Author:Jonah

Compiled by: Jiahuan, ChainCatcher

I've been holding onto this article for a while.

I've wanted to write it, but kept holding back, hoping things would quietly correct themselves. Until this morning when Bloomberg published "Polymarket Loses Prediction Market Lead to Delays and Backlash". To be honest, that report already says most of what I originally wanted to say. So I'll quote heavily from it, letting it shoulder some of the weight.

Polymarket, facing increasing operational setbacks in its attempt to reach its key audience (US customers), has now fallen behind its main competitor. From bloomberg.com

That headline is painful. And it should be.

I've been watching Polymarket since mid-2024. I believed in its vision, defended the platform in every regulatory scare, and recommended it to every trader I know. Prediction markets are some of the most important financial infrastructure of this decade, and Polymarket was the company I always hoped would win this赛道.

So this is not a hit piece. This is the kind of letter you write to something you truly care about.

Shayne Coplan, and the entire team, we need to talk.

The Current Situation is Brutal

Let's start with the data.

Reportedly, Kalshi's valuation is around $22 billion, and Polymarket's negotiated valuation is around $15 billion. That's a gap of about $7 billion against an opponent that was once far behind Polymarket. Year-to-date trading volume: Kalshi ~$37 billion, Polymarket ~$29 billion. US market share: Kalshi nearly 90%, while Polymarket is still stuck behind a waitlist.

A year ago, the mainstream narrative was "Polymarket is the king of prediction markets, Kalshi is the regulated stepchild." Today, the narrative has completely flipped. Kalshi has become the compliant, fast-delivering, institutionally credible option, while Polymarket has become the crypto-native veteran that keeps tripping over itself.

This lead was once firmly in our hands. Now, we are giving it away.

The Platform Itself Isn't Fully Operational

This needs to be said straight: there are real problems with the core product, and the company is acting like it's fine.

Last weekend, Polymarket delayed the CLOB V2 migration, the new pUSD collateral token, and the rebuilt matching engine by at least a week. To be fair, the delay itself was the right decision. The developer community had been shouting for weeks that there simply wasn't enough time for a clean migration integration. Pushing a half-finished product live would have been much worse than a delay.

So the delay is not the problem; the delay is actually a good thing.

What was embarrassing was the way the announcement was handled.

From what circulated in the community: the news of the delay went out on Twitter first, but the official migration announcement containing the guide hadn't even been posted yet. The migration guide that followed shortly after still referenced the old, now obsolete dates. Then corrections were added on top of corrections.

Structurally, this is exactly the kind of communication chaos that a "methodical operating machine" should not produce.

Then on Monday, a scheduled five-minute restart took over an hour. The exchange was effectively offline during peak weekday hours. Another small thing added to the mountain of problems.

As the Bloomberg article quotes a Polymarket spokesperson: you can't "build one of the most interesting consumer finance products of the last few years without becoming a methodical operating machine." That's true, that's the vision. But the reality is that this machine keeps failing on avoidable small things, and these small things are accumulating into a pattern.

And these are not isolated incidents:

- Fee adjustments for sports and crypto markets seemed reactive and poorly communicated

- The team预告ed the migration for months, with repeated delays on the infrastructure

- Planned maintenance windows repeatedly far exceeded the stated duration

- The US app has been stalled for months in a "mobile-only, sports-only, invite-only" beta phase, reportedly with over a million people on the waitlist

"Crypto-native" was supposed to mean more transparent, more resilient, and more accountable than traditional platforms, not an excuse for poor UX and unreliable infrastructure.

The community has patience, but patience is clearly not infinite. Every outage, every missed deadline, every vague status update pushes marginal users towards the competitor that "just works".

The Priority Order is Wrong

What really broke me yesterday was this.

Objectively, the platform is not at 100%. The upgrade was delayed. The US app is not fully open. A million people are on the waitlist. Traders on the global product suffered an outage on Monday afternoon.

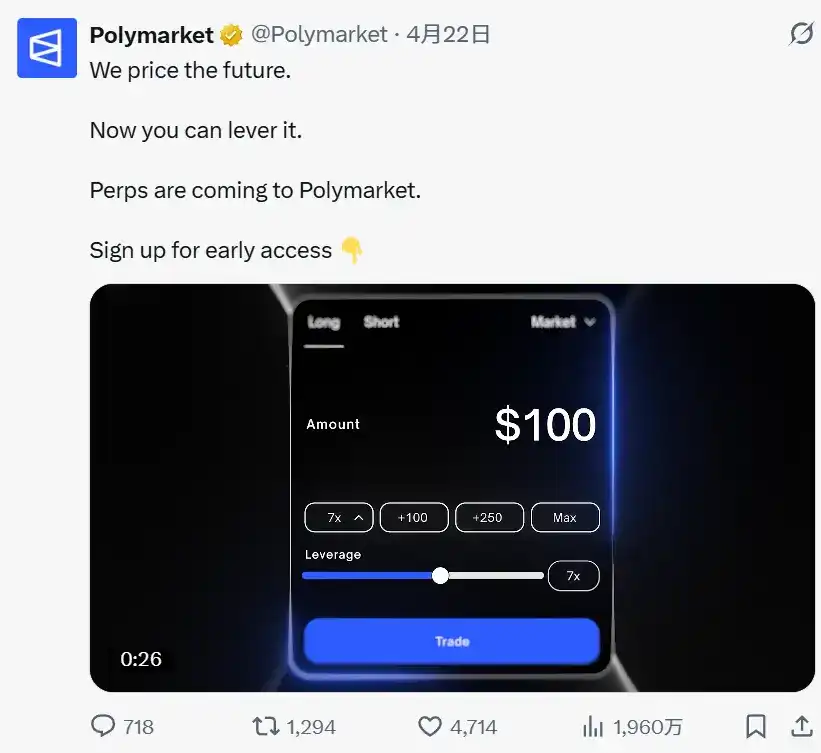

And then yesterday, Polymarket announced Perpetuals.

We price the future. Now you can leverage it. Perpetuals are coming to Polymarket. Sign up for early access.

Perpetuals are a great product, and in the long run, they absolutely belong on the roadmap. But announcing them now—just days after an infrastructure upgrade was delayed and a restart ran严重overtime, and while the US app is still in beta—sends only one message to most community members: a cash grab.

Perpetuals are the highest-fee, highest-leverage, highest-volume product in crypto, the fastest path to extracting revenue from existing users. Announcing them while the core exchange is unstable and a million Americans are locked out clearly signals where the team's true priorities lie: monetize the existing traders first, fix the platform later, and address the people outside the gate even later.

Whether intended or not, that is the signal this move sends. Revenue coverage优先于 product stability. Shipping new收费 products优先于 perfecting already-launched products. Harvesting existing users rather than fixing the experience for everyone—current and waiting.

Honestly, interpreting this as a "cash grab" might already be generous.

Look at the order. Kalshi预告ed its crypto perpetual product "Timeless": specific date, specific venue, specific launch event—April 27th, New York, a full product, delivered a week later.

Breaking: US's first CFTC-regulated prediction market exchange @Kalshi has chosen Pyth Pro as the exclusive data layer for its commodity markets. Gold, silver, oil, natural gas, copper, corn, soybeans, wheat. Here's why it matters.

Within days, Polymarket's response was... an early access sign-up page. No release date, no venue, no product specs, no product itself. Just a marketing tweet, a slogan "We price the future. Now you can leverage it," and a form to collect accounts.

That wasn't a product launch; it was a press release disguised as a launch announcement. When what you put out to counter an opponent is明显空洞, you are no longer setting the pace in this赛道—you are chasing someone else's pace. And there's a waitlist for it?

This is a赛道 defined by Polymarket itself. Polymarket was the pioneer, the cultural phenomenon, the incumbent with a head start of years. And today, on the derivatives launch, Polymarket became the chaser, using a sign-up form as PR material, simply because Kalshi announced first.

This is the most embarrassing sentence in this entire letter, but it's exactly what the Bloomberg article is really about.

The operational order should be very simple:

- The US App. Fully open it, kill the waitlist, make it stable, make it feature-complete. This is Polymarket's biggest lever, yet it's been sealed for months, letting Kalshi eat the US retail market. This must be priority number one. Not second, first.

- Core Platform Reliability. Finish the CLOB V2 migration, execute the pUSD transition cleanly, stop missing maintenance windows, make the exchange something traders can "set and forget".

- Then, and only then, expand the business surface. Perpetuals, new market categories, other things on the whiteboard.

The current order is backwards, and the community sees it clearly.

The Startup Phase is Over

The Bloomberg article put into the open what the community has been discussing for months: delays, distractions, and a culture that still feels like a 2021 wild-west startup—despite Polymarket now sitting on billions in open interest, a major partnership with ICE, a CFTC designated exchange status via the QCEX acquisition, and an MLB partnership.

That wild-west startup era is over. It has to be.

You are no longer facing a forum or a niche crypto app. You are facing a CFTC-licensed, institutionally-backed, New York-bred opponent that delivers on time and is taken seriously by regulators, counterparties, and the media.

This is the maturation period that every phenomenal finance company must eventually go through. Coinbase went through it, Stripe went through it. Every serious trading venue must eventually stop operating like a "group chat" and start becoming—to borrow the spokesperson's own words—a methodical operating machine.

Concretely, this means bringing in truly seasoned professionals in operations, risk, and PR. It means cutting out distractions that don't serve US rollout and core stability. It means over-communicating when things go wrong, with real post-mortems and real accountability, not just brief status updates and subsequent silence.

This is not hostility. This is what every serious financial venue eventually does. Polymarket is now one of them. Act like it.

Why I'm Still Bullish on Polymarket

With all that said, here's why I haven't left the platform, and why I don't think this race is over.

ICE is on your side. Jeffrey Sprecher doesn't write checks for vaporware. Intercontinental Exchange, the parent company of the NYSE, led a round last fall, a signal the market still hasn't fully priced in. You now have direct access to one of the world's most sophisticated market infrastructure operators. Use it.

The MLB partnership is a ceiling-level bonus. This signal says the endgame here is not "another betting app," but making prediction markets mainstream, embedded institutional financial infrastructure. Sports leagues, TV networks, traditional finance rails all converging on a single order book is epoch-making. Kalshi clearly doesn't have this cultural reach.

The brand is iconic. For better or worse, in public perception, Polymarket is almost synonymous with prediction markets. The election cycle cemented this彻底, with the platform being cited by journalists, hedge funds, and memes repeatedly. This is a moat most companies can only dream of.

The community is still here. The people who showed up in the early markets, scaled it during the 2024 election, and stuck with the platform through all the growing pains, haven't left. We want to win, and we want to see you win. That's why we're writing letters like this now,而不是 silently migrating volume to another platform.

Bring the Win Home

Truth: Kalshi is winning this quarter, and possibly this entire year.

But Polymarket can still win the decade. The brand, the partnerships, the community, the regulatory angle via QCEX, the ICE relationship—it's all still there, nothing is lost. It's just not being fully utilized while the team is pushing the wrong things in the wrong order.

So the ask is simple.

Fix the platform. Push out the US app. Stop announcing new products until the old ones are stable. Truly become the methodical operating machine the spokesperson described.

The community is still with you, and the believers are still here. But the window to close the gap is narrower than it was six months ago, and it will be even narrower in another six months.

Fix the platform first. Then, bring the win home.

Penned by a longtime Polymarket user who wants, more than anyone, to never have to write a letter like this again.