Author: Liam 'Akiba' Wright

Compiled by: Deep Chao TechFlow

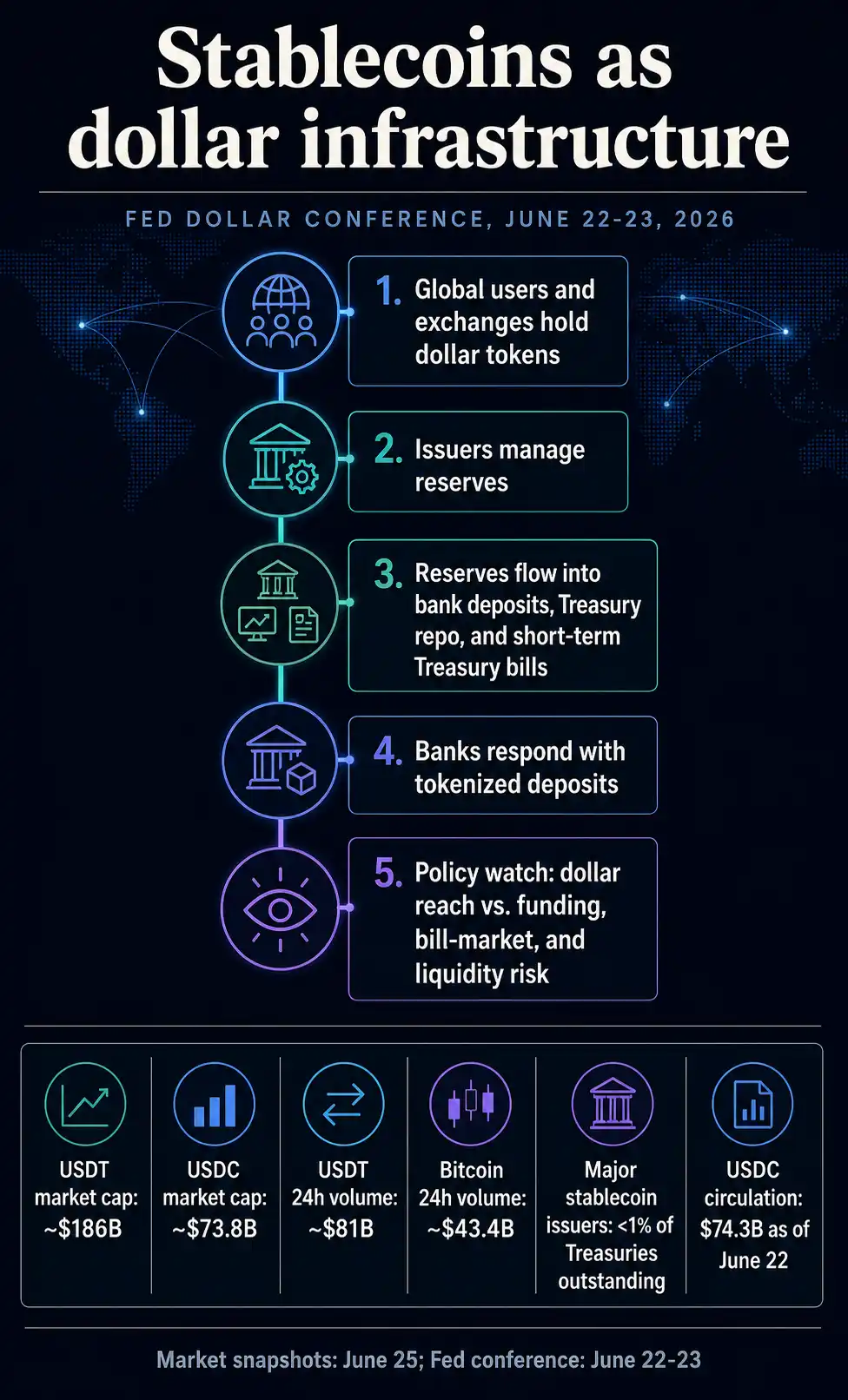

Deep Chao Insight: At the meeting on June 22, Federal Reserve Governor Waller upgraded stablecoins from a tool in the crypto market to an object of study for US dollar policy. This means that when the scale of USDT and USDC becomes large enough to influence the demand for short-term government bonds, bank financing, and global US dollar liquidity, they are no longer merely private tokens but channels for dollar transmission that the Federal Reserve must incorporate into its monitoring.

Federal Reserve Governor Christopher Waller included stablecoins in the Fed's research agenda regarding the international role of the US dollar at the central bank's dollar conference on June 22.

This is significant because dollar-denominated tokens impact bank financing, demand for short-term Treasury securities, and how global users access US dollar liquidity.

Now the question is whether growth stems from overseas demand or substitution for bank deposits, and whether reserve and redemption mechanisms can withstand stress tests.

Stablecoins have moved from the fringes of crypto policy discussions to the US dollar policy agenda of the Fed led by Kevin Walsh.

Federal Reserve Governor Christopher Waller used the central bank's dollar conference on June 22 to incorporate digital assets, including stablecoins, into the research agenda concerning the international role of the US dollar.

This statement is a signal for research rather than a new stablecoin policy. But it changes the context: stablecoin flows are now placed alongside issues like US dollar financing, payment channels, cross-border capital flows, demand for safe assets, and how private token issuers access public US dollar infrastructure.

Fed Governor Waller says "There's nothing scary about payments on DeFi channels"

This redefines the market. Dollar-backed stablecoins remain crypto trading tools, payment tokens, and regulatory subjects. But the Fed's US dollar agenda now views them as a potential transmission channel.

Waller's speech and the Fed conference agenda place stablecoins within a larger system: private digital dollar claims can flow among exchanges, wallets, issuers, banks, and reserve investment portfolios, while still relying on the US dollar and the short-term assets backing it.

A reasonable question is: what changes if these issuers become one of the channels through which global dollar demand reaches the banking system and Treasury market.

The Fed Treats Stablecoins as a US Dollar Channel

In his opening remarks at the Fifth Conference on the International Role of the US Dollar, Waller described distributed ledger technology and tokenized assets (including stablecoins) as channels for global US dollar intermediation, operating in parallel or connecting with traditional banking and payment systems.

The conference agenda clarifies the policy framework. The Federal Reserve and the New York Fed organized this June 22-23 event around financial innovation, digital assets, the role of the dollar in investment and payments, market structure, reserve currency status, digital fragmentation, and geopolitics.

Stablecoins are located on this broader digital dollar research map, alongside other digital assets and market structure issues.

The role of the dollar is typically discussed from the perspectives of banks, Treasury markets, foreign exchange reserves, trade invoicing, and offshore financing. Stablecoins add a private technological layer to this map.

Users outside the US can hold dollar-denominated tokens, transfer them between blockchains, trade them for other assets, or redeem them through issuers, while interacting with the dollar system differently than bank depositors or money market fund investors.

The result is a more complex form of US dollar access. Stablecoins can expand the reach of the dollar by making dollar claims easier to hold and transfer.

Once reserve management, redemptions, liquidity shocks, or overseas demand become large enough to affect other markets, they also pull private issuers into the policy debate.

That's why scale changes the policy question. Stablecoins are still small compared to the entire Treasury market, but they are already large within the crypto space.

CryptoSlate market data shows that Tether and USDC ranked among the top five crypto assets by market cap on June 25, with USDT near $1.86 trillion and USDC near $738 billion.

Tether's 24-hour trading volume alone was approximately $81 billion, almost double Bitcoin's roughly $43 billion during the same period.

These figures are just a snapshot. More importantly, dollar tokens now have sufficient scale and turnover to prompt central bank researchers to ask where the underlying dollars come from, where reserves are held, what happens during redemptions, and whether these flows might create stress in areas previously studied mainly through banks and money funds.

Circle's own materials show that as of June 22, USDC's circulating supply was $74.3 billion, and it states that the token is backed by highly liquid cash and cash equivalents. Circle also states that most reserves are held in the Circle Reserve Fund, an SEC-registered government money market fund managed by BlackRock.

This structure turns a payment token into a reserve management channel. Changes in stablecoin demand can alter demand for bank deposits, Treasury repo, or short-term Treasuries, depending on how issuers manage the backing assets.

Therefore, the US dollar policy narrative goes beyond one-to-one redemptions. The policy question is whether a sufficient volume of private tokens, backed by enough short-term US dollar assets, can be integrated into the distribution and absorption of US dollar liquidity.

Stablecoins Compete for Both Payments and Balances

Fed staff research has begun to distinguish potential bank impacts from the simplistic narrative of stablecoins draining deposits. A May FEDS note stated that stablecoins are noteworthy because they combine balance holding and payment functions on digital channels, meaning they compete for both transaction balances and payment flows simultaneously.

Another Fed note in December described deposit impacts as conditional. Stablecoin growth could reduce, recycle, or restructure bank deposits depending on who needs the tokens, what assets they convert from, and how issuers hold reserves.

Domestic users moving transaction balances out of banks have one effect. Overseas users seeking digital dollars might have another.

Issuers placing reserves in banks, money funds, repo, or bills transmit growth through different parts of the financial system.

Banks are now part of the response. On June 5, The Clearing House announced that major financial institutions support the Regulated Liability Network initiative to support clearing and settlement of tokenized bank deposits, while connecting blockchain activity to RTP and CHIPS.

Major Banks May Have Found an Answer to the Stablecoin Challenge in the CLARITY Act

This announcement shows the direction of the banking response: keeping digital currency flows within regulated commercial bank money while stablecoins build round-the-clock dollar channels.

A 2026 New York Fed staff research paper argues that stablecoin activity can transmit liquidity pressure to banks and complicate monetary policy implementation.

This is not an official policy statement, but it points to the same issue raised by Waller's conference framework: once stablecoins interact with banks, reserves, and wholesale payments, their effects spill over beyond the crypto market.

The strongest macro link is demand for short-term safe assets. A June BIS working paper found that inflows into dollar-backed stablecoins can lower short-term Treasury yields, an effect that intensifies during Treasury market stress and as the sector grows.

The paper's findings are quite specific: it describes yield compression from inflows into short maturities, not claiming to affect the entire Treasury curve.

Treasury advisory material adds a scale check. The 2026 Treasury Borrowing Advisory Committee report found that major stablecoin issuers held less than 1% of outstanding Treasury securities.

Tether's $141 Billion Treasury Reserve Reveals the Stablecoin Risk Now Embedded in US Debt

The same report also said stablecoins could add to demand for short-term Treasury issuance if future growth comes from new overseas dollar demand. This combination is the tension policymakers must track.

Today, stablecoins can be small relative to the entire Treasury market but still affect bills and repo at the margin.

At larger scale, their reserve portfolios could become another source of demand for the safest, most liquid dollar assets. During stress, redemptions could work in the opposite direction.

The dollar-strengthening argument relies on this channel. If dollar stablecoins continue to spread overseas, they can expand access to dollar instruments without foreign users needing US bank accounts.

But it also means private issuers and reserve managers become part of the system for distributing dollar liquidity. The more successful the model, the harder it becomes to view it as a crypto fringe market.

The Next Signal Is How the System Absorbs Them

The Fed's June meeting left an open question: will stablecoins continue as tolerated private extensions of dollar dominance, or become a more explicitly regulated layer of US dollar infrastructure. It indicates this issue has entered the main research agenda for the dollar.

Near-term signals suggest policymakers will observe whether stablecoin growth is driven by overseas dollar demand or domestic bank deposit substitution.

Banks will test whether tokenized deposits can match stablecoins' speed and programmability while keeping balances within the banking system. Issuers will have to prove that reserves, redemptions, and concentration risks can handle rapid expansions or contractions in stablecoin supply.

This is what changes when the Fed treats stablecoins as part of global dollar transmission. Tokens that once looked like crypto settlement assets become private dollar channels with public consequences.

Their growth can support dollar reach but can also, within the same framework, raise questions about bank funding, short-term Treasury demand, and liquidity stress.

The threshold is lower than replacing banks or dominating the Treasury market. Once stablecoins are large enough, useful enough, and connected enough that dollar demand increasingly flows through them, they become a policy question.