As well as running a crypto exchange that didn’t exchange crypto and owning a hedge fund that didn’t hedge, Sam Bankman-Fried had a venture capital fund that didn’t venture its own capital.

⠀

The VC division, in contrast to the rest of the FTX group, can now provide some insight into where some of the money went. Here’s where it went:

⠀

⠀

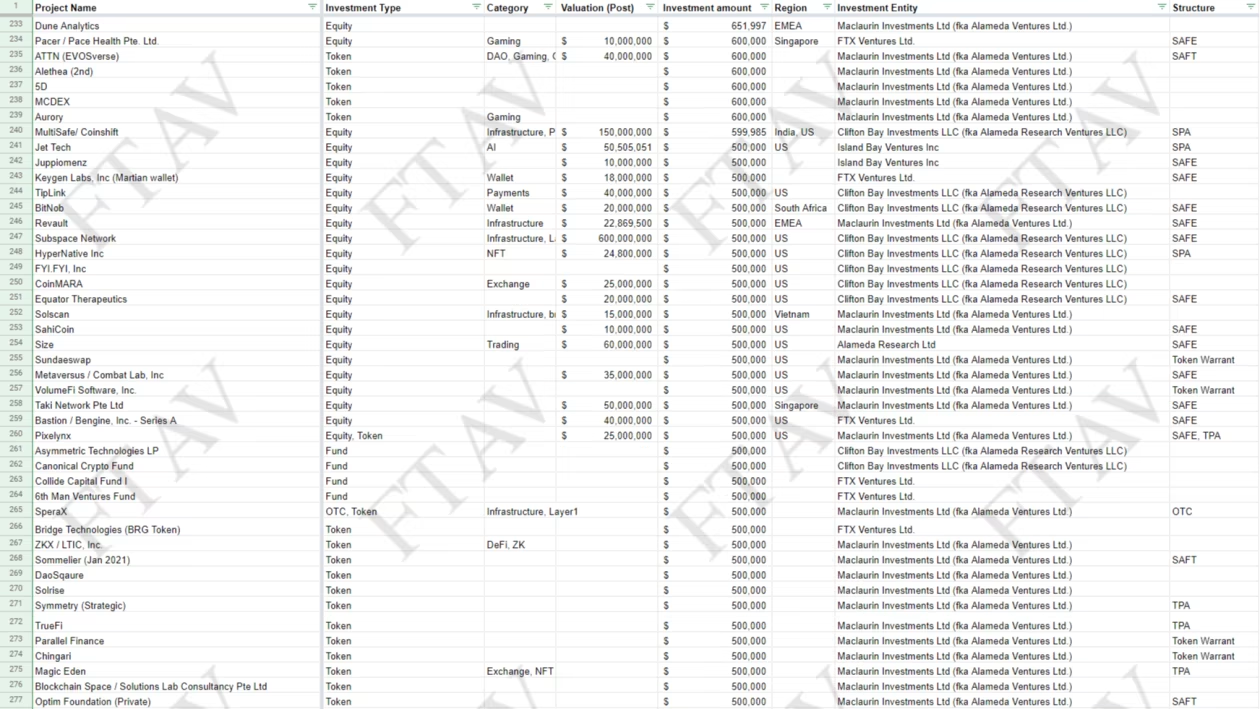

The screenshot above and all those below are taken from an Excel spreadsheet dated early November, when SBF was seeking rescue funding amid a run on FTX customer deposits. Mobile and app users are advised to click the magnifying glass below each image for more detail.

⠀

According to a person familiar with the rescue effort, the document shows an Alameda Research private equity portfolio — with some FTX bets mixed in — that was being offered as collateral in an attempt to secure a new credit line for the stricken group.

⠀

⠀

The disparate bundle of nearly 500 illiquid investments is split across 10 holding companies. The total investment value is given on the spreadsheet as in excess of $5.4bn.

⠀

⠀

As well as forming a central plank in efforts to maximise recoveries from FTX’s bankruptcy, the portfolio might offer regulators insight into whether the group’s trading and exchange businesses were ever operationally separate as claimed.

⠀

Bankman-Fried conceded in an interview with the Financial Times that he was involved in Alameda’s venture capital activities but has so far ducked questions around the misuse of FTX customer funds.

⠀

⠀

Going by the spreadsheet, boundaries between SBF’s companies were blurred. Two of Alameda’s biggest holdings, the crypto miner Genesis and the artificial intelligence research group Anthropic, are also listed on the draft FTX balance sheet published last month by FTAV. (Semafor subseqently reported that FTX had seized certain assets from Alameda after a margin call.)

⠀

⠀

As previously reported, the portfolio includes stakes in FTX backers Sequoia Capital and Anthony Scaramucci’s SkyBridge Capital, as well as in Elon Musk’s SpaceX and Boring Company projects through the investment in K5.

⠀

⠀

Of Alameda’s remaining investments, crypto and DeFi projects account for the majority. But the list also includes numerous start-up video game studios and betting platforms, online banks, publishers, a fertility clinic, a military drone maker and a vertical farming company,

⠀

⠀

Some entries have no clear link to an active business, suggesting they may be misspelt or mislabeled.

⠀

Note that FT Alphaville has excluded entries where an investment type is not given, which removes approximately a dozen names with a total stated investment of about $100mn. All other data are presented as they were shown to prospective FTX investors. The FT makes no claim as to the data’s accuracy or completeness.

⠀

⠀

When asked about why FTX used customer funds to prop up Alameda, SBF has repeatedly pleaded ignorance. The former FTX CEO said that to avoid conflicts of interest he chose not to get involved in Alameda’s trading and risk management, so before last month was not fully aware of its parlous state.

⠀

⠀

However, SBF told the FT that in early summer he had participated in conversations where Alameda’s financial health and borrowing were discussed. The venture capital investments Alameda had made were “effectively, some of them, on margin”, he added.

⠀

⠀

Alameda’s spreadsheet predates SBF’s current media blitz by a month, though it comes with all the same warnings about potentially selective recall and unreliable presentation, As the FT’s Joshua Oliver reports:

⠀

Bankman-Fried’s attempt to account for what went wrong was laced with caveats and references to his incomplete memory. He cited lack of “confidence” in his answers at least a dozen times, calling other responses “idle speculation” or “shitty answers”. At one point, he paused for half a minute with his head in his hands.

⠀

⠀

Caroline Ellison, former CEO of Alameda and SBF’s one-time romantic partner, could not be reached for comment.