The cost of an Apple iPhone over the years has only gone up. But has the iPhone price over the past decade outpaced the price of BTC, or ETH? Not even close, according to a new report from the folks at CoinGecko. The research team at CoinGecko went on a deep dive into the price archives for BTC and ETH, looking back over more than a decade, and cross-referenced crypto prices to iPhone MSRPs.

⠀

Lets take a look at the CoinGecko report and it’s key insights.

⠀

iPhone Prices Dwindles As Decades Go On… When Measured In BTC & ETH

⠀

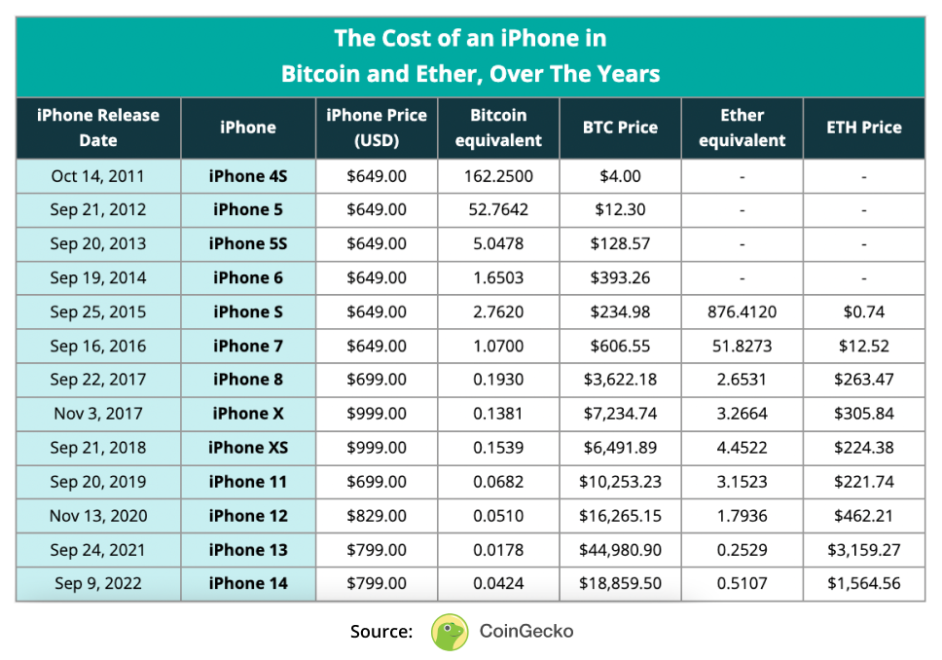

On the heels of the iPhone 13 release, and the announcement of the new iPhone 14, we’ve learned that the standard iPhone 14 models will start at $799 and their pre-order window has just opened up. A key perspective from CoinGecko’s insights is that the retail price of an iPhone over the past decade – from the iPhone 4S where CoinGecko’s research window begins – actually has remained somewhat stable.

⠀

The retail price of the 4S was $649.00, and with today’s 14 at $799.00, that represents an increase of roughly 25% over the past decade, with no inflation adjustment. Peak iPhone prices can be seen in 2017 and 2018 with the X and XS, respectively, with both models priced at $999.00. Take a look at how these prices have evolved with the price of Bitcoin below:

⠀

⠀

In 13 models released over the past 11 years, just 3 models saw their Bitcoin equivalent increase from the following year. Similar sentiments exist when comparing the price against Ether, as well, since it’s genesis in 2015. In just three occasions in the last nine iPhone releases was a phone more expensive in ETH than the model prior:

⠀

⠀

Callouts From The CoinGecko Report

⠀

There’s a few additional key callouts from the CoinGecko report:

⠀

The price slide in the market this year: BTC saw highs at nearly $70K earlier this year before tumbling back to earth. This led to the largest % increase from one model to the next, resulting in 13 models priced at 0.0178 BTC last year turning into 14 models priced at over 2X that, at 0.0424 BTC. Bitcoin, of course, is the primary market mover across altcoins too, so a similar sentiment can be expressed with ETH, which saw a respective increase of 0.2 ETH last year to 0.5 ETH this year.

⠀

A sound investment? Relatively speaking: Since the release of the iPhone 4S just over a decade ago, BTC and ETH have experienced nearly 500,000% and 250,000% percent gains, respectively. Compare that to iPhones 23% increase. This is to be taken with a grain of salt – it’s almost apples and oranges – but worth consideration when we think about the growth and respect that crypto assets have earned over the years.