As 2025 draws to a close, the crypto market is exhibiting an unprecedented "split" landscape: Bitcoin (BTC) is repeatedly hitting new all-time highs, driven by institutional capital, having once touched $125,000; Ethereum (ETH) is struggling around $2,800, still significantly below its historical peak; and the once "rising tide that lifted all boats" altcoins have plunged into an abyss, with most projects down 80-95% from their 2021 highs, failing to recover even as BTC reaches new heights.

This completely deviates from the classic narrative of the crypto market over the past decade. The traditional "four-year cycle" script—"BTC rises first → ETH catches up → altcoins surge in rotation—seems to have completely failed in 2025. The familiar "carving the mark on the moving boat" strategy of veteran players has now become a joke of "carving the mark to find fish".

Meanwhile, outlook reports for 2026 from institutions like Grayscale and CoinShares further reinforce a harsh reality: the "class solidification" of the crypto market is accelerating—BTC is becoming the "digital gold" for institutional asset allocation, while altcoins are relegated to a "twilight of the gods" with dried-up liquidity.

Is this a temporary failure of the cycle, or a permanent change in market structure? This article will deconstruct this ongoing "crypto paradigm shift" from four dimensions: phenomenon observation, underlying mechanisms, institutional behavior, and liquidity structure.

I. Phenomenon Observation: The "Great Divergence" Between BTC and Altcoins

1.1 Data Doesn't Lie: Unprecedented Performance Divergence

The crypto market in 2025 can be aptly described as "a tale of two extremes".

Chart: ETH/BTC Exchange Rate

1. Bitcoin's "Never-Setting Sun":

- Robust Price Performance: Rose from around $70,000 at the start of the year to a high of $125,000 (+78%), still maintaining between $86,000-$88,000 even after pullbacks.

- Institutional Capital Inflow: Spot ETFs saw net inflows of tens of billions of dollars, with products like BlackRock's IBIT dominating the market.

- Highly Concentrated Holdings: ETFs hold over a million BTC; MicroStrategy holds about 670,000 BTC (3.2% of circulating supply).

- Increased Market Dominance: BTC's dominance surged from 50% in early 2024 to 59-60% currently, a multi-year high.

2. Ethereum's "Midlife Crisis":

- Severely Lagging Gains: Limited gains this year, current price around $2,800, far inferior to BTC's performance.

- Collapse in Relative Value: ETH/BTC rate fell to multi-year lows, down over 60% from its historical high.

- Lackluster Institutional Interest: Total AUM of spot ETFs is far lower than BTC ETFs, with periodic outflows.

- Sluggish On-Chain Activity: Significantly reduced Gas fees, reflecting weak user activity and network demand.

3. Altcoins' "Twilight of the Gods":

- Seasonal Indicator Collapse: Altcoin Season Index remained below 20 all year (above 50 indicates altcoin season), the longest period of depression on record.

- Widespread Underperformance: Most projects in the top 100 by market cap underperformed BTC this year; many are down over 80% from 2021 highs.

- New Listings Immediately Break Issue Price: New coins listed on major CEXs in 5 routinely broke their issue price upon listing; VC coins became "poison".

- Liquidity Drying Up: Average daily trading volume for altcoins plummeted over 70% compared to 2021; insufficient CEX depth means any selling pressure can trigger a crash.

1.2 Historical Comparison: This Time "It's Really Different"

Looking back at the past three bull markets, the rotation logic of "BTC → ETH → altcoins" was almost an iron law of the market:

2017 Bull Market: The Classic Three-Stage Rocket

- BTC rose from $1,000 to $20,000 (+1,900%)

- ETH skyrocketed from $8 to $1,400 (+17,400%)

- ICO泡沫引爆,山寨币普遍50-500倍涨幅 (ICO bubble ignited, altcoins普遍 gained 50-500x)

2020-2021 Bull Market: The DeFi and NFT Carnival

- BTC rose from $10,000 to $69,000 (+590%)

- ETH rose from $200 to $4,800 (+2,300%)

- DeFi Summer and NFT frenzy pushed altcoins to gains of 10-100x普遍.

2024-2025 Bull Market: Transmission Mechanism Failure

- BTC rose significantly from its low to $125,000 (+78%+)

- ETH gains limited, hovering around $2,800

- Altcoins collectively flatlined, even falling further as BTC hit new highs

The core difference is clear: In 2025, BTC's gains no longer "spill over" to ETH and altcoins. Capital seems trapped behind an invisible wall within the BTC ecosystem. The name of that wall is "institutionalization".

II. Underlying Mechanisms: How Institutional ETFs "Rewrite the Rules of the Game"

2.1 BTC Becomes a "Shadow of US Tech Stocks"

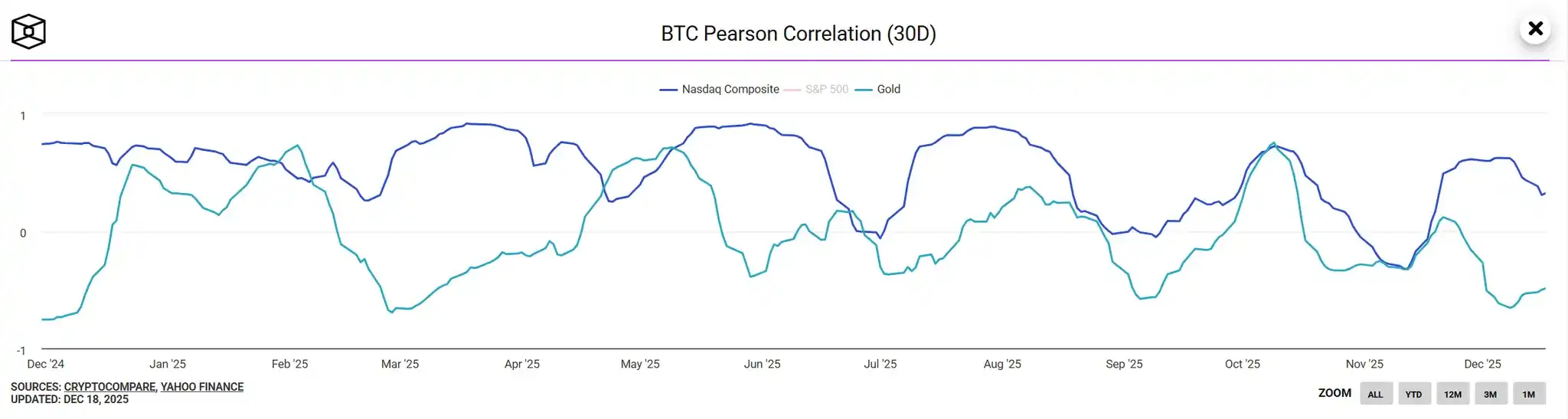

Chart: 30-day correlation coefficient between BTC and Nasdaq/Gold

In January 2024, the US SEC approved spot BTC ETFs, marking the crypto market's entry into the "institutional era." However, a side effect of this milestone is BTC gradually detaching from crypto-native narratives and becoming a "satellite asset" of traditional finance.

High Correlation with Nasdaq

In 2025, the 30-day correlation coefficient between BTC and the Nasdaq 100 index remained stable in the 0.75-0.85 range, hitting a record high; its correlation with gold dropped below 0.2. When US tech stocks (like Nvidia, Tesla) surged, BTC ETF inflows accelerated; when US stocks corrected, BTC fell in sync.

Essential Shift: BTC is no longer "digital gold" (safe-haven asset), but "digital tech stock" (risk asset). Its pricing power has shifted from crypto natives to Wall Street fund managers.

"One-Way Siphoning" Effect of Institutional Buying

Clients of traditional asset management giants like BlackRock and Fidelity (pensions, family offices, high-net-worth individuals) only recognize BTC, not altcoins. The reason isn't a deep understanding of crypto technology, but a trifecta of "regulatory compliance + sufficient liquidity + brand recognition":

- BTC has SEC-approved spot ETFs.

- BTC has CME futures and a well-developed derivatives market.

- BTC has 15 years of brand accumulation.

In contrast, altcoins are still "unidentified assets" in the eyes of institutions,叠加 regulatory risk, liquidity risk, and project risk,根本无法 passing traditional financial due diligence.

Structural Solidification of Capital Flows: In 2025, of the hundreds of billions flowing into BTC ETFs, over 95% was locked within the BTC ecosystem, with less than 5% flowing into ETH/altcoins via OTC trades or DeFi bridges. This starkly contrasts with the past "capital spillover effect".

MicroStrategy's "Infinite Ammo" Model

Michael Saylor's MicroStrategy has become another dominant force in the BTC market. By issuing convertible bonds, secondary offerings, etc., the company continuously buys BTC, currently holding about 670,000 BTC (cost ~$30 billion).

More crucially, MSTR's stock price has long traded at a 2-3x premium to the value of its held BTC, making it a proxy tool for retail investors to "leveraged long BTC". A positive feedback loop is thus formed:

MSTR stock price rises → Market cap膨胀 → Ability to issue debt increases → Buys more BTC → Pushes BTC price higher → MSTR stock price rises again

This "corporate hoarding" model further siphons capital that could have flowed into altcoins, strengthening BTC's dominance.

2.2 Why Did ETH "Fall Behind"? Layer 2's "Vampire Attack"

Ethereum's weak performance is not only due to lack of institutional interest but also internal contradictions within its own ecosystem.

Layer 2's Liquidity Fragmentation Dilemma

The TVL (Total Value Locked) of Layer 2 networks like Arbitrum, Optimism, Base, zkSync has exceeded tens of billions,接近 60% of the mainnet's. But the problem is, the tokens of these L2s (ARB, OP, etc.) do not adequately capture value for ETH, instead diverting users and capital.

Core Contradiction: When users transact on L2s, the Gas fees paid are in L2 tokens or stablecoins, not ETH. The economic model of L2s is structurally decoupled from the ETH mainnet—the more successful L2s are, the lower the demand for ETH. This is a classic "vampire attack".

Staking Yield's "Prisoner's Dilemma"

After transitioning to PoS, ETH staking offers an annual yield of ~3-4%. Although liquid staking derivatives (like Lido's stETH) account for a significant portion of the total stake, this has not pushed the ETH price higher.

Paradox: Staked ETH is locked, reducing circulating supply (theoretically bullish for price), but it also reduces speculative demand (actually suppressing price). ETH has been downgraded from "programmable money" to "interest-bearing bond", but its 3-4% yield cannot compete with US Treasuries at 4.5%, let alone attract crypto investors seeking high returns.

Narrative Vacuum Lacking Killer Apps

The DeFi Summer and NFT frenzy of 2021 made ETH synonymous with the "world computer". But in 2025:

- DeFi TVL halved from its peak.

- NFT trading volume crashed 90%.

- Emerging applications like AI Agent, on-chain games have not yet achieved scale.

The narrative contrast is stark: BTC has a clear positioning as "digital gold + institutional allocation", Solana has market consensus as "high-performance公链 + Meme culture", while ETH's positioning is模糊—not "hard currency" enough, nor "sexy" enough.

2.3 Altcoins' "Liquidity Black Hole"

If BTC is the "empire on which the sun never sets", and ETH is having a "midlife crisis", then altcoins are experiencing a true "twilight of the gods"—former star projects are falling, new projects are stillborn.

VC Coins' "High FDV Low Float" Death Trap

In 2024-2025, many VC-backed projects launched with extremely high valuations (FDV often $1-5 billion), but with only 5-10% circulating supply. This model is doomed:

- Retail investors buy at high prices.

- VC and team unlock selling pressure持续 for 1-3 years.

- Prices grind lower long-term, even valuable projects can't escape.

Typical case: A知名 Layer 1 project launched with FDV $3 billion, circulating market cap only $300 million. 6 months later, price down 80%, FDV still $1 billion—valuation still inflated, but retail investors are wiped out.

Meme Coins' "Ponzi Game" and Market Fatigue

In 2025, Meme coins on Solana (like BONK, WIF, POPCAT) briefly attracted capital, but are "zero-sum games"—early players harvest later players. Lacking real value支撑, 90% of Meme coins go to zero within 3 months.

More serious is the market fatigue effect: After being "harvested" repeatedly (2022 Terra collapse, FTX bankruptcy, 2024-2025 VC coin暴雷), retail investors gradually远离 the altcoin market,形成 a psychological trauma of "once bitten, twice shy".

CEX's "Liquidity Drought" and Death Spiral

Altcoin trading volume on top exchanges like Binance, Coinbase暴跌 over 70% compared to 2021; smaller exchanges are closing down浪潮. Reasons include:

- Regulatory Pressure: SEC's ongoing lawsuits against Binance, Coinbase.

- User Loss: Shift to compliant products like BTC ETFs.

- Declining Project Quality: Bad money drives out good.

Low liquidity leads to increased price volatility (order book depth for a 10% move might be less than $100k), further scaring away investors, forming a death spiral: "liquidity dries up → price crashes → investors leave → liquidity dries up further".

Narrative Exhaustion and Homogeneous Competition Dilemma

2017 had ICOs, 2020 had DeFi, 2021 had NFTs and Metaverse, 2024 had AI and RWA... but 2025 has no new narrative真正 igniting the market.

Existing sectors (Layer 1, Layer 2, DeFi, NFT) are highly saturated, projects are heavily homogenized, users cannot distinguish good from bad. Final result: Capital doesn't know where to invest, so it just "parks" in BTC.

III. Institutional Perspective: Grayscale and CoinShares' 2026 Predictions

3.1 Grayscale Report: Dawn of the Institutional Era and a Tiered Landscape

Grayscale, in its 《2026 Digital Asset Outlook: Dawn of the Institutional Era》, clearly states the crypto market is entering a new phase dominated by traditional finance.

BTC: Irreversible Institutionalization Process

Grayscale expects 2026 to accelerate the shift in digital asset investment structure, driven by two main themes:

- Macro Demand for Alternative Store-of-Value Assets: Ongoing fiscal imbalances, inflation risks, and global money supply growth drive demand for BTC and ETH as scarce digital commodities.

- Increasing Regulatory Clarity: Expect more countries to approve crypto ETP products; US might pass bipartisan market structure legislation, further integrating blockchain finance.

Key catalysts include:

- The 20 Millionth Bitcoin即将 Mined: The 20 millionth BTC (out of 21 million) will be mined in March 2026, a milestone reinforcing BTC's fixed supply transparency and scarcity narrative.

- Rising Institutional Allocation: US state pensions, sovereign wealth funds (like Harvard Endowment and UAE's Mubadala have already started) will gradually increase BTC allocation from current <0.5% to higher levels.

- Hedge Against USD Devaluation: Amid soaring US debt and global de-dollarization trend, BTC's hedging属性 as "digital gold" becomes more prominent.

Grayscale predicts BTC could hit a new all-time high in H1 2026,突破 $150,000 as a base case.

ETH: "Sideways Accumulation" Amid Painful Transformation

Grayscale直言 ETH is undergoing a "painful transformation", needing time to adapt to institutional adoption and regulatory standards. Three转型 directions include:

- Deep Binding of Layer 2 and Mainnet: Through economic model improvements (like further evolution of EIP-4844), making L2 success truly benefit ETH value.

- Institutional-Grade DeFi/RWA Apps: Scaling compliant use cases like tokenized bonds, on-chain asset management.

- Mass Consumer Adoption: On-chain social, gaming apps breaking out of "small circles".

But these transformations need 1-2 years to verify. Grayscale predicts 2026 is more likely a "sideways accumulation" phase for ETH, with relatively limited price gains, far from replicating the explosive growth of 2017 or 2021.

Altcoins: Tiered Fate and Survival of the Fittest

The report emphasizes "Not all tokens will successfully transition out of the old era", altcoins will show clear stratification:

Tier 1: Quasi-Institutional Grade Assets

- Representatives: Solana, Avalanche, Polygon

- Characteristics: Real users, institutional backing, regulatory path.

- Expectation: May attract some institutional capital, but gains far inferior to BTC.

Tier 2: Ecosystem & Utility Tokens

- Representatives: DeFi protocols (Aave, Morpho, Uniswap), AI chains (Bittensor, Near)

- Characteristics: Benefit from real use case growth, have cash flow支撑.

- Expectation: Limited upside, but can survive in the "utility era".

Tier 3: Speculative Tokens

- Representatives: Meme coins, purely narrative projects, high FDV low float VC coins.

- Characteristics: Lack practical utility, rely on retail FOMO.

- Expectation: High probability of归零 or marginalization.

Grayscale clearly states the "普涨时代 universal rising tide era" for altcoins is彻底 over, the traditional four-year halving cycle is瓦解, replaced by more stable institutional capital inflows. Only projects with sustainable revenue, real users, and a regulatory path will survive; the rest will disappear in the "survival of the fittest".

3.2 CoinShares: From Speculation to Utility, "Hybrid Finance" Defines the Future

CoinShares' 《Outlook 2026: Toward Convergence and Beyond》 report proposes a more radical view: 2025 is the last year of speculation-driven markets, 2026 will shift towards utility, cash flow, and integration.

The Rise of "Hybrid Finance"

CoinShares introduces the "Hybrid Finance" concept: deep integration of public blockchains with traditional financial systems, creating new infrastructure neither can build alone. The core story for 2026 is "convergence":

1. Traditional Institutions Building on Public Chains:

- BlackRock issuing on-chain money market funds (BUIDL)

- Franklin Templeton launching tokenized treasuries

- Banks like Citi, HSBC conducting bond issuance on private chains

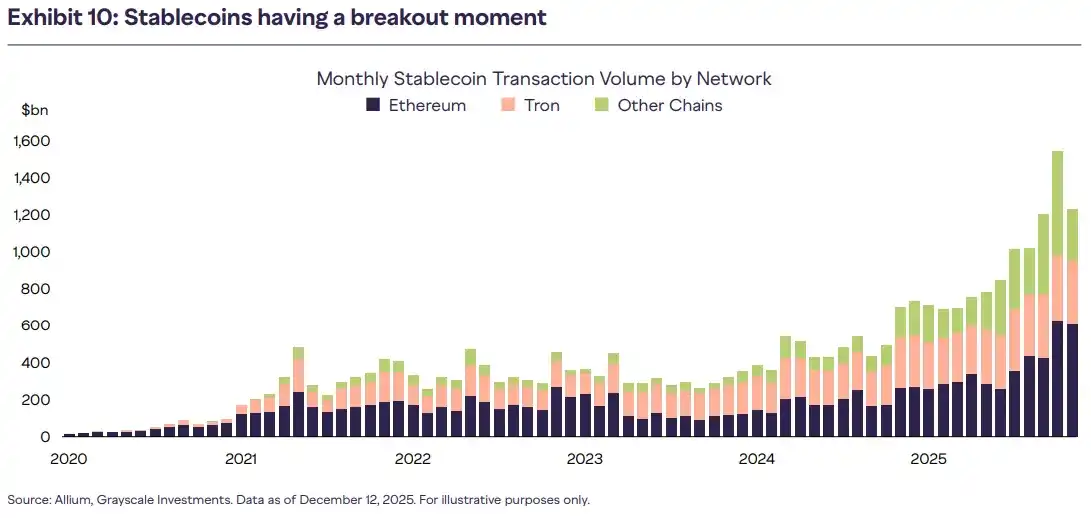

2. Stablecoins Shift from Crypto Tool to Global Payment Rail:

- Regulatory frameworks like US GENIUS Act, EU MiCA provide green lights.

- After Stripe acquires Bridge, businesses can integrate stablecoin payments directly via API.

- Stablecoin market cap moves from $200B towards $500B.

3. Tokenization Explosion:

- Private credit, tokenized treasuries dominate the market.

- On-chain products offer faster settlement, lower cost, global distribution.

- RWA (Real World Asset) market cap expected to突破 $50 billion in 2026.

4. Value Capture Era:

- Apps like Hyperliquid use revenue to buy back/burn tokens.

- Tokens upgrade from "governance tools" to "equity-like assets".

- Cash flow and fundamentals become core valuation metrics.

Institutional Dominance and Disappearing Retail FOMO

CoinShares points out that 2025 BTC ETF inflows exceeded $90 billion, showing institutional mainstreaming is irreversible. Meanwhile, retail FOMO sentiment has significantly weakened due to past trauma, narrative fatigue, and regulatory uncertainty. Retail capital chooses to观望 or is limited to mainstream assets like BTC.

2026 Price Scenario Predictions

CoinShares provides three scenarios based on macro environment:

- Soft Landing (Base Case): BTC突破 $150,000, ETH follows limitedly, quasi-institutional altcoins rise moderately.

- Stable Growth: BTC maintains in $110,000-$140,000 range, market volatility decreases.

- Stagflation/Recession: Short-term pressure but medium-term recovery, BTC's "digital gold" attributes highlighted.

Core Predictions:

- BTC's dominance rises further to over 65% (currently 59-60%).

- Institutions dominate pricing power, retail influence marginalized.

- Liquidity concentrates towards utility projects; only projects with "real users + real revenue + compliance path" win.

- 90% of existing altcoins will be eliminated, market completes "natural selection".

Ultimate Judgment: CoinShares believes 2026 is not about digital assets "challenging" traditional finance, but becoming part of mainstream finance. Utility wins, hybrid finance defines the future, the crypto market will transform from "disruptor" to "integrator".

IV. Core Question: Has the Four-Year Cycle Really Ended?

4.1 The Nature of the Cycle: From "Supply-Driven" to "Demand-Driven"

The past four-year cycle was essentially a supply-driven model:

Classic Transmission of Halving Effect: BTC halving → Miner selling pressure reduces → Supply contracts → Price rises → Triggers FOMO → Retail floods in → Capital spills over to ETH → Spills over further to altcoins.

Cyclical Entry of New Capital: Each bull market had new capital sources (2017 ICO retail, 2021 DeFi/NFT players & pandemic money printing潮), this capital followed the natural flow path "BTC→ETH→altcoins".

2025 Structural Change: Demand-Side Restructuring

However, in 2025, the demand side changed fundamentally:

- Institutional Capital's "Directed Demand": Only buys BTC, not altcoins, preventing capital "spillover".

- Retail FOMO's "Permanent Absence": After the 2022 crash, retail lost confidence in altcoins, dare not chase even as BTC hits new highs.

- Solidification of Liquidity Tiers: The liquidity pools of BTC, ETH, and altcoins are彻底割裂 split, capital cannot flow freely as before.

Conclusion: The "halving → BTC rise → altcoin rotation" logic of the four-year cycle hasn't ended, but its transmission mechanism has been interrupted by institutionalization. Future cycles might be "lame bull markets" of "BTC rises alone → ETH barely follows → altcoins continue to languish".

4.2 Do Altcoins Have a Future?

The answer is: Most altcoins have no future, but a few sectors still have room to survive.

Altcoin Types With No Future

- High FDV Low Float VC Coins: Inherently flawed economic model, retail is always the bag holder.

- Meme Coins with No Practical Use: Except for a few "cultural symbols" (like DOGE, SHIB), most will go to zero.

- Homogeneous Layer 1/Layer 2: The market only needs 3-5 major公链 (ETH, Solana, BNB Chain, etc.), the rest are "zombie chains".

The crypto market in 2025 is undergoing a painful but necessary "rite of passage"—transitioning from a retail-dominated casino to an institution-dominated asset allocation market.

Bitcoin's "never-setting sun" is not a victory for crypto, but the "taming" of crypto by traditional finance. When BTC becomes a "shadow of US tech stocks", it gains liquidity and compliance, but loses its original intention of "decentralized money". This is progress, but also compromise.

The altcoins' "twilight of the gods" is not an end, but the eve of rebirth. When the bubble bursts and bad coins are purged, truly valuable projects will rise from the ashes. History always rhymes—every bubble破裂孕育 the seeds of the next era.

The four-year cycle has not ended; it has merely changed its face. Future bull markets may no longer be a狂欢 of "all coins rising together", but a残酷竞赛 of "the strong get stronger, the weak get eliminated". In this race, those who understand the new rules, embrace institutionalization, and adhere to value investing will have the last laugh.

Data for this report was compiled and edited by WolfDAO. Please contact us if you have any questions for updates;

Author: Nikka / WolfDAO( X : @10xWolfdao )