Author: YettaS, Investment Partner at Primitive Ventures

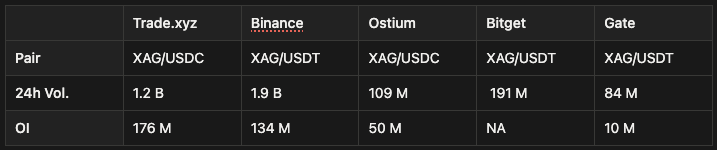

As gold and silver continue to hit new highs, Trade.xyz's daily trading volume approaches $2 billion, and Binance lists TSLA perpetual contracts with little hesitation, the trend is hard to ignore: Traditional financial assets are becoming the new gateway for the crypto market to absorb global liquidity.

Just a year ago, most CEX operators probably couldn't accept this fact: An on-chain trading venue is actually using TradFi assets as a wedge to begin eroding and reshaping the core territory of centralized exchanges.

We all know that crypto capital inherently prefers volatility; from a product structure perspective, equity perps are precisely at the convergence point of several key upgrades, which is the fundamental reason they stand out in this cycle:

-

As CBOE / CME gradually accept crypto in-kind margin this year, the liquidity and availability of crypto assets as collateral will significantly improve.

-

Once the DTCC establishes a direct on-chain connection, the settlement layer will begin to permeate on-chain, and stock assets will gain a native on-chain settlement channel from the source.

-

The truly interesting part then emerges: Tokenized stocks as collateral → Perpetual contract exchanges accept them → Institutions begin systematic basis farming.

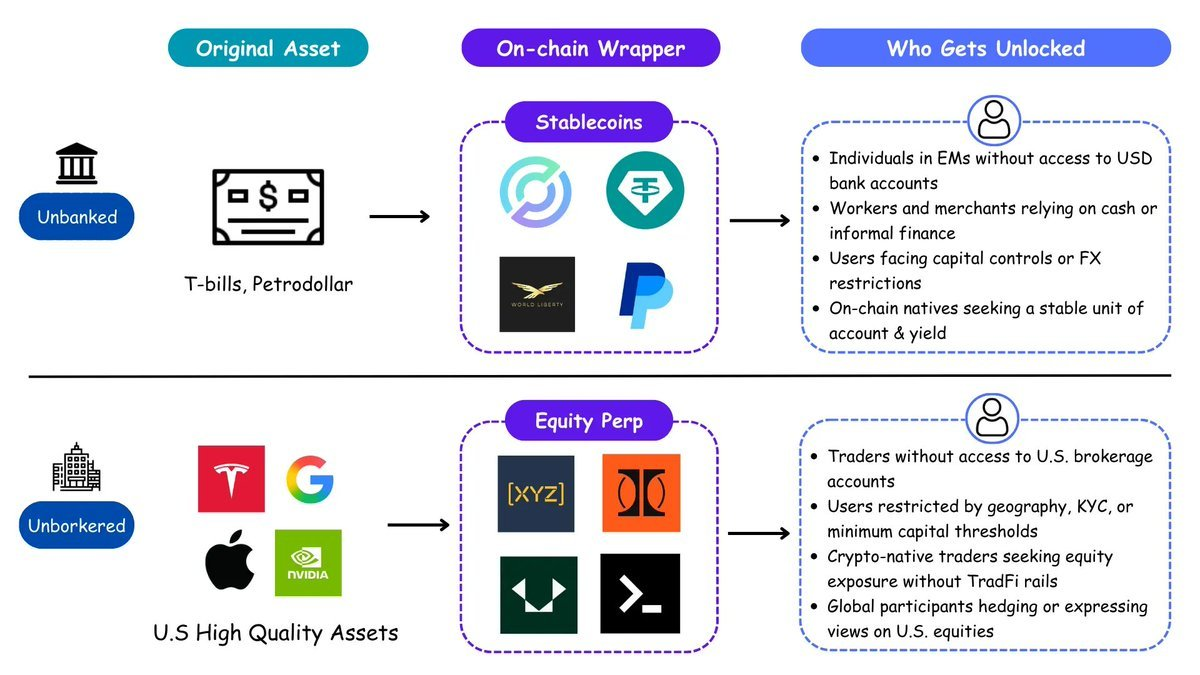

Onshore Issuance, Offshore Distribution

The U.S. exports finance not by exporting financial institutions themselves, but by exporting "access." The petrodollar system distributed dollars globally, externalizing inflationary pressure; stablecoins replicated this logic by wholesale purchasing of U.S. Treasuries, turning the whole world into new dollar holders without the need for banks or brokers. On-chain stocks are the next step in this logic. From unbanked to unbrokered, dollar assets will once again complete their global倾销 (dumping).

CEXs saw the opportunity and potential threat early on, so they chose to expand first. Ondo and xStocks focused on the issuance side—connecting with brokers, custodying real stocks, minting 1:1 tokenized stocks on multiple chains—but it turned out that issuance itself doesn't automatically create a market.

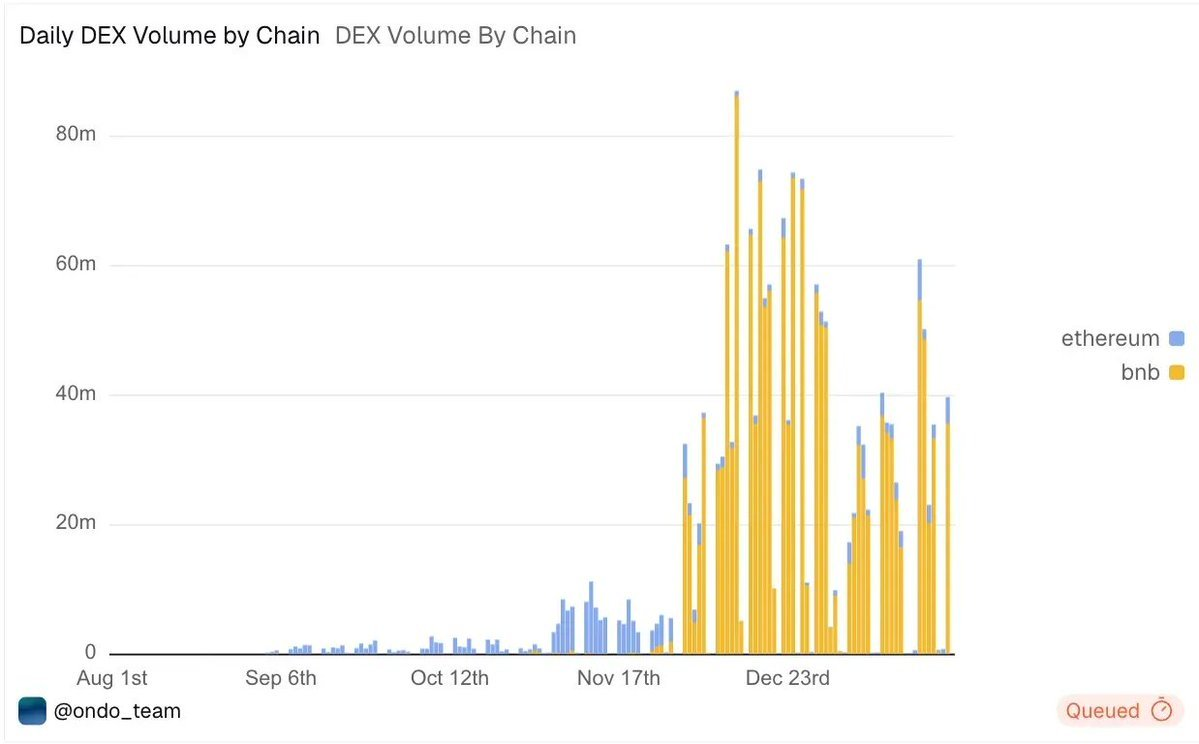

The first wave of real demand came from traders unable to access the U.S. brokerage system and crypto-native users seeking exposure to U.S. stocks without relying on TradFi infrastructure. The issuers handled the heaviest compliance and custody work, but the flow of funds went to the side that truly controls trading attention and distribution capabilities. Offshore platforms embedded the products directly into their trading interfaces, and trading volume naturally aggregated there. Ultimately, we see the vast majority of tokenized stock trading volume concentrated on BNB Chain, accounting for over 80%.

If offshore spot unlocked retail demand, on-chain equity perps further attracted the flow of professional traders. These users are global trading participants who want to trade or hedge U.S. stocks without being constrained by broker access, trading hours, or jurisdictional limits.

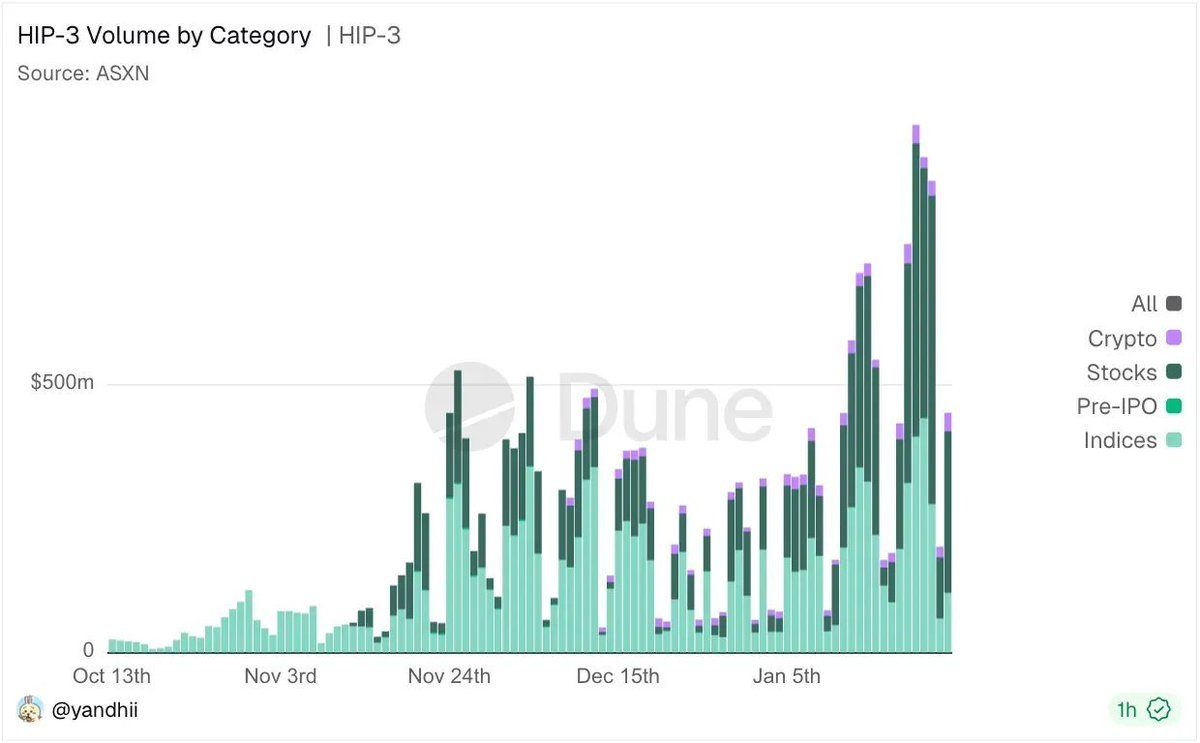

Take HIP-3 as an example; it provides professional traders with a trading interface to systematically conduct basis trading, capture cross-market dislocations, and cover stocks, crypto assets, and indices simultaneously. With the叠加 (overlay) of potential airdrop incentives, trading volume continues to刷新 (refresh) new highs.

The Golden Window for On-Chain Stock Perpetuals

Once a现货锚点 (spot anchor) exists, perpetual contracts almost always become the most efficient trading tool, for reasons that are as direct as ever:

-

7×24 hour trading,不受 (not subject to) market hour restrictions

-

Cross-margin with all assets, extremely capital efficient

-

High leverage allows true risk appetite to be释放 (released)

-

Composable into DeFi strategies

-

Provides a clear collateral path for RWA / tokenized assets

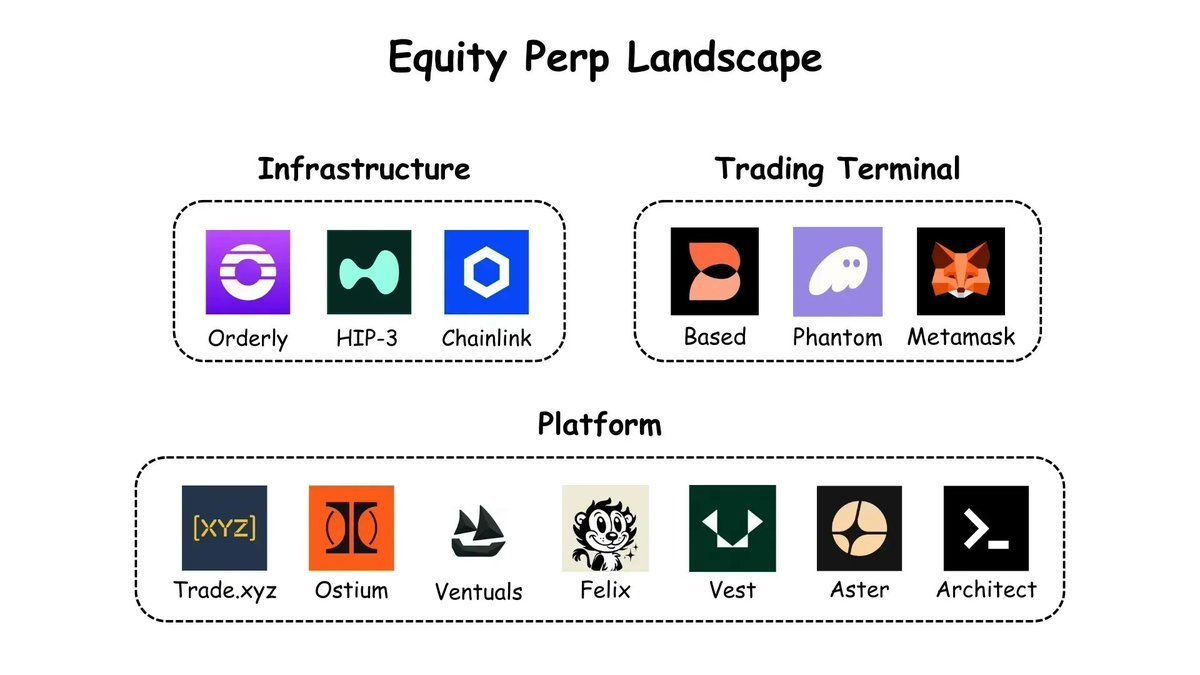

The entire tech stack is rapidly taking shape:

Infrastructure

-

HIP-3 / HyperCore: High-performance orderbook engine, supports any perp market

-

Orderly: Unified omnichain orderbook, anyone can launch a perp with no code

-

Chainlink: Stock price oracle (core data layer)

Platforms (Where trading happens)

-

Trade.xyz: Based on HIP-3, currently the largest equity perp DEX

-

Ostium: FX / Commodities / Stocks,偏向 (leaning towards) CFD structure

-

Ventuals: pre-IPO market (HIP-3)

-

Felix / Vest / Aster / Architect: Each has its focus on settlement, coverage, and distribution

Terminals (Current upstream traffic entry points)

-

Based: Multi-asset interface aggregating Hyperliquid, HIP-3, and prediction markets

-

Phantom / Metamask-like frontends: Convert wallet traffic into trading behavior

Looking forward, the focus is shifting from "tokenization" to "monetary velocity." The real on-chain GDP will be generated here. The ultimate winners won't just be players who can mint on-chain wrapped assets, but those trading venues that, at scale, can convert any asset into usable collateral and provide the deepest liquidity and the cleanest matching / risk engine.

Imagine the future as a globally unified "collateral network": Bitcoin, U.S. stocks, gold, U.S. Treasuries are no longer locked in their respective systems but can be used as collateral like building blocks at any time; perpetual contracts become the most universal risk expression tool; stablecoins play the role of cash; various trading and arbitrage strategies run automatically 7×24 on-chain, constantly combining. Assets are no longer "held" but are continuously called upon.

Racing Against Time

The window is open, but time is not on the side of on-chain equity perps. The biggest threat is not demand, but the formal approval of onshore products. History has repeatedly shown that once regulators nod, distribution回流 (flows back) to the existing brokerage system in an extremely short time. 0DTE options are the most direct example: after approval, they were quickly absorbed and dominated by Robinhood.

More importantly, the countdown has begun. The SEC and CFTC are systematically studying perpetual derivatives and their market structure and risks, which usually means regulatory boundaries are being actively defined. Meanwhile,

-

Bitnomial became the first CFTC-compliant perp

-

Coinbase also launched 5-year futures with a funding mechanism,几乎 (almost) indistinguishable in trading behavior from perps.

The reason offshore and on-chain players can still lead is simply that the products haven't been standardized yet. Once the rules take shape, the advantage will quickly disappear. Those who truly have a chance are not those waiting for certainty, but those who, while the window is still open, quickly lock in users and liquidity, and shape the rules while running and coordinating with regulators. Time is not a background variable but the core constraint determining victory or defeat, and the countdown has already begun.

Just as Tether used crypto's distribution power to quietly push the dollar globally back in the day, today's on-chain economy is essentially doing the same thing—leveraging the liquidity and trading tools of the crypto market to deliver U.S. stocks and American assets in a form with higher frequency, higher leverage, and higher liquidity to a broader set of participants. On-chain is not对抗 (fighting against) off-chain; it is rewriting the operating methods of the existing system with faster speed and stronger capital efficiency. The real watershed lies in whether one can timely capture this mechanism and complete the cognition and layout of the new continent on-chain.