Author: Claude, Deep Tide TechFlow

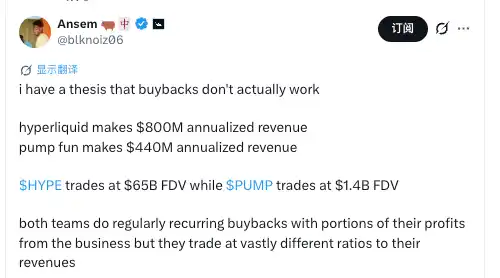

Deep Tide Introduction: Famous Solana trader Ansem posted that the buyback mechanism itself does not create value, and what determines the token valuation multiple is the "trust premium" between the team and the community. Using Hyperliquid (annualized revenue approx. $8 billion, FDV approx. $65 billion) and pump.fun (annualized revenue approx. $440 million, FDV only approx. $1.4 billion) as a comparison, he pointed out that both are conducting large-scale buybacks, but their valuation multiples differ by nearly 50 times.

One of the most enduring narratives in the crypto market is being challenged: dumping protocol revenue into buybacks will make the token price rise.

On July 16, famous Solana trader Ansem (@blknoiz06) posted a long thread on platform X, proposing a counterintuitive argument: the buyback mechanism itself does not create value; what truly determines the token trading multiple is the "trust premium" between the team and the community. This post quickly gained over 469,000 views, 3,240 likes, and 509 reposts.

Ansem selected two of the crypto industry's highest-earning protocols for comparison. Hyperliquid's annualized revenue is approximately $8 billion, HYPE's FDV is approximately $65 billion; pump.fun's annualized revenue is approximately $440 million, PUMP's FDV is only about $1.4 billion. Both teams are using the vast majority of their revenue for buybacks, but their valuation multiples differ by nearly 50 times.

Ansem's conclusion is: the gap is not in the scale of revenue, but in the trust accumulated through the team's actions.

Both Spending Heavily on Buybacks, Why Do Hyperliquid and pump.fun Have Such Widely Different Valuations?

Ansem deconstructed the buyback strategies of the two platforms in his post.

Hyperliquid directs 97% to 99% of protocol fees directly into HYPE buyback and burn. According to CryptoNews data, as of June 30, Hyperliquid's cumulative protocol revenue had exceeded $1 billion, with an annualized run rate close to $840 million. The platform has burned over 41 million HYPE tokens, worth over $1 billion, reducing the circulating supply by approximately 4.2%. At the time of writing, HYPE is quoted around $60 to $67, with an FDV of approximately $57 to $62 billion.

pump.fun is similarly aggressive. In 2025, the platform's total revenue was approximately $970 million, and it invested close to 100% of revenue into PUMP buybacks, accumulating about $213 million in buybacks. In April 2026, the team executed a one-time burn of PUMP tokens worth $370 million (about 36% of the circulating supply) and locked 50% of subsequent revenue for continuous burns. However, PUMP is currently quoted around $0.0016, with an FDV of approximately $1.4 to $1.7 billion.

pump.fun's annualized revenue is a bit more than half of Hyperliquid's, but its FDV is less than 3% of Hyperliquid's. If the buyback mechanism were the core driver of valuation, this multiple gap would be unexplainable.

Ansem's Explanation: Trust Premium is the Core of Pricing

Ansem believes the high valuation the market gives Hyperliquid stems from the trust established by Jeff (Hyperliquid founder) and his team.

He listed several points in his post: Hyperliquid has never overpromised; the team focuses solely on shipping products; user rewards are strictly distributed based on pre-determined on-chain metrics without opaque operations; the core user base has an extremely high trust rating for Jeff and the team. Ansem's original words stated that this trust premium "is one of the main reasons the token is trading so well."

Hyperliquid's historical actions support this judgment. The project did not accept VC investment, allocating 70% of the total supply to the community; the massive airdrop at launch in November 2024 fulfilled early promises; the platform showed resilience during the market sell-off in February 2026, indicating its user base includes many serious traders who rely on the platform for daily trading.

The pump.fun Problem: $1 Billion in Revenue, Promised Airdrop Unfulfilled for a Year

Ansem's criticism of pump.fun is more direct.

He pointed out that pump.fun has accumulated over $1 billion in revenue, raised another $1 billion in its ICO, but the airdrop promised to users has never been delivered. According to a Protos report, pump.fun clearly stated "airdrop coming soon" when announcing the PUMP token ICO on July 9, 2025, promising to allocate 24% of the supply to the community. By mid-July 2026, this promise has been outstanding for a full year, with no airdrop in sight.

Ansem had previously criticized this on June 25: "pump.fun is the only application in crypto that has sustained attention for several years, not even OpenSea achieved that. But people are angry because they promised a 24% airdrop and never delivered, just sitting on the cash now."

The $370 million token burn in April 2026 was intended to repair trust, but the community reaction backfired. Some users believed the burned tokens should have been used for the airdrop allocation, and burning them directly eliminated the community's deserved share. According to a Cryptopolitan report, the widespread community interpretation of this move was that it "deepened distrust."

In his latest post, Ansem made a hypothetical scenario: if pump.fun seriously fulfilled its airdrop promise and addressed the concerns of its core users, the token price could potentially increase 10 to 15 times, while trading volume, attention, and platform revenue would also see substantial growth.