Charles Hoskinson says Cardano’s Pentad initiative is dealing with a roughly $40 million funding gap after ADA fell from around $0.83 at the time of the original proposal to roughly $0.25. In a March 6 video update, the Cardano founder said the plan was initially working with the equivalent of about $58 million in value from 70 million ADA, but that figure has since dropped to about $18 million.

That repricing, he argued, has fundamentally changed the economics of the program. “The reality is that there’s a $40 million shortfall between when we wanted to do it and where we’re at today,” Hoskinson said. “Every single member of the Pentad has to accept that shortfall, meaning out of pocket for commitments and obligations. They have to make it up.”

Hoskinson Defends The Cardano Pentad

Pentad was designed as a coordinated effort between five core Cardano ecosystem entities to secure commercially important integrations for the network more efficiently and at scale. Hoskinson said the original logic was that Cardano and Midnight could negotiate together and get better aggregate terms, but the collapse in ADA’s dollar value means even the Cardano-side integrations now cost more than the treasury-backed funding effectively covers. Midnight, he said, is also paying for its own integrations out of pocket, with liabilities exceeding $10 million.

A central point of the update was a reimbursement dispute tied to Fireblocks. Hoskinson said one party had negotiated separately with Fireblocks outside the Pentad process, reached its own fee arrangement, and then later sought reimbursement. That, he argued, is not comparable to the more expansive and expensive integration the Midnight Foundation had been negotiating and was never part of the original governance-approved structure.

“Everyone in the Pentad is at a loss. We did not make a profit,” he said. “The vast majority of the integrations will require out-of-pocket expenses from the Cardano Foundation, the Midnight Foundation, Input Output, Emergo, and Intersect and long-term liabilities because many of these things required multi-year contracts.” By contrast, he added, external actors who were not signers to those liabilities cannot reasonably expect to be made whole simply because earlier public comments were made under different assumptions.

Hoskinson nevertheless cast Pentad V1 as an operational success. He said Cardano went from signing a deal with Circle to having USDCX live on the network in 84 days, calling it the number one stablecoin on Cardano already. He also pointed to integrations with LayerZero, Pyth, Dune Analytics and custodians, arguing the effort has moved Cardano from being “an island” to being connected to the broader crypto market.

Related Reading: Cardano Founder Sounds Alarm Over New US Crypto Bill

That shift matters because, in Hoskinson’s view, Cardano’s next challenge is no longer core infrastructure. It is utility, user experience and DeFi traction. He said the ecosystem still needs strategic capital deployment to help applications survive and compete, and floated Pentad V2 as a possible treasury-backed “weighted index” of Cardano DApps and DeFi projects rather than a grant program.

“We don’t have an infrastructure problem,” he said later in the video. “We have DApps and DeFi and we have an experience problem. We were an island. We’re no longer an island. We built those bridges. That’s what you paid for with Pentad.”

The broader message was political as much as financial. Hoskinson framed the reimbursement fight as a test of whether Cardano’s on-chain governance can function under stress without collapsing into public infighting. If the ecosystem can align behind difficult capital-allocation decisions despite lower token prices, he argued, Pentad could become less a funding controversy than an early demonstration of whether Cardano’s governance model can actually execute.

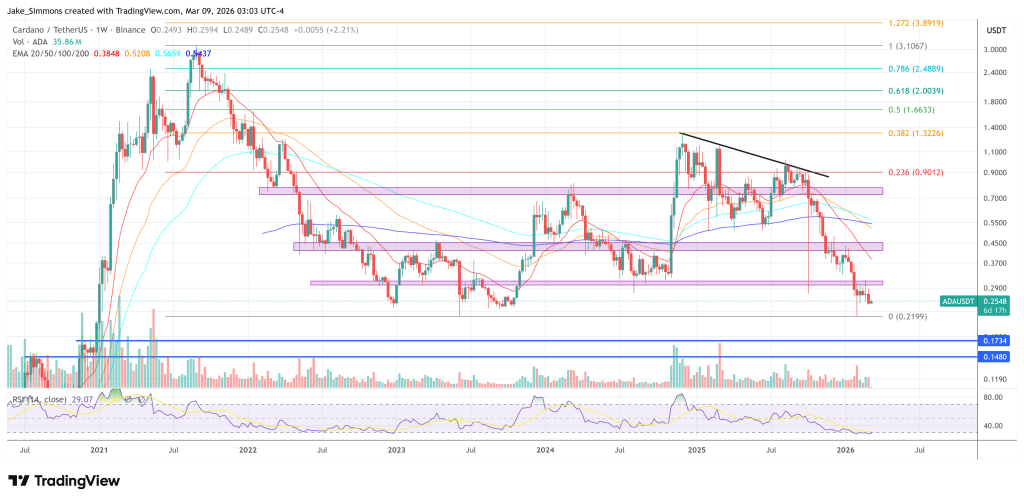

At press time, ADA traded at $0.2548.