Article Author: Thejaswini M A

Article Translation: Block unicorn

Preface

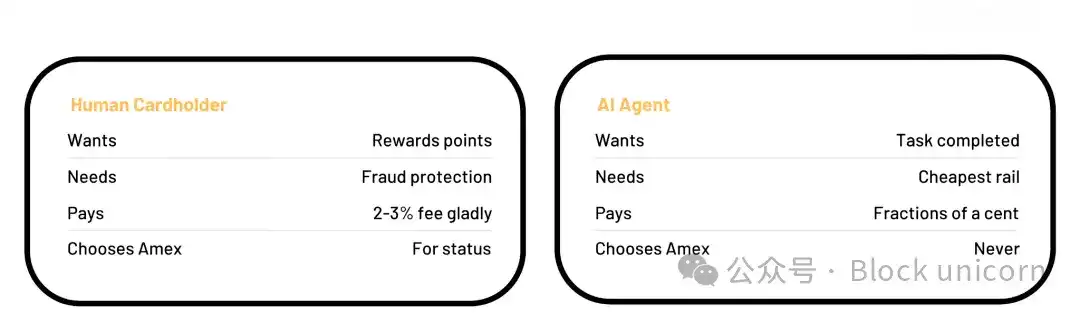

Visa's entire business model is a bet on human behavior. It's about human consumption and psychology. The reward points you accumulate, the fraud protection you rely on, the Centurion card you dream of, and the zero-liability policy that makes you feel secure when swiping your card at an ATM abroad—all of these exist not because transferring funds is difficult, but because humans are anxious, status-seeking, and not good at reading terms and conditions. Visa has exploited this cognitive gap to build a $500 billion company.

However, AI agents do not possess these traits.

They do not accumulate points, do not seek fraud protection, and do not desire a black card. They have only one instruction: complete the task. And when the task involves payment, the agent performs complex calculations that humans would never bother with: the cheapest path, the fastest settlement, the lowest fees. Every time, automatically, without any emotion.

Last month, an article on SubStack titled "The 2028 Global Intelligence Crisis" caused Visa's stock to plummet 4% in a single day, Mastercard to fall 6%, and American Express to drop 12%. The report was labeled a "scenario analysis," not a "prediction" (原文如此). But the market didn't buy it. The technical arguments were also irrelevant. The point is that by 2027, agents will bypass transaction centers and use stablecoins for settlement. Visa spent fifty years perfecting its product, and now its customer base is being replaced.

In machine-to-machine commerce, a 2-3% interchange fee is clearly a target. This argument from Citrini Research is its core thesis. This does not mean that AI will destroy Visa tomorrow. Rather, the fee structure upon which Visa built its commercial empire is essentially a tax on human irrational behavior, and the transactors themselves are completely rational. This is the very reason for Visa's existence.

What is Visa Selling?

To understand why this matters, you must know what interchange fees are actually used for.

When you use a credit card to make a purchase, the merchant pays a 2-3% fee to the credit card network and your issuing bank. This fee pays for your reward points, fraud protection, purchase insurance, and dispute resolution services. The entire consumer value proposition of the credit card is borne by the merchant, who ultimately passes the cost on to the consumer through slightly higher prices. This is a well-established and stable system that has worked for fifty years because the consumer in the transaction is willing to bear all these costs, albeit not directly.

AI agent does not need these. It will not dispute charges or request refunds. The justification for charging this fee is that it protects against human error, fraud, and impulsive behavior. If there is no human involved in the transaction, this fee becomes completely meaningless.

American Express is the most典型 example of this problem. Its customers are high-income, high-spending, and aspirational premium cardholders. Its annual fee is higher than Visa's or Mastercard's precisely because its customers are willing to pay for status and privilege. This model presupposes that purchasing behavior is human-driven, that customers choose Amex over Visa because lounge access is worth it. An agent will not actively choose Amex; they will only look for the cheapest option to complete the transaction. In a world where software controls credit cards, premium membership tiers do not exist.

An agent-led commercial routing model that bypasses interchange fees poses a greater risk to credit card banks and mono-line issuers that rely heavily on 2-3% fee revenue and have built their entire business segments around merchant-subsidized reward programs. Visa and Mastercard have network businesses that can adapt. Those issuers who have built their entire P&L model around interchange fees and reward programs have nowhere to retreat.

The Week Everyone Shipped at Once

The Citrini report and infrastructure project launches happened to be released within the same three weeks.

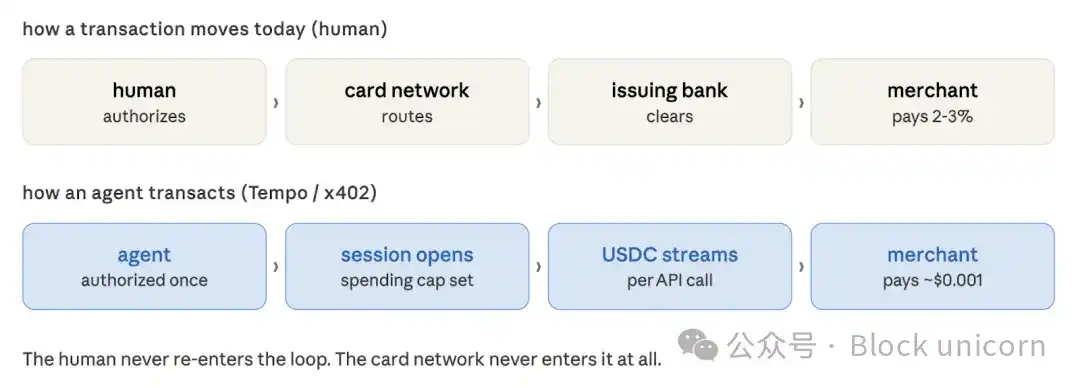

Tempo officially launched its mainnet last Wednesday. The payment blockchain jointly developed by Stripe and Paradigm, designed for high-volume stablecoin settlement, was launched同步ously with the Machine Payable Protocol (MPP). MPP is an open standard that allows AI agents to autonomously pay for services without manual approval for each transaction. The protocol introduces session mechanics. An agent authorizes a spending limit once and can then make continuous micropayments for services like data consumption, computation, or API calls. Funds are paid using OAuth authentication. The user authorizes a budget, and the agent spends. The entire process does not require a bank card at every step.

Anthropic, DoorDash, Mastercard, Nubank, OpenAI, Ramp, Revolut, Shopify, Standard Chartered, and Visa are listed as design partners for Tempo. The entire payment and e-commerce ecosystem has acknowledged this structural change.

On the same day Tempo launched, Visa's cryptocurrency division launched a command-line interface tool for AI agents to make payments through the terminal, without API keys, without accounts, and without human authorization. Visa calls this "command-line commerce"—machines transacting without human intervention.

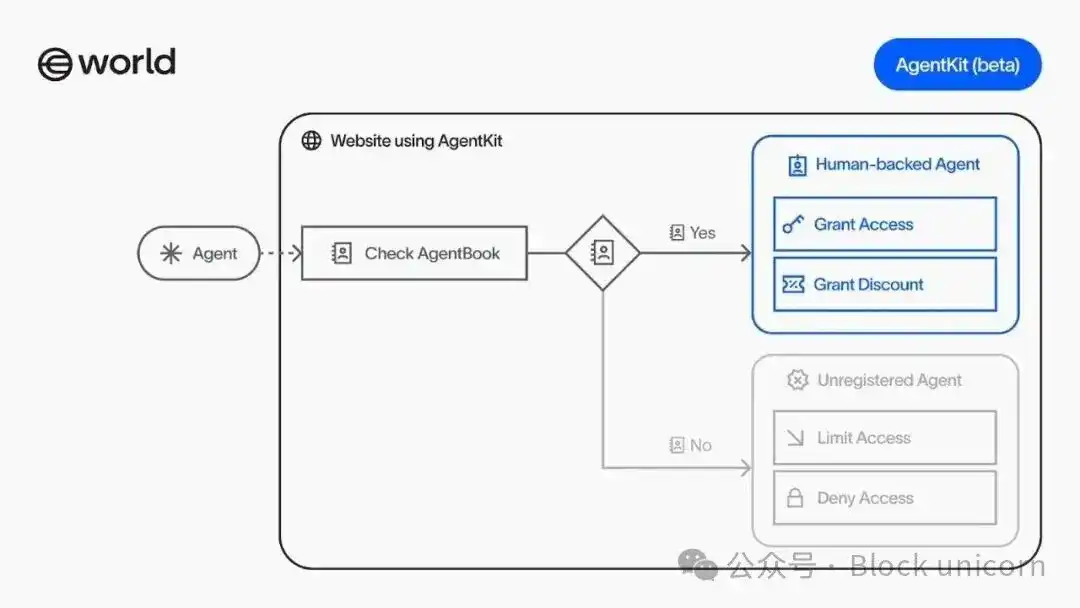

Mastercard agreed to acquire stablecoin infrastructure startup BVNK for $1.8 billion. Circle launched Nanopayments on the testnet, a sub-cent, gas-free USDC transaction designed for agents using pay-per-use APIs without accounts or credentials. Sam Altman's World project launched AgentKit, allowing agents to carry cryptographic proofs to demonstrate they represent a real person; the toolkit integrates directly into Coinbase's payment system, enabling platforms to verify agent identity without hindering legitimate transactions.

What happened last week, in my view, is that companies are racing to become the new Visa, lest Visa realizes what it has lost.

The Obvious Paradox

Let's be perfectly clear: Visa is not standing still.

It is involved in the development of Tempo's Machine Payable Protocol (MPP), has launched Visa Crypto Labs, and its head of cryptocurrency wrote an article in Fortune explaining how agents can use bank card payments through new standards. Mastercard is investing $1.8 billion in stablecoin infrastructure. Stripe acquired Bridge and Privy. The incumbents are aware of this shift and are preparing before the new infrastructure fully arrives.

Visa's argument is that it can extend its rails to agent-driven commerce before agent-driven commerce builds rails that make Visa irrelevant.

This argument is not entirely wrong. Stripe processed $1.9 trillion in payment volume in 2025, a 34% year-on-year increase. These companies are not shrinking. The network distribution advantages of card organizations are difficult to replicate. I admit I am reluctant to say this publicly because historically, as soon as someone makes this argument, a new product is launched that makes them look foolish.

So, here is the flaw in the argument: Visa's distribution advantage is built on relationships with merchants and consumer trust. Merchants accept Visa because consumers hold Visa; consumers hold Visa because merchants accept Visa. The entire flywheel runs on people. Once agents become the primary buyers in a significant area of commerce, this flywheel slows down. Agents have neither brand loyalty nor wallets. They only have budgets and instructions. Whichever route is cheapest and fastest wins their business, with zero switching costs.

I want to be precise about where we are because the narrative is currently moving faster than the data.

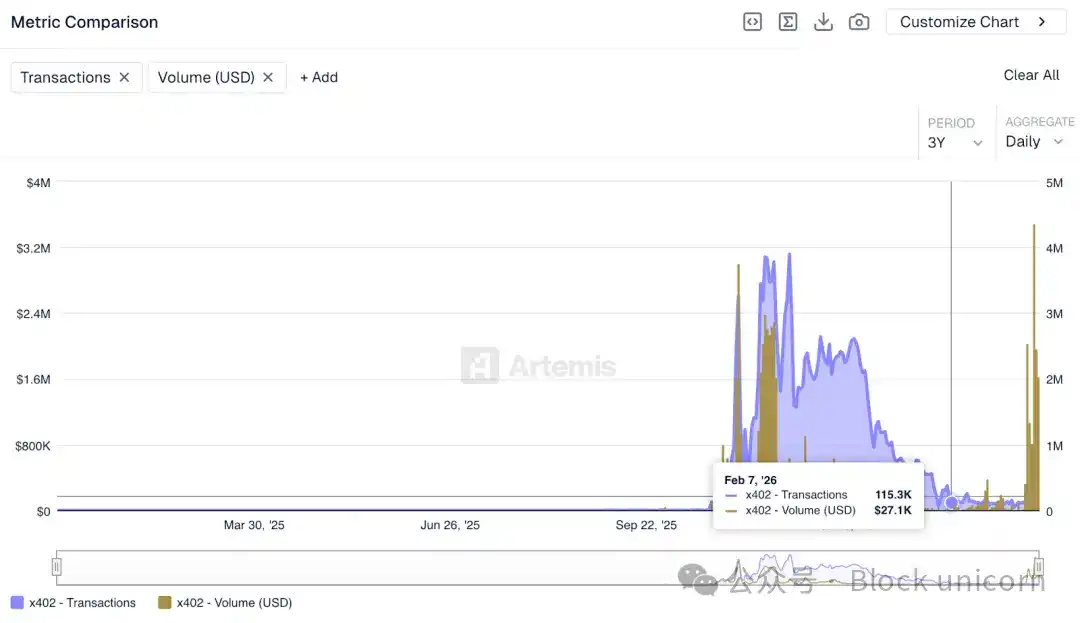

Although the ecosystem around x402 is valued at approximately $7 billion, on-chain data shows that the protocol's daily transaction volume last week was only around $28,000, most of which came from testing rather than actual transactions. This figure is a world away from Visa's daily transaction volume.

x402's transaction count has exceeded 50 million. Although the amount per transaction is small, the number of transactions indicates that the infrastructure is being used. Developers are building on it. The merchant-side services that accept agent payments are also growing. This is how payment networks start.

McKinsey estimates that by 2030, AI agents could facilitate $3 trillion to $5 trillion in global consumer transactions. This estimate may be correct or overly optimistic. But it is indisputable that agent-driven business models are not yet widespread at scale. The merchants building native agent services, the businesses using agents as primary buyers, and the transaction volumes that can truly test the economics are still developing.

The Citrini report caused market panic because it模拟ulated a series of credible events. Mastercard's Q1 2027 earnings report will not attribute a slowdown in transaction volume to "agent-led price optimization." At least not yet.

The first to be affected will be micropayments for AI infrastructure, not consumer commerce.

An agent completing a research task calls specialized data APIs hundreds of times per session. Each call costs a fraction of a cent. Over a week, these calls could generate $40 in revenue for the developer operating the service. Credit card networks cannot handle this. The economics of minimum transaction amounts don't work. The merchant onboarding process doesn't work. The fee structure doesn't work. This type of business model is destined not to work within Visa's framework. It requires a completely new model, and x402, Nanopayments, and Tempo are building it.

As Citrini's model shows, the disruption of consumer commerce, if it happens, will come later. It requires agents to handle a significant portion of discretionary spending, which in turn requires consumers to trust agents enough to let them make purchasing decisions that they currently make themselves.

Visa is being冲击ed by better customers. These customers no longer need the elements upon which Visa's success was built. The 2-3% interchange fee is not a transaction tax; it is a tax on the irrationality of human nature. And agents are perfectly rational.

How do I know this matters? Because Visa spent $1.8 billion last week to ensure it is not left out of the answer.