Author: DWF Ventures

Compiled by: Deep Tide TechFlow

Deep Tide's Introduction: This report from DWF Ventures makes one thing clear with data: money hasn't left crypto, it has just shifted tracks. In 2025, over 80% of tokens traded below their initial offering price, while crypto IPO financing surged 48 times to $14.6 billion, and M&A reached a five-year high of $42.5 billion. This isn't just a matter of market mood; it's a systemic migration of capital structure, with a wave of IPOs including Kraken, Ledger, and Animoca on the way for 2026.

Core Conclusions

The old playbook for token offerings is over. High valuations and declining liquidity have hit investor confidence, and we are seeing a shift of funds towards equity.

Tokens and equity offer similar upside potential, but their risk structures are vastly different: tokens peak faster (within 30 days) and face greater volatility; equity, on the other hand, maintains steady gains over a longer time horizon.

Equity enjoys a higher valuation premium than tokens: this premium can be attributed to institutional access barriers, potential for index inclusion, and the richer trading strategies supported by equity.

Price-to-Sales (P/S) ratio provides a useful benchmark for company evaluation, but the dispersion in valuations reflects the importance of other factors, including regulatory moats, revenue diversification, shareholder value, and sector sentiment.

M&A activity hits a five-year high, consolidation accelerates: Acquiring capabilities is proving faster than building them, and regulatory compliance is driving strategic M&A.

The Current State of Token Offerings

The crypto industry has reached an inflection point. Billions of dollars are pouring in, institutional interest is at a peak, and regulation is becoming friendlier—yet for builders and users, everything feels gloomier than ever. The widening gap between institutional inflows and the morale of the crypto-native community is part of a larger problem—the original spirit of decentralization and cypherpunk experimentation seems to be fading with the influx and immense influence of centralized entities.

Crypto has also thrived in a high-risk, casino-like environment, which is being slowly stripped away as token performance plummets. This is also driven by extractive events that significantly impact retail investors, leading to liquidity withdrawal from the market.

According to a report by Memento Research, over 80% of tokens issued in 2025 are currently trading below their TGE price. Projects have been severely hit by high volatility and a general lack of token demand—due to high valuations that are difficult to justify and sustain. Upside is also scarce, with most tokens facing massive selling pressure from TGE—stemming from early profit-taking, lack of substantial confidence in the product, or poor token economic models (airdrops, CEX listings, etc.). This has dampened investor and retail interest, and events like 10/10 have further exacerbated crypto outflows, calling into question the industry's core infrastructure.

The Rise of IPOs

Meanwhile, in traditional markets, IPOs are gaining strong traction among crypto companies—2025 saw many notable listings, and more companies are filing for upcoming IPOs. Data shows that crypto IPO financing increased 48 times compared to 2024, raising over $14.6 billion in 2025. M&A deals experienced similar growth, with leading core companies seeking to diversify their offerings, which we explore further below. Overall, the strong performance of these companies demonstrates a robust market demand for digital asset exposure, a momentum likely to accelerate further into 2026.

The Flow of Liquidity

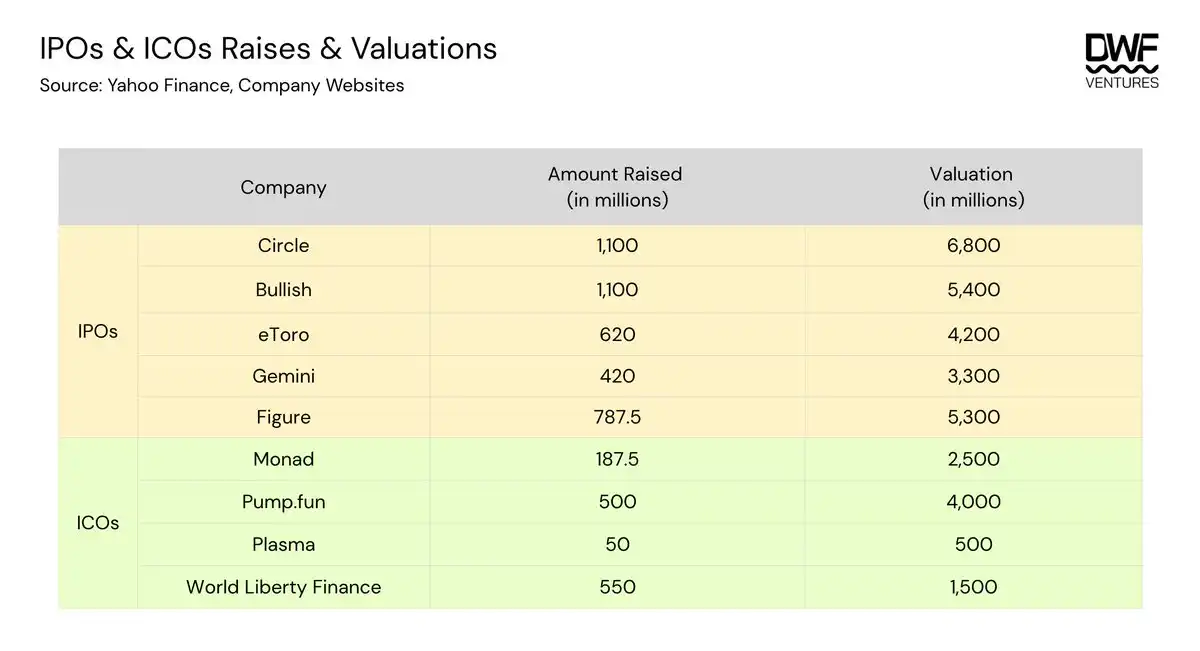

Over the past year, we have seen high-profile IPOs and ICOs both raise significant capital. The table below shows the funding amounts and initial valuations for various companies.

From this, we observe that IPO and ICO valuations are relatively close. Some ICOs, like Plasma, were specifically priced below the valuation for institutional investors, aiming to provide greater upside and participation opportunities for retail investors. On average, the public float for IPOs ranges from 12% to 20%, while for ICOs it ranges from 7% to 12%. World Liberty Finance is a clear exception, offering over 35% of the total supply for sale.

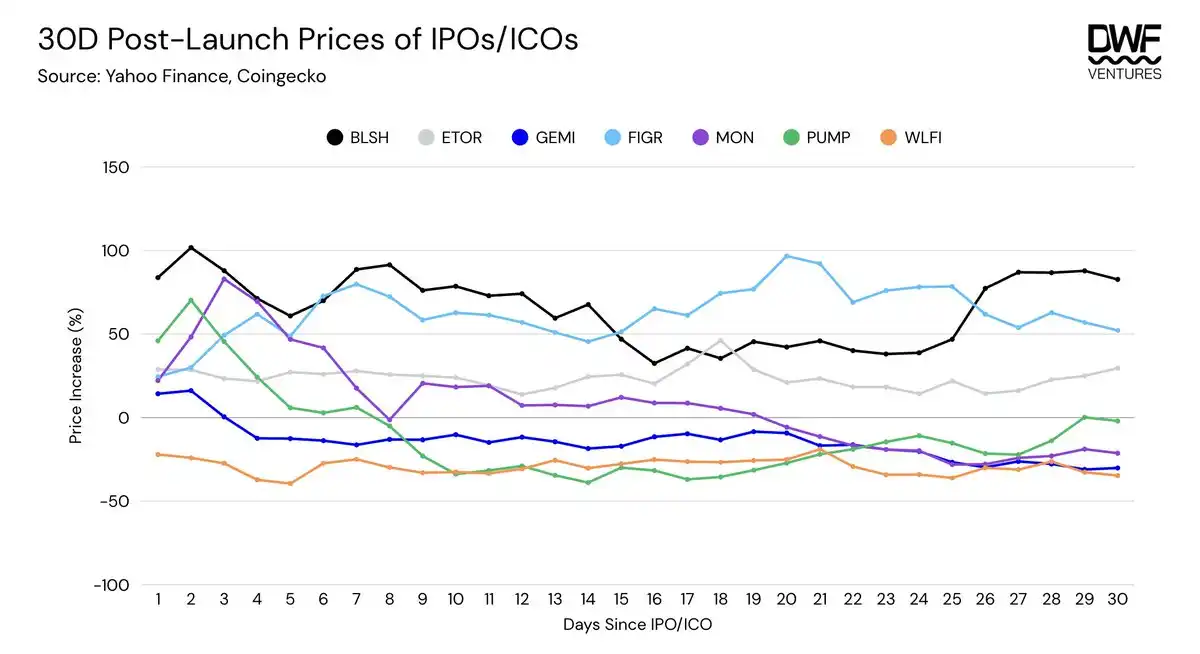

Analyzing the performance of ICOs and IPOs, tokens are associated with greater short-term volatility and a shorter time to peak (within 30 days). On the other hand, equities tend to record steady gains over a longer time horizon. Notably, however, the upside potential is similar for both.

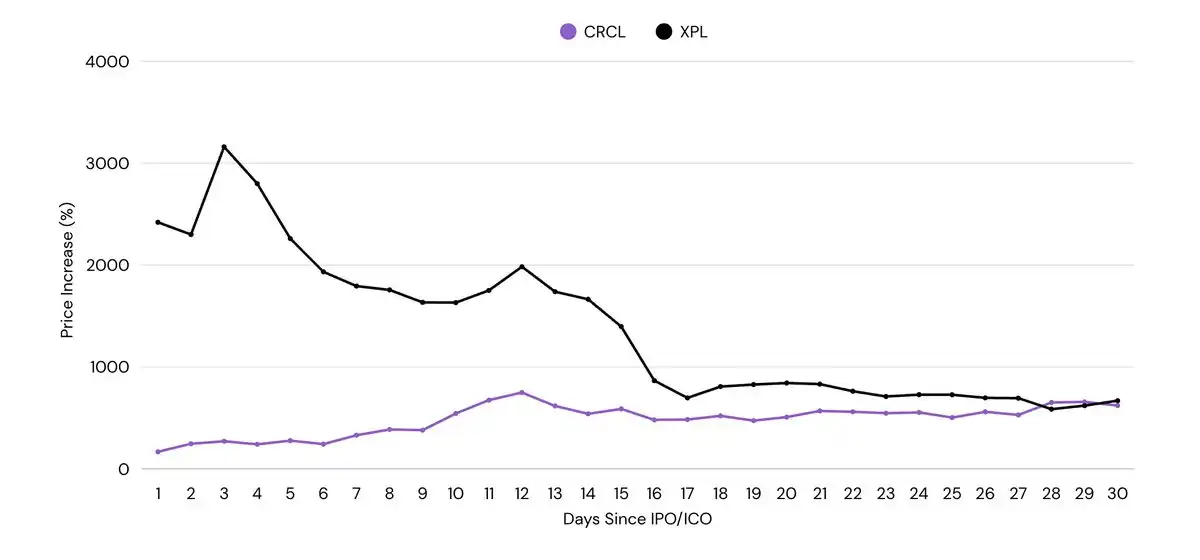

CRCL and XPL are exceptions, having experienced massive gains from the start, offering investors 10x to 25x upside. Nonetheless, their performance also followed the aforementioned trend—XPL retraced 65% from its peak within two weeks, while CRCL climbed steadily over the same period.

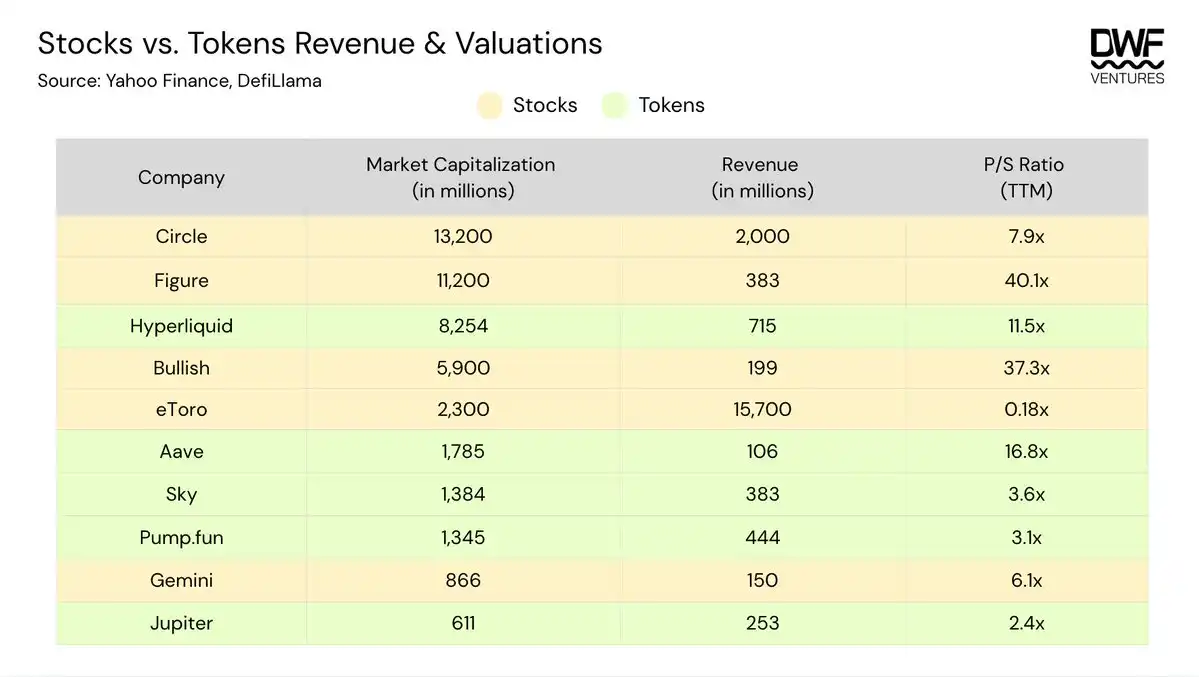

Revenue: Assessing the Equity Premium

Delving into revenue figures, stocks overall enjoy a higher premium than tokens, with P/S ratios in the ranges of 7-40x and 2-16x, respectively. This can be attributed to enhanced liquidity from several factors:

Institutional Access: Despite growing positive sentiment around holding digital assets on balance sheets, this remains limited to funds with securities-only mandates (particularly pensions or endowments). Opting for an IPO allows companies to tap into this pool of institutional capital.

Index Inclusion: The growth tailwinds in public markets are far stronger than on-chain. Coinbase's inclusion in the S&P 500 in May 2025 as the first crypto company likely contributed to buying pressure from index-tracking funds/ETFs accumulating positions.

Alternative Strategies: Compared to on-chain tokens, equity enables a wider variety of institutional strategies, including options and leverage, whereas on-chain tokens often lack liquidity and counterparties.

Overall, the P/S ratio shows a company's valuation based on the last 12 months of revenue, helping to judge whether a company is undervalued or overvalued relative to its peers. However, factors beyond the numbers that reflect investor sentiment are not captured. Some factors to consider when evaluating stocks/tokens include:

Moats & Diversification: In the fast-evolving digital asset industry, this is crucial. The market is paying a premium for licenses and regulatory compliance, while diversified business models strengthen the value proposition of the core business beyond pure revenue numbers.

For example, Figure launched its own RWA lending pools, open to retail and institutional investors, and became the first SEC-approved yield-bearing stablecoin ($YLDS). Bullish is a regulated exchange that also owns other businesses like CoinDesk, enhancing its value beyond pure trading services. These factors likely contributed to higher premiums.

In contrast, eToro has an extremely low P/S, seemingly "undervalued" on the surface, but a deeper analysis reveals its revenue growth climbing in sync with costs, which is not optimal. Furthermore, the company is purely focused on providing trading services, lacking differentiation and having low margins. This indicates that building defensible moats and diversified business models are also key considerations for investors.

Shareholder Value: Returning capital to investors through buybacks is common in both stocks and tokens, especially for high-revenue companies.

For example, Hyperliquid has one of the most aggressive buyback programs, with 97% of revenue used for buybacks. Since genesis, the aid fund has bought back over 40.5 million HYPE tokens, representing over 4% of the total supply. Such aggressive buybacks impact the price, boosting investor confidence as long as revenue remains stable and the sector has room for growth. This leads to a higher P/S ratio but does not necessarily mean the token is "overvalued," as strong support from the team itself is real.

Sector Sentiment: High-growth sectors driven by institutional or regulatory dynamics naturally command a premium, as investors seek exposure.

For example, Circle's stock price soared quickly after its IPO in June 2025, with the P/S ratio peaking at around 27x. This could be attributed to the passage of the GENIUS Act—a framework dedicated to legitimizing stablecoin adoption and issuance, introduced shortly after Circle's listing, which would make Circle a major beneficiary as a leading player in the stablecoin infrastructure space.

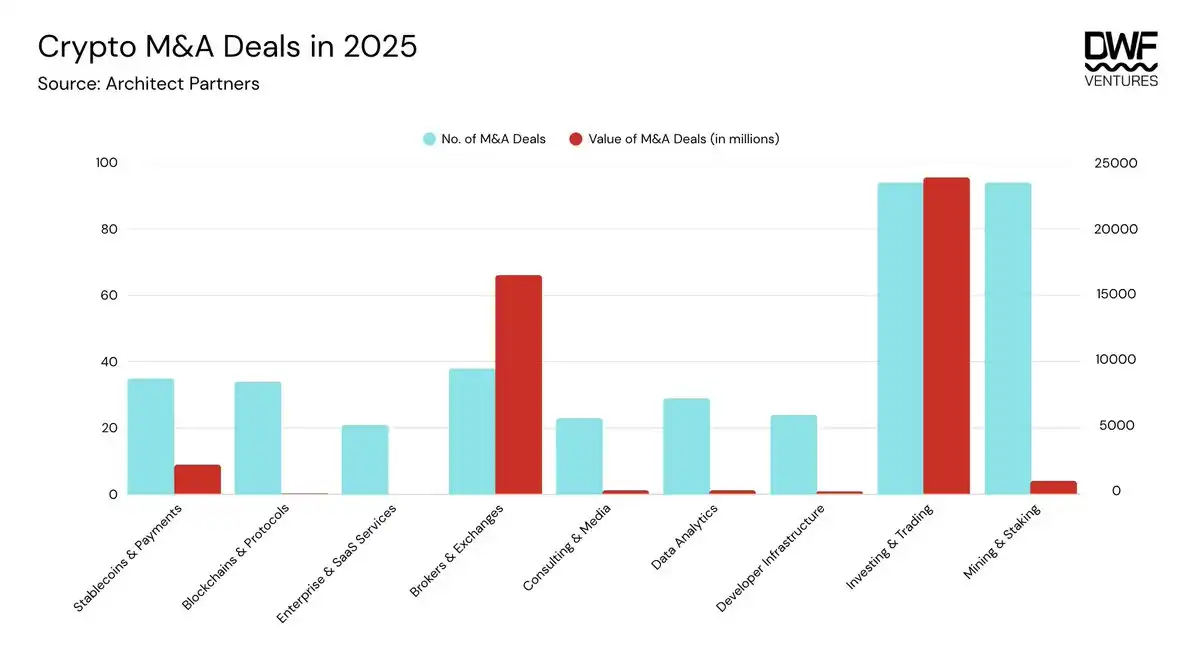

M&A: The Great Consolidation

According to the report, crypto M&A activity hit a five-year high in 2025—driven by massive entry from TradFi institutions, coupled with more friendly regulatory sentiment. After the Trump administration rolled out a series of crypto-friendly policies, the Digital Asset Treasury (DAT) frenzy emerged, making holding digital assets on balance sheets less controversial. Companies also shifted focus to acquisitions, as it is a more efficient way to obtain specific licenses for better compliance. Overall, the introduction of appropriate regulatory frameworks laid the groundwork for M&A acceleration.

Looking back over the past year, we see a clear rise in the number of deals across categories. The following three categories have become priorities for institutions:

Investment & Trading: Encompassing trade settlement, tokenization, derivatives, lending, and DAT infrastructure;

Brokers & Exchanges: Regulated platforms focused on digital assets;

Stablecoins & Payments: Covering on/off-ramps, infrastructure, and applications.

These three categories together accounted for over 96% of the deal value in 2025, totaling over $42.5 billion.

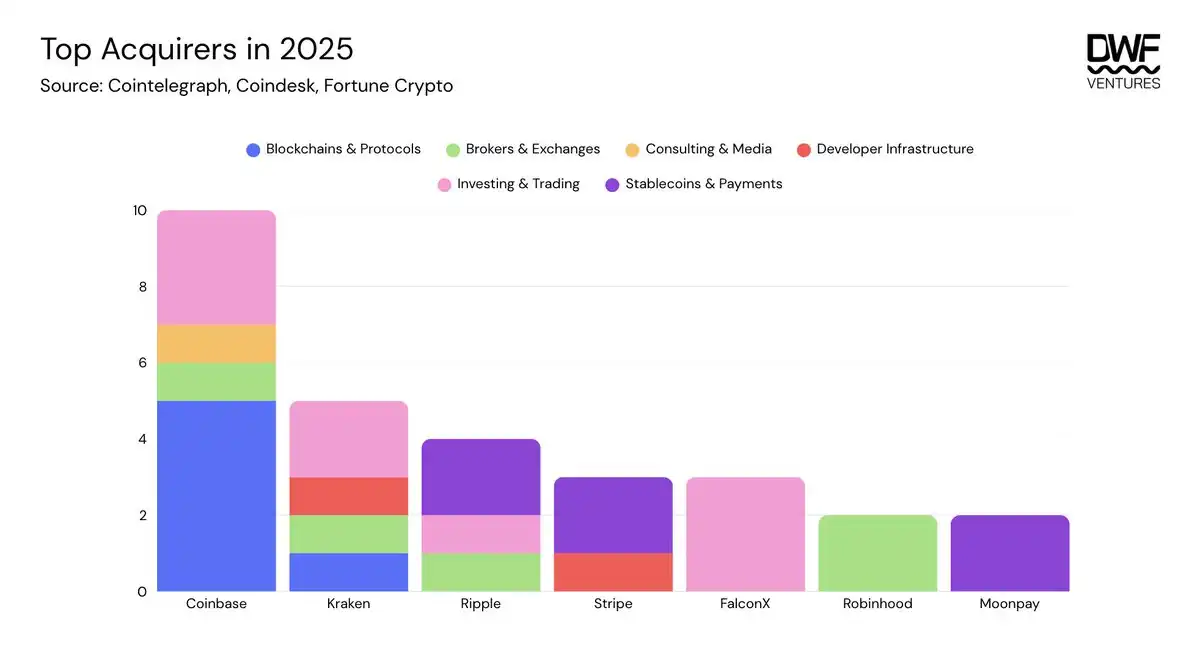

Top acquirers include Coinbase, Kraken, and Ripple, all involved in multiple categories. Among them, Coinbase's moves are particularly prominent, highlighting its ambition to become a "one-stop super app," with a core focus on bringing on-chain to the masses through acquisitions of both traditional and innovative DApps. This is driven by intensifying competition among exchanges and the quest for all-in-one traffic portals.

Companies like FalconX and Moonpay are deeply cultivating their own categories, building full-service capabilities through complementary acquisitions.

The Next Step for Token Offerings

Despite the current market environment and sentiment, we believe 2026 will continue to bring significant tailwinds to the digital asset space. We expect more companies to go public, which is a net positive for the industry overall—it provides access to a larger pool of capital and investors, making the overall pie bigger.

The next batch of IPO candidates includes:

Kraken: Filed an S-1 registration statement with the SEC in November 2025, with strong expectations for an IPO in early 2026;

Consensys: Reportedly working with Goldman Sachs and JPMorgan to prepare for a mid-2026 listing;

Ledger: Targeting a $4 billion valuation, advancing its IPO with Goldman Sachs, Jefferies, and Barclays;

Animoca: Plans to list on Nasdaq in 2026 via a reverse merger with Currenc Group Inc.;

Bithumb: Aims to list on Korea's KOSDAQ in 2026 with a $1 billion valuation, underwritten by Samsung Securities.

The way forward is not a choice between TradFi validation and crypto-native innovation—it is fusion. For builders and investors, this means prioritizing fundamentals and building useful products that generate real, sustainable revenue. A shift towards a long-term mindset may cause some turbulence, but those who adapt will be able to capture the next wave of value creation.

The token is dead, long live crypto.