原文作者:马赫,Foresight News

5 月 5 日,美国上市加密资产平台 Bullish 与私募股权公司 Siris Capital 达成最终协议,将以 42 亿美元总对价收购 Equiniti。该交易由 18.5 亿美元 Equiniti 现有债务承担以及约 23.5 亿美元 Bullish 股票对价组成,股票发行价格基于截至 2026 年 5 月 4 日收盘前 30 个交易日成交量加权平均价(VWAP)每股 38.48 美元计算,交易尚需进行惯例购买价格调整。

交易预计将于 2027 年 1 月完成,届时需获得监管部门批准及其他惯例成交条件满足。公告发布后,Bullish 股价一度上涨至最高 48.93 美元,涨幅超 11%。

Equiniti:传统资本市场核心「户籍管理」服务商

Equiniti 成立于 19 世纪末,是转让代理和股东服务提供商,主要为上市公司提供注册股东记录管理、股票发行 / 转让 / 注销、股息发放与再投资、股东沟通、企业行动处理、税务申报等核心服务。

Equiniti 目前为近 3000 家上市公司担任转让代理,服务超过 1.5 万家企业客户,管理超过 2000 万名验证股东,每年处理约 5000 亿美元的支付款项。

Equiniti 在美国证券交易委员会(SEC)注册为转让代理,在英国受金融行为监管局(FCA)监管,具备成熟的合规框架和跨市场运营能力。

2021 年,Siris Capital 收购 Equiniti,并将其与美国同行 AST 合并,形成规模化全球转让代理平台。

收购逻辑直指代币化万亿蓝海

收购完成后,Bullish 旗下拥有交易平台 Bullish Exchange、媒体 CoinDesk 以及端到端的代币化基础设施服务。

2025 年第四季度财报披露,Bullish 调整后收入达到 9250 万美元,同比大幅增长(2024 年同期为 5520 万美元);调整后 EBITDA 达 4450 万美元,同比大幅提升,毛利率达 48%。全年调整后收入约 2.885 亿美元,同比增长约 35%。订阅、服务及其他收入在 Q4 单季达 5460 万美元,同比激增 284%,得益于期权交易推出、机构客户资金增长以及代币化流动性服务扩张。2 月 5 日其股价触及最低点 24.79,财报公布后,连涨 2 日一度触及 32 美元。

交易完成后,Bullish 与 Equiniti 的合并实体预计 2026 财年将产生约 13 亿美元调整后总收入。

2027-2029 年,合并公司预计实现 6%-8% 的复合年收入增长,其中代币化与区块链服务贡献 20% 的收入增速。

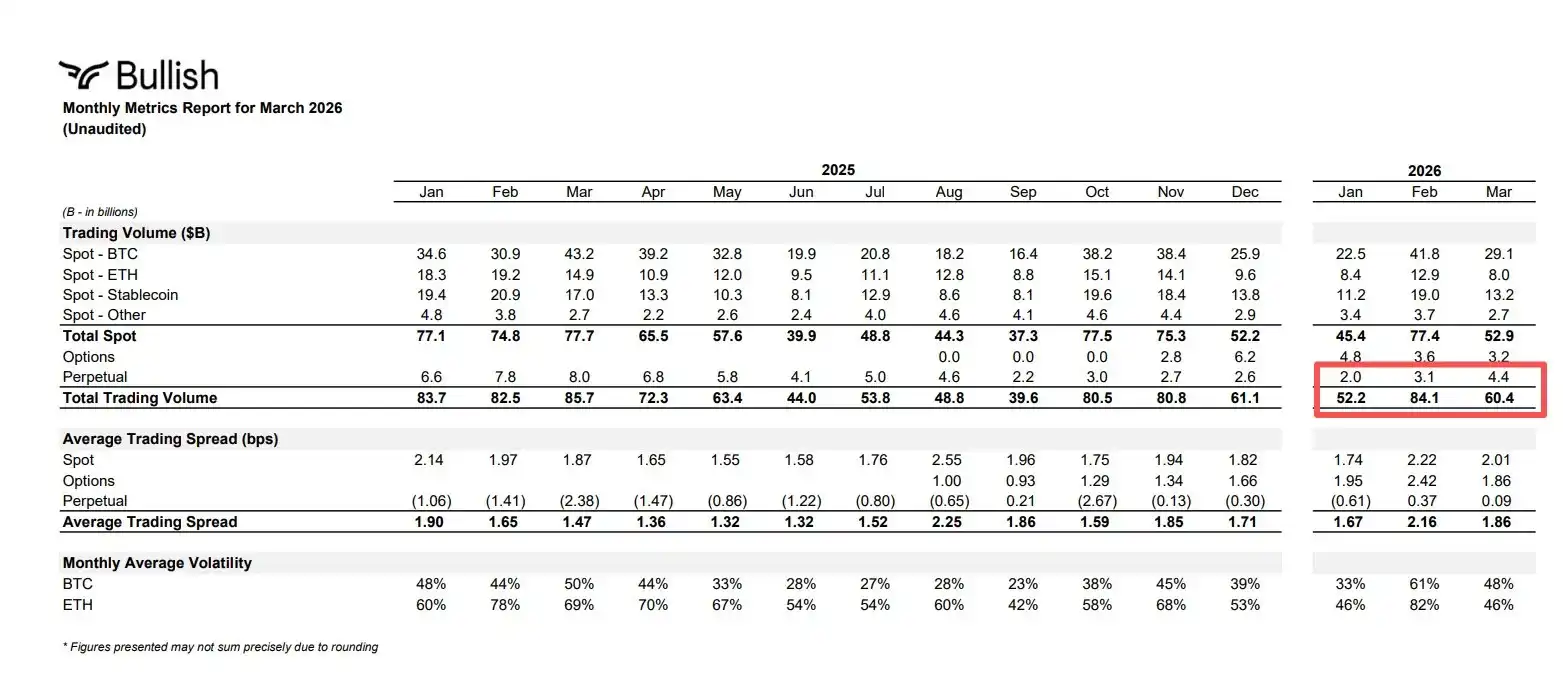

今年 3 月,Bullish 总交易量为 604 亿美元,较 2 月份的 841 大幅下降约 28% 。但是 Bullish 的 3 月永续合约成交量达到 44 亿,创下了 2025 年 5 月以来的新高,而且这是在总交易量下滑的情况下实现了逆势增长。

Crypto 生态中,RWA 已被视为下一代万亿级赛道。传统转让代理的瓶颈在于手动处理、延迟结算和高成本,而区块链技术可实现即时所有权转移、 碎片化所有权和全球 24/7 流动性。

Bullish 此举或许是对标 BlackRock、BNY Mellon 等传统巨头布局 RWA 的加密版回应,先将「受监管转让代理 + 加密交易所 + 媒体数据」三者合一,构建闭环生态。

前纽约证券交易所总裁、Bullish 首席执行官 Tom Farley 在公告中强调:「代币化是资本市场运作方式的代际转变,是未来 25 年最具定义性的基础设施趋势。机构级大规模采用需要三要素:端到端代币化服务、单一统一账本,以及规模化的蓝筹发行人关系。本次合并一次性交付了这三要素。」

这也意味着 Bullish 将从交易收入主导的模式,逐步转向高毛利基础设施服务,抗周期能力或许将显著增强。