Author: Xiao Bing, Tide Research

On June 4th, SpaceX officially launched its IPO roadshow. The 62-page presentation details an offering of 555.6 million shares at $135 per share, aiming to raise $75 billion and target a valuation of $1.75 trillion. If all proceeds as planned, pricing will occur on June 11th, with trading commencing on Nasdaq under the ticker SPCX on June 12th.

This will be the largest IPO in the history of human capital markets, surpassing Saudi Aramco, Alibaba, and all others.

Five major investment banks—Goldman Sachs, Morgan Stanley, Bank of America, Citi, and JPMorgan—are joint lead underwriters, with 21 institutions participating in distribution. Elon Musk has a lock-up period of 366 days. Insider unlocks for other internal stakeholders will begin in batches starting after the Q2 2026 earnings report. Fidelity is opening subscription to all retail accounts holding over $2,000.

The internal codename for the roadshow presentation is Project Apex, and based on its content, the name is fitting.

Three Pillars: Space, Connectivity, AI

In its roadshow, SpaceX defines itself as "the only company simultaneously building infrastructure for space, connectivity, and AI." This is not mere marketing rhetoric. From a financial perspective, the three business segments exhibit vastly different growth trajectories, profitability characteristics, and capital requirements, constituting an extraordinarily complex investment proposition.

Space: The Foundation

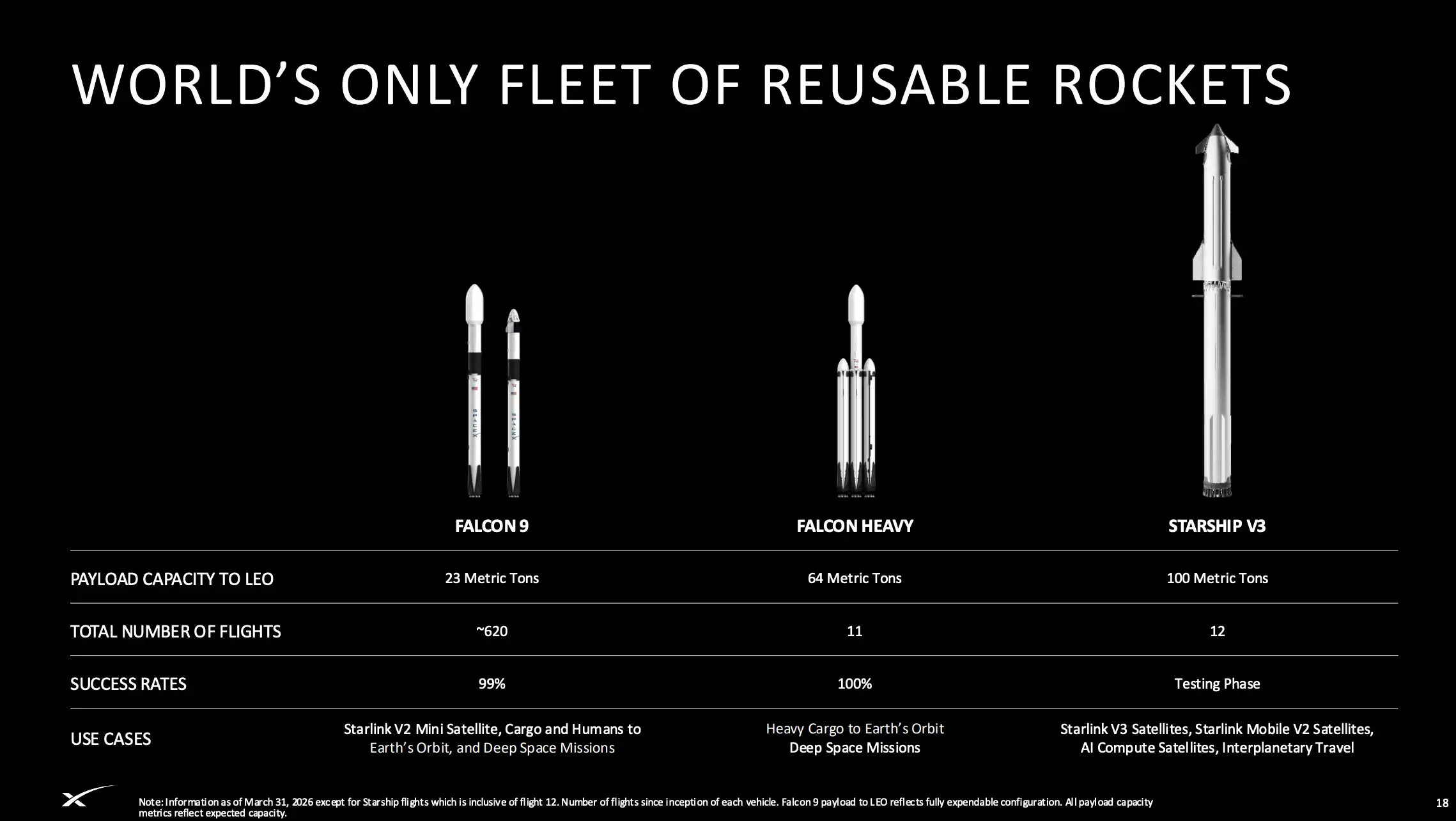

In 2025, SpaceX completed 165 Falcon series launches, using only 8 newly manufactured boosters. Rocket reusability technology has transitioned from experimental to industrialized production, directly driving launch costs down from the historical industry average of $18,500/kg to $2,700/kg for Falcon 9 and $1,400/kg for Falcon Heavy. The goal for Starship V3 is to reduce costs by over 99% from these levels.

Over 80% of the world's orbital mass is delivered by SpaceX. This figure was 65% in 2023 and 45% in 2021. Such market concentration is extremely rare in any infrastructure industry.

However, the financial performance of the space segment itself is not stellar. In 2025, revenue was $4.1 billion (excluding internal satellite launches for Starlink), representing only 8% year-over-year growth. More critically, Starship R&D investment reached $3 billion in 2025, dragging the space segment's operating profit into a loss of $657 million. Adjusted EBITDA declined from $1.2 billion in 2024 to $700 million in 2025.

The value of the space business lies not in its own profitability but in the deployment capability it provides to the other two segments at a cost far lower than competitors. Every Starlink satellite launch, every future deployment of orbital AI satellites, is built upon the cost curve of Falcon and Starship.

Starlink: The Cash Machine

Starlink is the true valuation anchor for SpaceX.

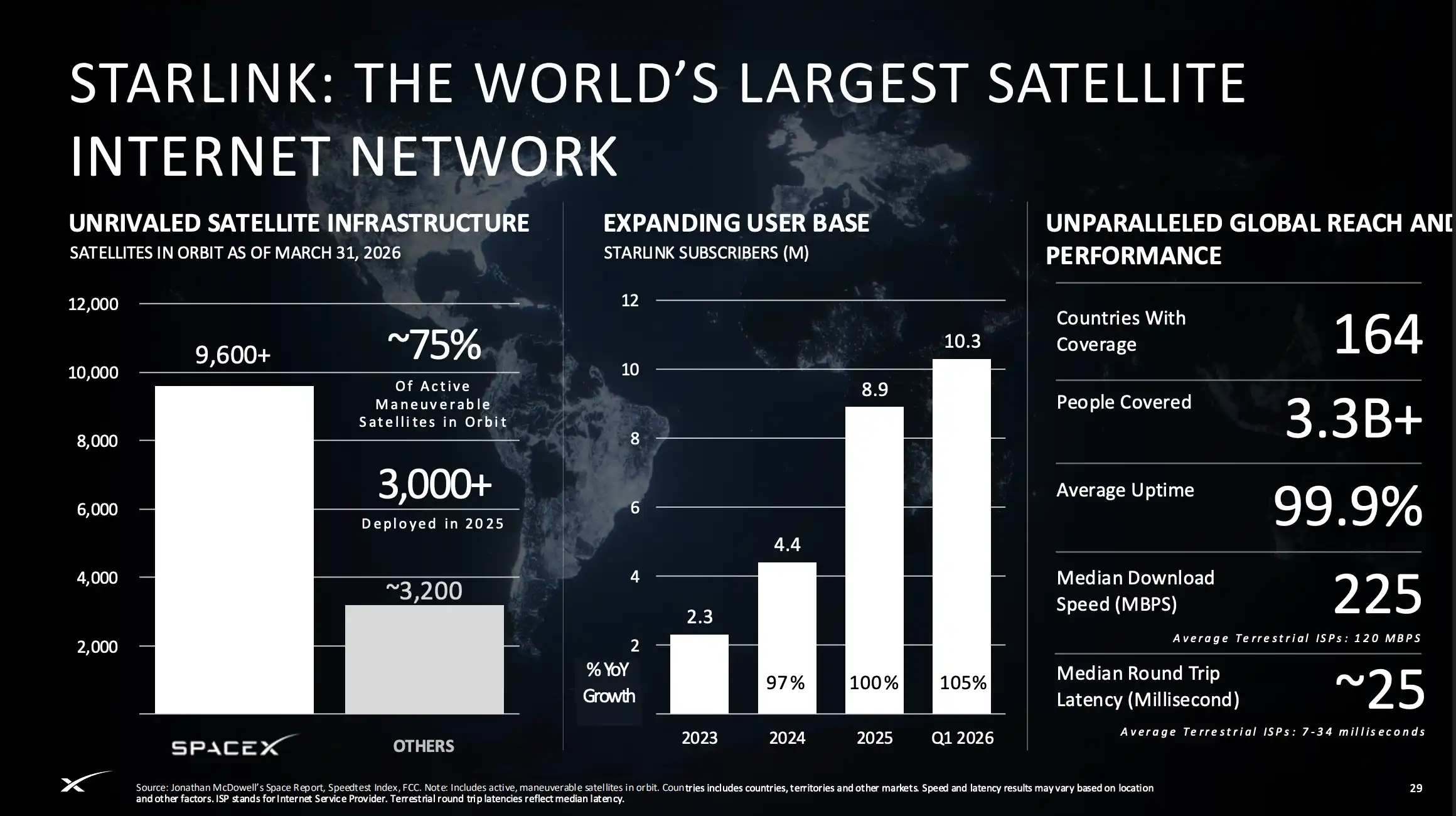

Subscribers grew from 2.3 million in 2023 to 4.4 million in 2024, 8.9 million in 2025, and reached 10.3 million in Q1 2026. Coverage spans 164 countries and regions, with a median download speed of 225 Mbps, median latency around 25ms, and average uptime of 99.9%. Among all maneuverable satellites globally, Starlink accounts for roughly 75%.

The financial data is more direct: Starlink generated $11.4 billion in revenue in 2025, up 50% year-over-year. Adjusted EBITDA reached $7.2 billion, with operating profit at $4.4 billion. This is SpaceX's only consistently profitable segment, and its margins are still expanding.

The roadshow presentation reveals a key technical upgrade: the V3 satellite. Each V3 satellite boasts a bandwidth of 1024 Gbps, more than 10 times that of the current V2 satellite. Launching V3 satellites on Starship (60 per launch) can add 61,000 Gbps of network capacity per launch, which is over 20 times the capacity added by current Falcon 9 launches with V2 satellites.

Deployment of V3 satellites on Starship is planned to begin in the second half of 2026. If Starship achieves operational-level reusability on schedule, Starlink's bandwidth expansion speed will see an order-of-magnitude leap, further widening the gap with all competitors.

Starlink Mobile (direct-to-cell satellite connectivity) is also noteworthy. Approximately 650 first-generation mobile satellites have been deployed, covering about 1.9 billion people. Partnerships have been established with around 30 mobile operators, including a 2025 agreement with a major U.S. airline for in-flight connectivity. Second-generation mobile satellites, planned for deployment on Starship in 2027, will offer 5G-level speeds and voice services. SpaceX also signed an agreement in 2025 to acquire EchoStar's U.S. and global mobile satellite spectrum licenses for $65 per MHz-POP, expected to close in November 2027.

The TAM (Total Addressable Market) presented for the connectivity business is $1.6 trillion (Broadband $870B + Mobile $740B). Based on the current growth trajectory, the penetration rate into this TAM remains low.

AI: A Money-Burning Black Hole or a Trillion-Dollar Bet?

In February 2026, SpaceX completed the acquisition of xAI in an all-stock transaction, with a post-merger valuation of $1.25 trillion. This deal is a key variable in understanding SpaceX's $1.75 trillion IPO valuation and the largest source of controversy.

The post-merger AI business comprises three components:

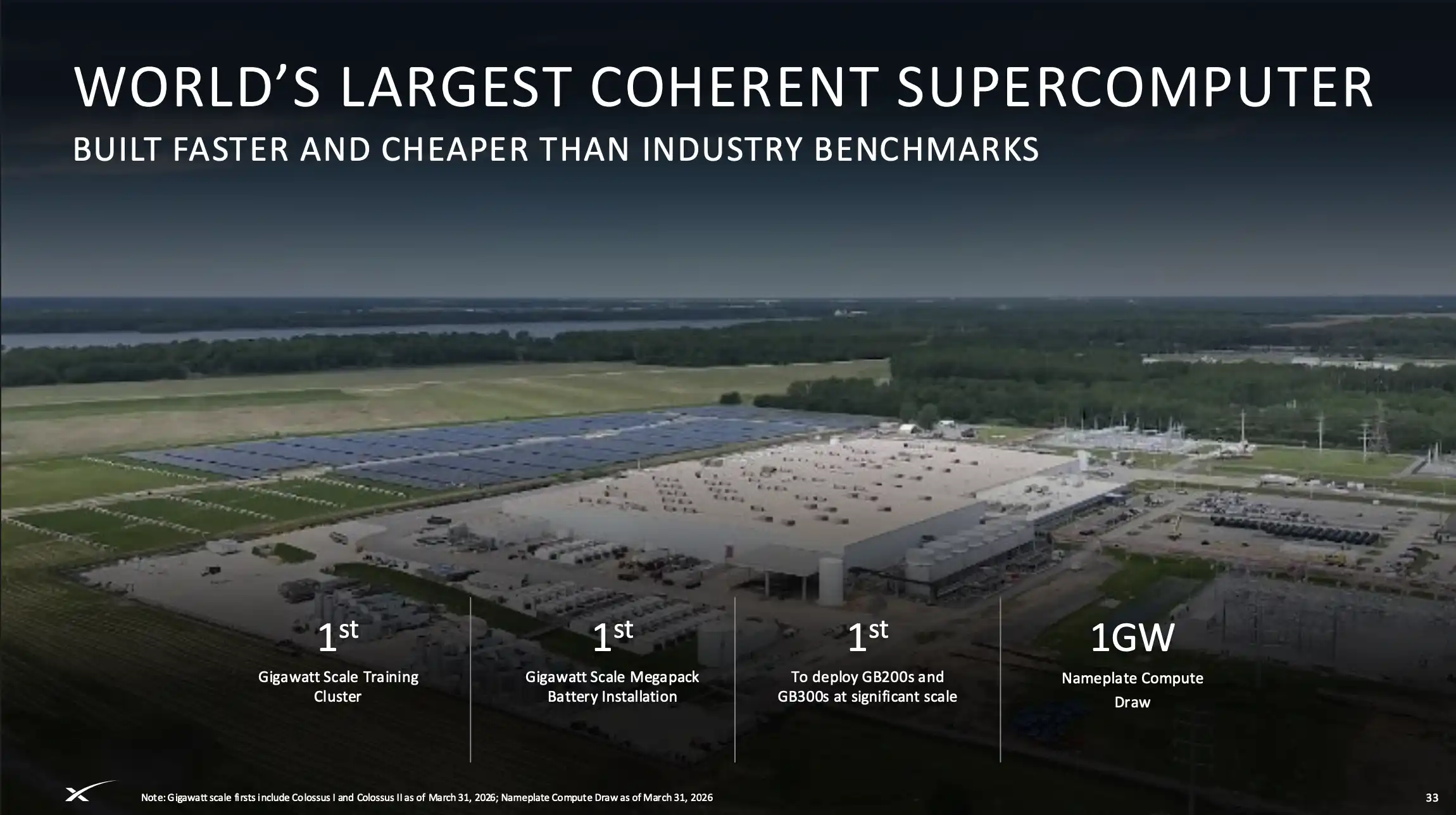

First, compute infrastructure. The combined compute power of Colossus I and Colossus II reaches 1 GW, claimed to be the world's largest coherent supercomputer and the first GW-scale cluster deploying GB200 and GB300, paired with a GW-scale Tesla Megapack battery storage system.

Second, the Grok large language model. The roadshow claims it achieves frontier performance on benchmarks like scientific reasoning (GPQA Diamond), stating it is "faster than any other leading model provider." The current version, Grok 4.3, was released in May 2026. SpaceX also has an agreement with Cursor, granting it an option to acquire Cursor at an implied valuation of $60 billion.

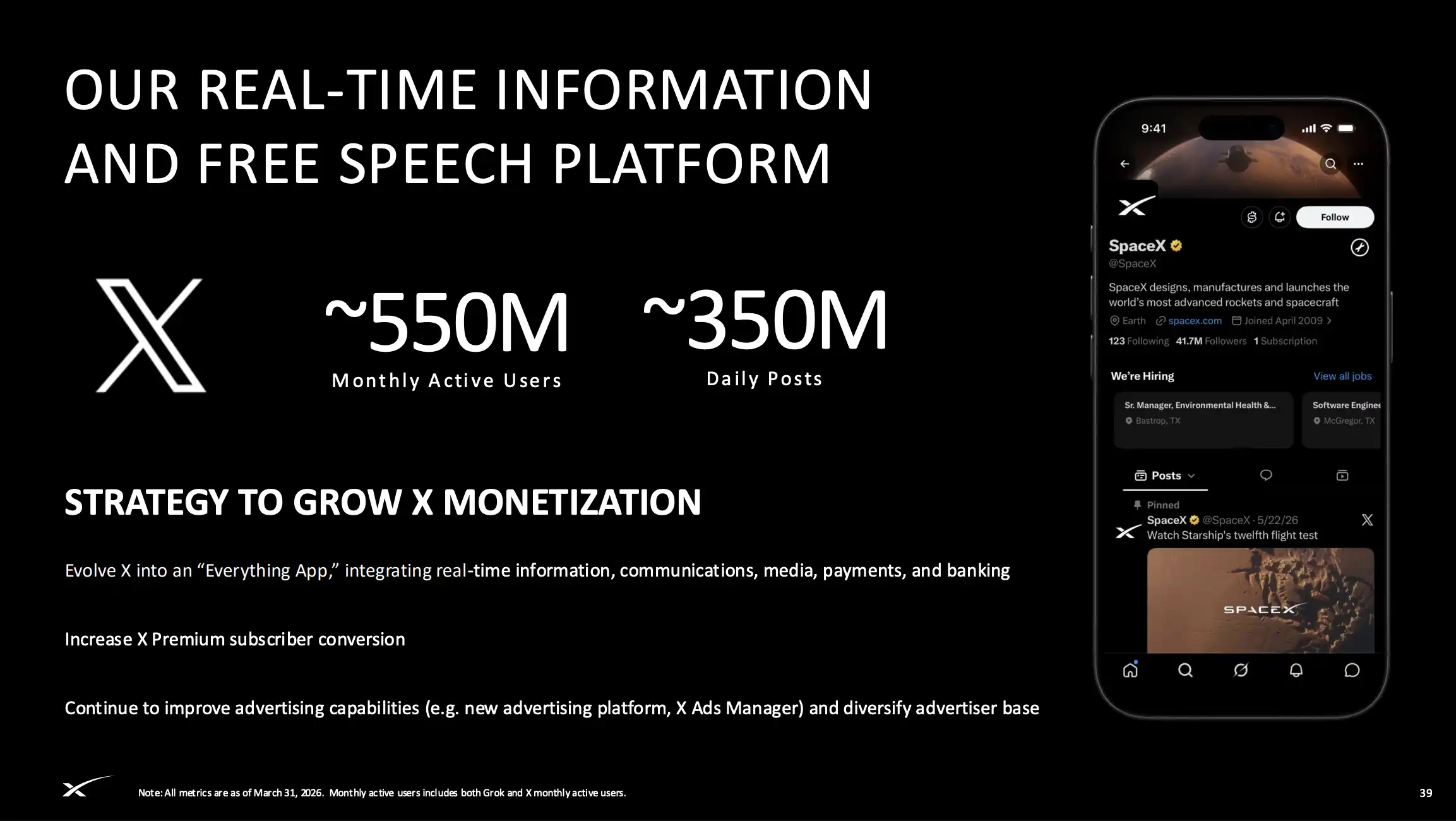

Third, the X platform. Approximately 550 million monthly active users (including Grok and X users), with about 350 million daily posts. 117 million MAUs have used Grok's AI features. X is launching a new advertising platform, X Ads Manager, and plans to evolve into an "Everything App" integrating messaging, communication, media, payments, and banking.

Monetization for the AI business currently follows three paths: consumer (X Premium subscription + advertising), enterprise (Grok Enterprise/API + Cursor partnership), and compute power sales (a computing capacity agreement with a cloud service provider for a monthly fee of $1.25 billion, running through May 2029).

However, the financial reality is stark. The AI segment generated $3.2 billion in revenue in 2025, with the vast majority coming from X's advertising and subscription income. Adjusted EBITDA was negative $1.2 billion, with an operating loss of $6.4 billion, consuming 61% of the company's total capital expenditures. Morningstar estimates xAI will burn through $10 billion in 2026.

The near-term TAM presented for the AI business is $3.8 trillion (Infrastructure $760B + Consumer Subscriptions $600B + Digital Advertising $2.4T). Adding "larger opportunities unlocked by AI," the total TAM soars to $26.5 trillion.

The Most Valuable Page: Sending GPUs to Space

Pages 35-36 of the roadshow presentation contain the highest information density in the entire document and represent SpaceX's most significant differentiating play in its investment narrative.

The core logic is that U.S. ground-level power supply cannot keep pace with the growth in AI compute demand. In 2025, data center power demand was 62 GW against a supply of only 49 GW, a 13 GW gap. U.S. electricity production saw almost zero growth from 2008 to 2023, compared to roughly 6% growth in China over the same period. Building data centers on the ground faces bottlenecks like grid approval, land planning, and community opposition.

SpaceX's solution: Move AI compute to space.

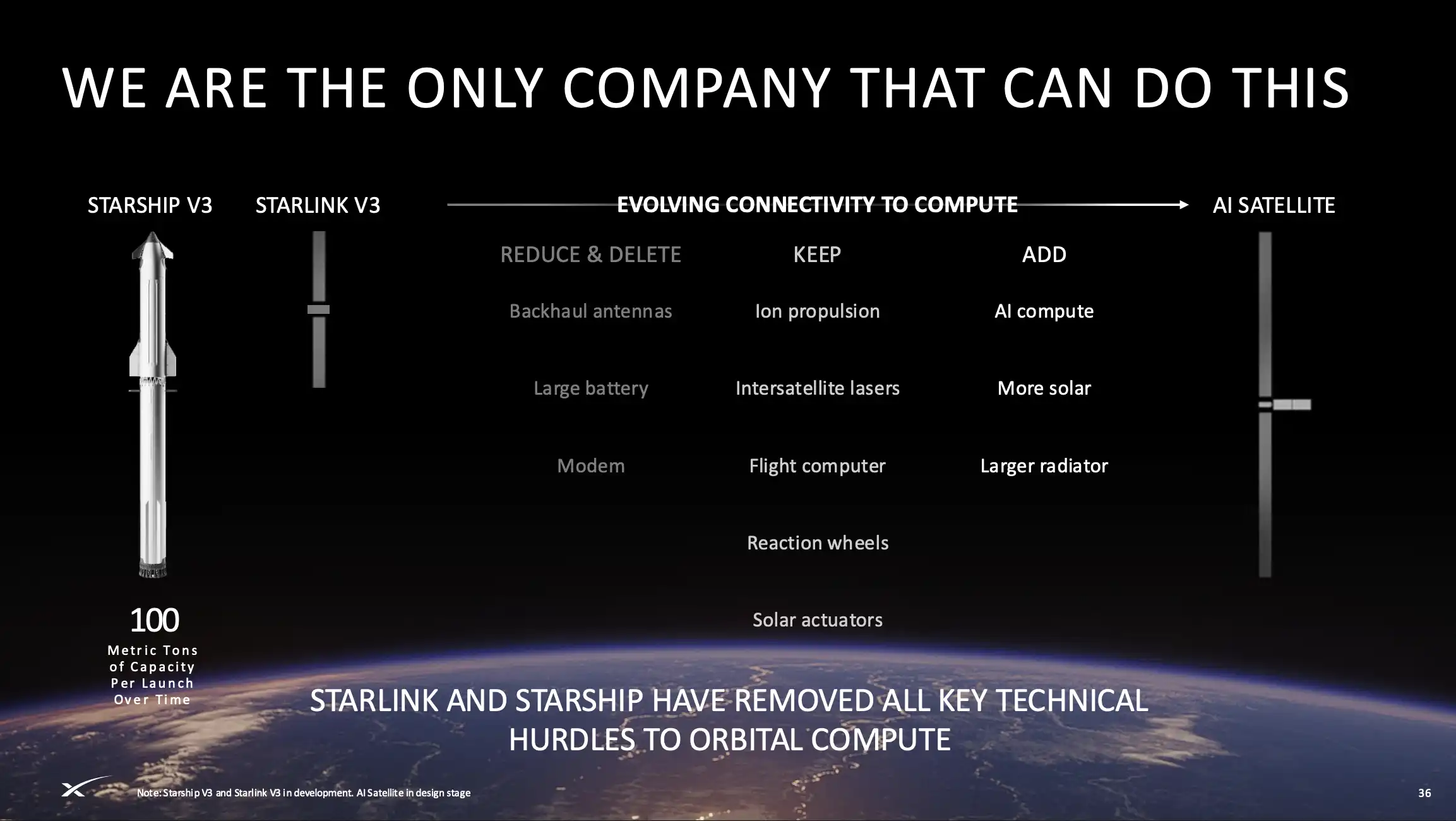

The design logic for orbital AI compute satellites builds upon the Starlink V3 satellite platform. The roadshow outlines a clear evolutionary path: The Starlink V3 retains core components like inter-satellite laser links, flight computers, and attitude control, removes downlink antennas, large batteries, and modems, and adds AI compute chips, more solar panels, and larger radiators.

SpaceX claims orbital AI compute has three structural advantages:

First, solar power is limitless, clean, and potentially lower-cost, with distribution via the Starlink network, bypassing ground grid approval bottlenecks. In a sun-synchronous orbit, satellites are in sunlight over 99% of the time, supporting uninterrupted AI training tasks.

Second, using radiation for heat dissipation is potentially cheaper than liquid or air-cooling systems. Data is efficiently routed between orbital compute clusters and ground users via the existing Starlink network.

Third, faster deployment of new-generation chips. Each new generation of GPUs brings a step-change in token efficiency. Leveraging Starship's rapid payload launch cycles, upgrades can occur faster than in ground-based data centers.

SpaceX's calculation: Launching 1 million metric tons of satellites annually, with each ton providing 100 kW of compute power, would add 100 GW of AI compute capacity per year, with minimal ongoing operational costs.

On January 30, 2026, SpaceX submitted an application to the FCC to deploy up to 1 million orbital data center satellites—the largest data center construction proposal in human history. The FCC accepted it for review on February 2nd. Pilot testing of in-orbit compute nodes on Starlink V3 hardware will begin in the second half of 2026, with formal deployment of AI compute satellites starting in 2028.

The power of this narrative lies in its redefinition of SpaceX from a "rocket company + satellite internet company" to a "global AI infrastructure supplier."

A phrase repeated throughout the roadshow is: "Only we can do this."

This confidence stems from a vertically integrated chain that other companies cannot replicate: proprietary rockets (lower launch cost) → proprietary satellites (lower manufacturing cost) → proprietary inter-satellite communication network (lower data transmission cost) → proprietary AI model (directly consumes compute) → proprietary end-user platform (X, 550M MAU). From silicon to space, from space to end-user, the entire chain is owned.

Google is attempting something similar. Its Project Suncatcher, announced in November 2025, plans to launch two prototype satellites in early 2027 in partnership with Planet to validate the feasibility of AI payloads in orbit. However, Google would need SpaceX for launch and lacks the capability to build its own satellite network.

Nevertheless, the market remains sober about this narrative.

Analysis by Varda Space Industries indicates the per-watt cost of orbital compute is currently about 3x that of ground-based compute. While Musk claims cost parity could be achieved within 2-3 years, independent analysts generally believe it's only possible in the 2030s. Unsolved engineering challenges include cosmic radiation interference with chip operations, thermal management in a vacuum, and latency between orbital satellites and the ground. The head of Amazon AWS publicly stated that orbital data centers are "far from practical."

But even discounting this story by half, SpaceX's structural advantage remains: If any company wants to do orbital computing, they will ultimately need to buy SpaceX's launch services. Whether the timeline for orbital data centers is 2028 or 2035, SpaceX is the necessary path.

The Vision: Developing the Moon and Mars

Pages 43 and 44 of the roadshow contain no revenue forecasts or timelines. They simply list six phrases, each followed by a scenario that sounds like science fiction: Lunar Economy, Mars Energy Production & Manufacturing, Point-to-Point Earth Travel, In-Orbit Manufacturing, Manned & Cargo Mars Missions, Asteroid Mining...

The title of these pages reads: "We are best positioned to create trillion-dollar new markets."

On the Lunar Economy page, SpaceX provides slightly more detail, outlining three concurrent tracks:

First, support NASA's Artemis program to return humans to the Moon in the late 2020s, using Starship for crew transport to establish a sustainable lunar base and validate all systems needed for long-term human survival off-Earth. Second, build AI satellite factories on the Moon, using solar power and lunar mass drivers to launch satellites into orbit. Third, through this manufacturing-launch pipeline, scale global AI compute from GW to TW levels.

Of these three tracks, only the first has external backing. NASA's Artemis contract is a real commercial order; SpaceX is the sole selected contractor for the Human Landing System. Sending humans to the Moon in the late 2020s is plausible given current technological progress.

The second and third tracks currently remain at the conceptual engineering stage. The list of challenges for a lunar factory is long: lunar dust erosion of manufacturing equipment, precision assembly in low gravity, engineering validation of mass drivers—each could consume decades.

As for point-to-point Earth travel (using Starship for 30-minute intercontinental flights like New York to Shanghai) and asteroid mining, SpaceX itself provides no timelines.

But the presence of these two pages answers a question investors must confront: What exactly are you buying for a $1.75T valuation?

Morningstar's DCF model values SpaceX at $780B, anchored to Starlink's predictable cash flows and the stable income from space launch services. The nearly $1 trillion gap between $780B and $1.75T corresponds to a proposition far greater than five years of profit growth: If human civilization is to expand beyond Earth, SpaceX is the sole infrastructure provider.

This proposition doesn't require investors to believe the lunar factory will definitely be built or that Mars colonization will happen in their lifetimes. It only requires belief in one thing: If any of these scenarios moves toward reality, only SpaceX can do it.

Exclusivity, not certainty, is the pricing logic for this $1 trillion premium.

Tide Research Interpretation

In Tide Research's view, like Tesla, SpaceX is a "faith stock."

As Morningstar analyzed, Starlink alone could support a valuation north of $600B. But the ~$1 trillion between $780B and $1.75T is the "faith premium," pricing in the ten-year call options on orbital AI compute, lunar economy, and Mars colonization. A 94x revenue multiple is unprecedented for a trillion-dollar company.

Furthermore, xAI represents the largest risk variable in this IPO, a topic insufficiently addressed in the roadshow.

In the $250 billion all-stock acquisition in February 2026, Musk controlled both buyer and seller. This related-party transaction saddled SpaceX overnight with all the losses of the AI segment. Pre-merger, SpaceX was briefly profitable in 2024 ($800M). Post-merger, it reported a net loss of $4.9 billion in 2025 and a $4.3 billion loss in Q1 2026 alone. The AI segment's annual operating loss of $6.4 billion, projected to burn $10 billion in 2026, exceeds Starlink's $4.4 billion operating profit by 30%.

Grok's position in the frontier model race is far from secure, and X's advertising recovery is in its early stages. More notably, Musk maintains absolute control through a dual-class voting share structure, leaving public shareholders with little ability to check future related-party transactions or capital allocation decisions. Morningstar bluntly states xAI poses a "material risk of value destruction."

Finally, SpaceX's short-term trading logic and long-term investment logic may be entirely contradictory.

An extremely low float (3%), expectations of rapid inclusion in the Nasdaq 100 (potentially as early as July), price support from 21 underwriting banks, and market enthusiasm for AI infrastructure could create a supply-demand imbalance post-listing, pushing the stock price well above levels justified by fundamentals.

However, SpaceX's lock-up structure is unique: Insiders can start selling 20% in batches after the Q2 2026 earnings report, with the first major unlock wave coming in December 2026. Musk's personal lock-up expires after 366 days (June 2027). Combined with the gradual exposure of AI segment losses in quarterly reports, a significant window of selling pressure could form from late 2026 into the first half of 2027.

Overall, the 62-page roadshow paints a picture of a full-stack infrastructure empire spanning from Earth to space, from rockets to AI. SpaceX's launch capabilities and Starlink's growth curve have proven the Musk team's execution prowess. The question is: Where are the limits of that execution? Within the atmosphere, or beyond?

The answer to that question will determine whether $1.75T is visionary or hubris.

Disclaimer: This article represents solely the analytical views of Tide Research and does not constitute any investment advice. SpaceX has not officially listed. The financial data in the roadshow materials is preliminary, unaudited, and subject to revision. Investors should carefully read SpaceX's S-1 Registration Statement and Prospectus filed with the SEC before making any investment decision to fully understand the associated risk factors.