience indicators of the current U.S. financial system have significantly improved: bank tier 1 capital adequacy ratio rose from 8.1% to 13.7%, household sector debt-to-disposable income ratio fell from 130% to 97%, and non-performing loan ratio dropped from 1.4% to 0.7%.

Even if some SaaS companies do face declining revenue, their scale is not enough to trigger a systemic credit crisis. Former Bloomberg financial columnist Nick Smith believes Citrini made a common mistake in this link: linearly extrapolating a micro-level industry shock into a macro-level systemic risk. For the demand collapse, Smith's answer is fiscal policy. If unemployment真的 rises sharply, the government is fully capable and willing to underpin demand through large-scale fiscal stimulus.

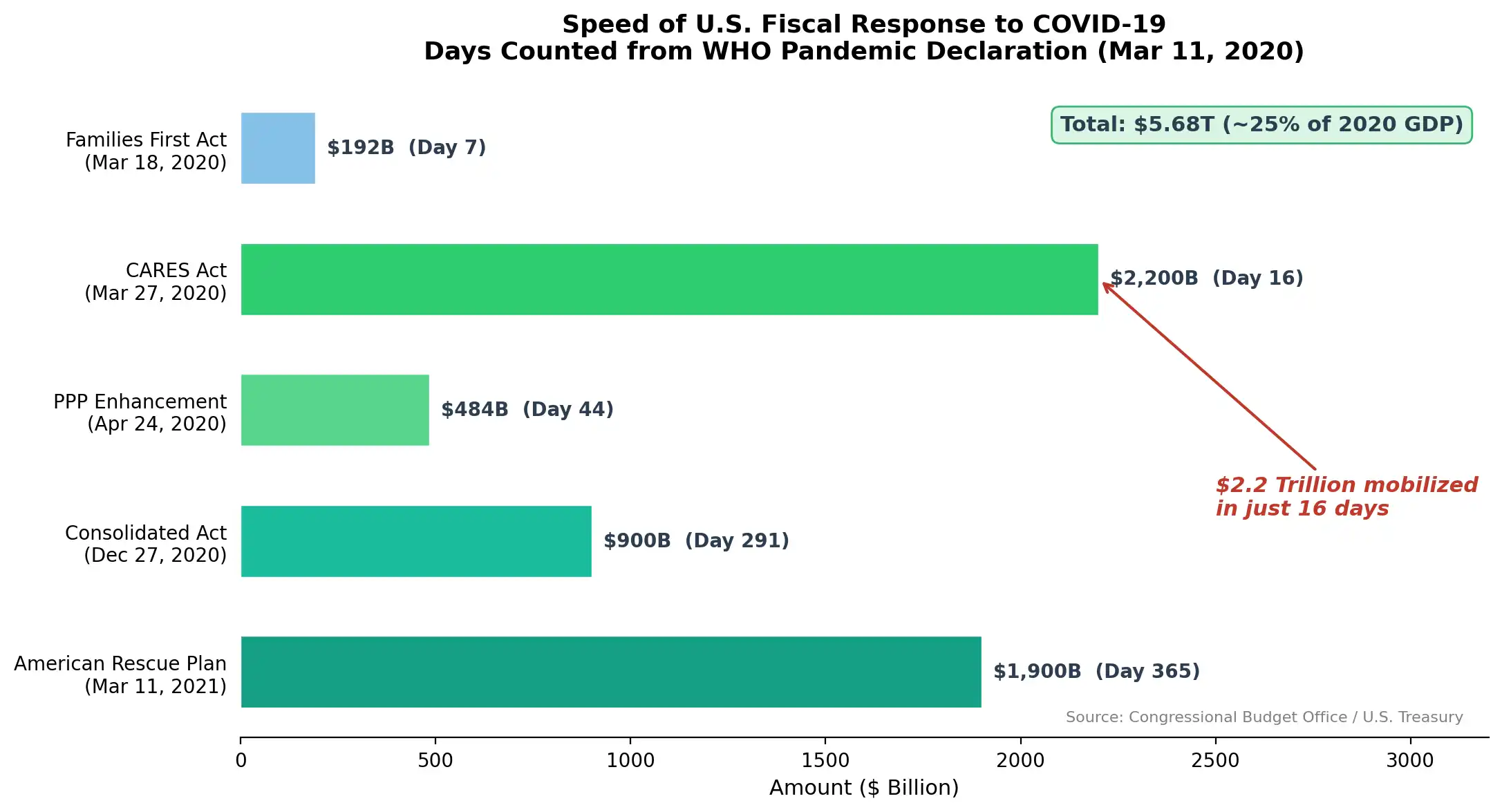

The system's response capacity also seems underestimated. Taking the policy response during COVID as an example, the WHO declared a pandemic on March 11, 2020, and just 16 days later, the $2.2 trillion CARES Act was signed into law. Within the following year, the U.S.累计推出 $5.68 trillion in fiscal stimulus, equivalent to about 25% of 2020 GDP.

If AI-driven unemployment真的 occurs at the speed and scale described by Citrini, policy intervention is unlikely to be absent.

Other commentators raised doubts at a more fundamental level. Technological doomsday theories普遍 stem from a lack of faith in humanity. Citrini's projection treats the market as an unattended machine, allowing "causality" to unfold on its own until collapse. But the real economic system does not operate this way. Laws, institutions, politics, culture, and ideology profoundly determine how the real world absorbs technological shocks.

Consensus and Disagreement

We can perhaps try to mark some consensus and分歧.

That AI is and will continue to change the demand structure of white-collar labor is almost undeniable; the分歧 lies only in the speed and scale of the change. Additionally, the pain of the transition period is real and should not be obscured by long-term optimism. Also, the quality and speed of the policy response will largely determine the outcome.

Disagreements exist at a deeper logical level. Some believe this technological shock may exceed historical precedents in speed and breadth, making historical analogies less applicable; others trust more in the adaptability of institutions and the repeatability of history.

Look Up

Citrini's article has many problems: the logical connections are too tight, institutional responses are systematically underestimated, and the jump from micro-industry shock to macro-systemic risk lacks sufficient intermediate argumentation. But its most fundamental problem may lie in an underestimation of human society: it assumes a static institutional environment where technology crushes everything at an almost unstoppable speed. Doomsday theories about technology have proliferated throughout history; they are often flawless in technical logic but almost invariably ignore the variable of "human beings." The complexity of human society, its friction, its redundancy, its seemingly inefficient institutional arrangements,恰恰 constitute a powerful, distributed shock absorption capacity. We have ample time to avoid those projected doomsdays, provided we are not frightened by the projections themselves.

What about the optimistic narratives? The "Jevons Paradox" is an observation about long-term trends. "Moravec's Paradox" tells us that manual labor is temporarily safe, but it doesn't tell us where the replaced white-collar workers should go. Historical analogies are instructive, but history never repeats itself exactly, it only rhymes. Optimistic narratives need time to be tested, and we are at the starting point of that test.

Doomsday production, anxiety consumption. Forge your own judgment, bear risks, manage positions, rather than indulging in those articles that "see the end at a glance".

Twitter:https://twitter.com/BitpushNewsCN

Bitpush TG Discussion Group:https://t.me/BitPushCommunity

Bitpush TG Subscription: https://t.me/bitpush