I’m currently reading Alchemy of Finance by George Soros, and it inspired me to write this stream of consciousness piece about my macro thesis regarding the ETH merge. Soros is the GOAT when it comes to macro investing. Acolytes of his — such as Paul Tudor Jones and Stan Druckenmiller— are superstars in their own right, but they owe a lot of their success to the strategies and principles elucidated by Soros over the years. Alchemy of Finance presents a fascinating philosophical discussion about what drives markets — and if you are serious about the craft of managing your own or others’ money, it’s a must-read.

Soros’ central theory — which he dubs the “theory of reflexivity” — is that there is a feedback loop between market participants and market prices. The basic idea is that market participants’ perception of a given market situation will influence and shape how that situation plays out. The expectations of market participants influence market facts (or so-called “fundamentals”), which, in turn, shape participants’ expectations, and so on and so forth. To put it even more simply, the participants — consciously or not — often play a major role in bringing about the very future they speculate on. Their biases can reinforce a rising or falling price trend because the future becomes a self-fulfilling prophecy.

That’s a very short and incomplete explanation of the theory of reflexivity — but I’ll explain it in more detail as we go on. For now, let’s bring this back to crypto and how it relates to the merge.

The Inputs

The Event

Either the merge happens, or it doesn’t. That is the future event we are trading. The merge itself is unaffected by the price of ETH, and will succeed or fail solely based on the skills of the Ethereum core developers.

Structural Flows

The merge will do two things:

1.It will remove the Proof-of-Work ETH emissions on each block (i.e., the ETH that was being paid to miners in exchange for the computation power they provided to maintain the network). At present, these emissions total ~13,000 ETH per day. The merge is expected to replace these ~13,000 daily ETH emissions to miners with a much smaller emission of approximately 1,000 to 2,000 ETH per day that will instead go to network validators (i.e., folks staking ETH, who receive more ETH in exchange for helping determine which ETH transactions are valid and which are not). These emissions will occur at the same rate regardless of the price of ETH and the Ethereum network’s usage.

2.A certain amount of gas fees will be burnt every block (meaning the ETH used to pay those fees will be permanently removed from circulation). This variable depends on the usage of the network. The usage of the network is a reflexive variable, which I will explain in more detail later.

Total ETH Inflation = Block Emission — Gas Fees Burnt

I will treat Block Emission as a constant under the current local conditions. These local conditions could be violated, but it would in the very long term (i.e., on the order of hundreds of years). So, we can therefore comfortably treat this variable as a constant.

Gas Fees Burnt is dependent on the usage of the network.

Inflation = Block Emission > Gas Fees Burnt

Deflation = Block Emission < Gas Fees Burnt

Those who believe ETH will become a deflationary currency must also believe that the network usage (and therefore, the amount of ETH burned in fees paid by users) will be high enough to nullify the amount of ETH emitted every block as a reward for validators. To assess whether or not they are likely to be right, though, we must first ask — what determines how much a given crypto network like Ethereum gets used?

A user has many choices when picking a layer-1 smart contract network chain. Other layer-1 chains include Solana, Cardano, Near, etc. The following are the factors that I believe influence a user to choose one chain over the other:

1.Mindshare — Which chain is more widely known? Social media and blog posts are the primary mediums through which information is disseminated about various layer-1 chains.

Applications — Which network has the most robust set of decentralised applications (dApps)? Which of these applications are category leaders? Which of these applications have the most liquidity for trading? etc.

Mindshare

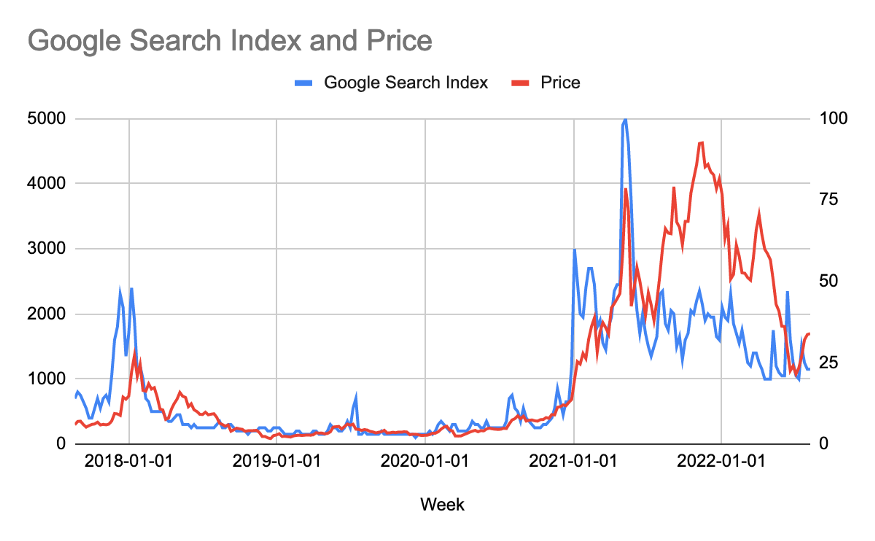

2.Mindshare and the price of ETH have a reflexive relationship. The above chart shows the Google search trends for “Ethereum” and the price of ETH. As you can see, they are very closely correlated. If I run a correlation between the two data series, the r = 0.77. Conceptually, this makes sense. Interest in the Ethereum network rises and falls with the price of its native token — and as the price rises, more people hear about ETH and want to buy in and use the network, driving the price up further.

Applications

The quality of the applications on a network starts with the quality and quantity of its engineers. As a developer, you create things for people to use. If there is no one using the network, you aren’t likely to develop on it. Obviously, a developer would like to code in a language they know well, but that preference is secondary to the number of users one can interact with on a given decentralised network.

The number of developers is directly related to the number of users their creations can service. And as we established above, the number of users of a given network is directly related to the price of its native token. And since the number of users and the price share a reflexive relationship, then the number of developers and the price must also share a reflexive relationship. As the price goes up, more people hear about Ethereum, more people use the network, and more developers are drawn to develop applications on the network to attract its large and growing user base. The better the applications, the more users join the network. Round and round we go — reflexivity 101.

The Outputs

The magnitude of the deflation of ETH is dependent on the amount of gas fees burnt.

The amount of gas fees burnt is dependent on the amount the network is used.

Network usage is dependent on the number of users and quality of applications.

The amount of users and quality of applications have a reflexive relationship with the price of ETH.

Therefore, by the transitive property, the magnitude of deflation and the price of ETH have a reflexive relationship.

With that in mind, there are two potential future states of the world.

The Merge Happens:

If the merge is successful, there is a positive reflexive relationship between the price and the amount of currency deflation. Therefore, traders will buy ETH today, knowing that the higher the price goes, the more the network will be used and the more deflationary it will become, driving the price higher, causing the network to be used more, and so on and so forth. This is a virtuous circle for bulls. The ceiling is when all of humanity has an Ethereum wallet address.

The Merge Does Not Happen:

If the merge is not successful, there will be a negatively reflexive relationship between the price and the amount of currency deflation. Or, to put it another way, there will be a positively reflexive relationship between the price and the amount of currency inflation. Therefore, in this scenario, I believe traders will either go short or choose not to own ETH.

There is a floor to this relationship in that the network is the longest operating decentralised network. ETH hit a very large marketcap without a merge narrative. The most popular dApps are built using Ethereum, and Ethereum also possesses the largest number of developers of any layer-1 chain. In light of that, and as I mentioned in my previous essay “Max Bidding”, I believe that ETH won’t go lower than the $800 to $1,000 prices it experienced during the TerraUSD / Three Arrows crypto credit meltdown.

The Market’s Opinion

We now need to determine what we think the market believes regarding whether the merge will succeed or fail.

In my view, that is best ascertained from the chart below, which shows the ETH/BTC exchange rate. The higher it goes, the more ETH outperforms Bitcoin. As Bitcoin is the reserve asset for the crypto capital markets, if ETH is outperforming it at this stage, to me, that means the market believes that a successful merge is growing more and more likely.

Since the aftermath of the crypto credit unwind, ETH has outperformed BTC by approximately 50%. So, I think it’s fair to assume the market is becoming more and more confident that a successful merge is on the horizon. The current expected merge date — as put forward by the Ethereum core developers — is 15 September 2022.

But that’s just the spot market’s opinion. What do we think derivatives traders believe?

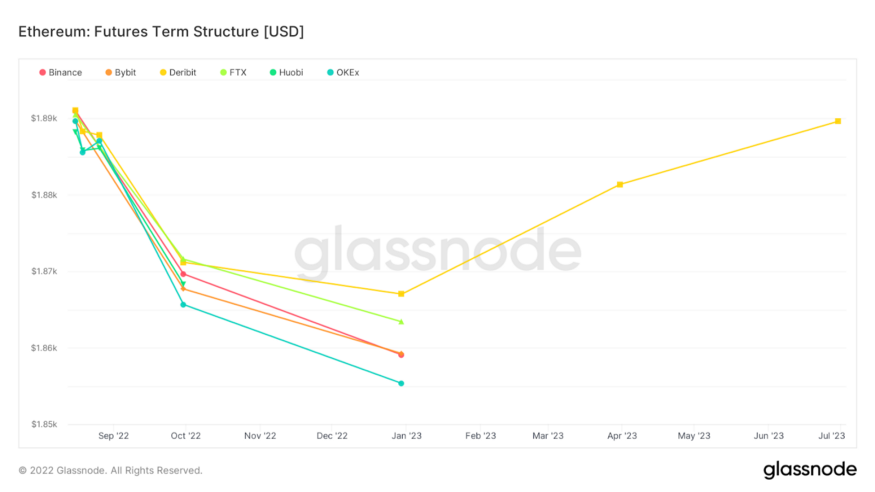

The above chart illustrates the futures term structure for Ether. The futures term structure plots current prices of futures contracts by their maturities. It allows us to make predictions about supply and demand conditions for different maturities by calculating the premium or discount of a futures contract vs. the underlying spot price.

Backwardation = Futures Price < Current Spot Price; Futures Trade at a Discount

Contango = Futures Price > Current Spot Price; Futures Trade at a Premium

Given that the entire curve out to June 2023 is trading in backwardation — meaning that the futures market is predicting ETH’s price by the maturity date will be less than the current spot price — there is more sell pressure than buy pressure at the margin.

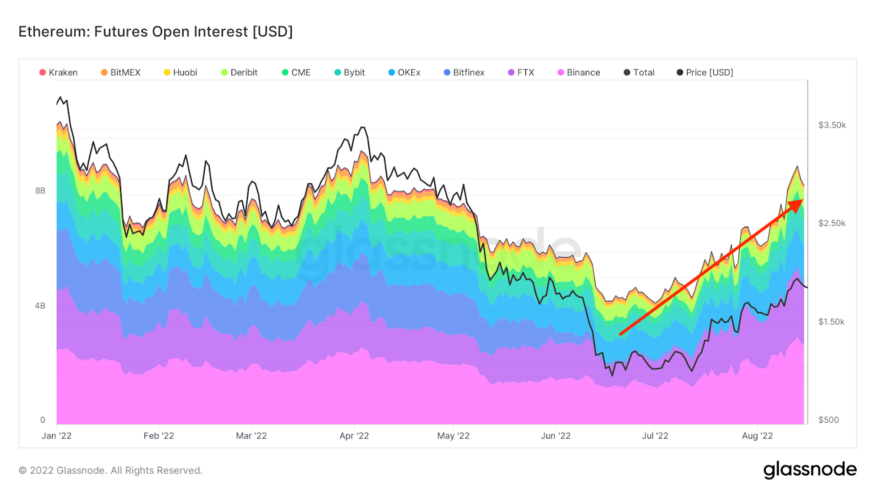

This is a chart of the open interest on ETH futures. Open interest is the total number of open futures contracts held by market participants at a given point in time. As you can see, it is rising off of the lows experienced during the crypto credit meltdown in mid-June. The open interest is increasing at the same time the curve is in backwardation. To me, that points to a high and rising sell pressure at the margin. Conversely, if the curve were in contango (futures price > current spot price) and the open interest were increasing, that would suggest high and rising buy pressure at the margin.

There are two potential reasons for the current sell pressure:

1.You are long physical ETH, but are unsure about whether the merge will be successful or when it will happen — so you fully or partially hedge your ETH exposure by selling futures contracts at prices higher than the current spot price.

You expect the merge to occur, and want to be able to pick up the free chain-split tokens that will be minted and distributed to all ETH holders when some faction of the ETH faithful inevitably resists the merge and creates a fork to maintain an ETH Proof-of-Work chain. So, you are long physical ETH — but you also want to hedge out your ETH exposure by selling futures contracts. If you sell the futures contract at a discount that is less than the value of the chain-split token(s) received, then you make a profit.

2.On the other side of these directional futures flows are the market makers. They run delta-neutral portfolios, meaning they take no outright exposure to ETH. Therefore, as they buy futures from the sellers, whose motivations I described above, they must sell ETH physically in the spot market to hedge themselves. This adds sell pressure to the spot or cash market.

But remember — I just showed you that ETH has outperformed BTC by 50%. The selling by the market makers in the spot market is no match for the long flows of the bulls. This is bigly encouraging. It means the market’s confidence in a successful merge is UNDERSTATED, and masked by the short spot hedging flows of the market makers.

1.If the market believes the odds of the merge happening is growing day by day, what happens to all those who hedged via futures contracts if the merge is successful?

2.If the merge is successful, those who own spot ETH will buy back their hedge so they are long ETH and can benefit from the positive reflexivity I described above.

If the merge is successful and chain-split tokens are distributed, they will be sold for whatever they are worth, and those who hedged their positions will immediately unwind them. Now, they may decide to sell spot ETH to completely close out their position– but I bet that those traders will be in the minority. The ETH will be uncovered, and can benefit from the positive reflexivity.

I believe a successful merge will lead to buying pressure at the margin, flipping the market makers’ futures positioning in the process. They will go from long futures / short spot to flat or short futures / long spot. The spot they are short must be covered (that means buying spot), and if they get taken net short futures, they must now go into the market and purchase additional spot. The unwind of the derivatives flows that lead to backwardation pre-merge will lead to contango post-merge.

Trading Decisions

For those who believe the merge will successfully occur on schedule-ish, the question then becomes: how should you express your bullish view?

Spot / Physical ETH

The most straightforward trade is to sell filthy fiat for ETH, or be overweight ETH in your crypto portfolio.

Lido Finance

Lido Finance is the largest Ethereum Beacon Chain validator. Lido allows you to stake ETH with them to earn validator rewards. In return, Lido takes 10% of the ETH rewards earned. Lido has a DAO that issued a token, LDO.

If you want to take even more merge risk, this is an attractive option. It is riskier than owning spot ETH, because the value proposition of Lido is entirely dependent on the merge being successful– whereas with spot ETH, it may still be successful sans-merge because it has other value propositions (i.e., it powers the second large public blockchain by marketcap).

As a result of this higher beta play on the merge, LDO is up over 6x since the crypto credit meltdown in mid-June.

Long ETH Futures

For those who want more juice by adding leverage to the trade, going long ETH futures is a good option. Due to the negative basis, long futures holders get paid to take ETH exposure.

Basis = Futures — Spot

Looking at the term structure, the December 2023 expiring futures contracts are the cheapest. If the merge is successful, due to the time value remaining, these should swing violently into contango as shorts cover. The September 2023 expiring futures contracts will have 1 to 2 weeks of time value remaining post-merge, and you will not get the same basis effect as if you went long the December futures.

Long ETH Call Options

For those who like leverage but don’t want to worry about getting liquidated like you would with futures contracts, buying call options is a good strategy. The current implied vols on the Sept and Dec futures trade below realised vol. This is expected, as hedgers not only use futures contracts, but use options as well.

Anecdotally, when I have gone into the market to buy my Dec 2022 $3,000 strike ETH call options, I have been able to trade near the offered price for a much larger size than is on the screen. I am told this is because the dealers are all massively long call options, as the hedgers were call overwriting to hedge their long ETH positions. The dealers are very happy to reduce their long call option exposure because it frees up margin, and they are showing very tight prices on the offer side.

Similar to the futures term structure, the Dec calls trade cheaper in terms of implied vol than the Sept calls, especially on the wings. Another reason why I prefer the Dec calls is that I don’t have to be as precise with the timing of the merge. While the developers told us September 15 is the date, tech delivery dates are known to slip. I don’t want to worry about being a few weeks off on the merge completion date.

If you didn’t understand anything I just said, stick with simpler products so I don’t see your mugshot on Faces of REKT.

Long Dec Futures vs. Short Sept Futures

This is a curve-steepening play. You need to watch your margin very carefully. While you have no exposure to the ETH price, on one leg you will show an unrealised loss, and on the other leg an unrealised profit. If the exchange in question does not allow you to offset these, then you will have to put additional margin against the losing leg of the trade — otherwise, you will get liquidated.

You are short Sept futures trading at a discount, which means you pay theta (or time value). You are long Dec futures trading at a discount, which means you receive theta. When you net the theta exposure, you actually make money every day due to the net positive theta (assuming no movement in the spot price). If we believe there will be intense short covering post-merge, the Dec futures will move higher than the Sept futures. Therefore, the curve will steepen, and you will make more money on your long Dec position than you lose on your short Sept position.

(Sorry about the jargon– just remember the note about Faces of REKT in the previous section.)

Buy the Rumor, Sell the Fact?

Assuming you are long via some ETH-related instrument, the question becomes — do you reduce or close your long position entirely right before the merge happens?

As the positive reflexivity drags the price of ETH higher pre-merge, textbook trading suggests that you should at least reduce your position right before the merge. But, actual reality rarely lives up to expectations.

However…

The structural reduction in inflation will only happen post-merge. I expect we will see it play out similar to Bitcoin halvings — i.e., we all know the dates they will occur, and yet, Bitcoin still always rallies post-halving.

That said, it’s possible the price of ETH dips slightly heading into and right after the merge. Those who cut partially or fully would initially feel great about their decision. However, as the deflation kicks in, and due to the reflexive relationship between a high and rising ETH price and usage of the network, the price could keep gradually grinding higher. At that point, you would have to decide when to get back into your position. This is usually a very mentally challenging trading situation. You believed in the long-term trend, but wanted to trade around your position– and now, you must pay higher prices to re-establish your position. It hurts, because you are always waiting for that dip when you know it’s time to buy back in. But the dip — or at least, a dip to the extent you are looking for — never happens, and you either never reestablish the same size position, or you miss out on a large portion of the gains.

With that thought experiment in mind, and my conviction about the reflexivity of this situation, I will not reduce my position going into or right after the merge. If anything, I will add to my position if the market sells off– as I believe the best is not (and cannot) be priced into the market today.

How to Sell

To be intellectually thorough, we must also consider the best strategy to short the merge event occurring. Given the current market sentiment and price action, those going short ETH pre-merge are trading against positive reflexivity. That is a very dangerous situation. When you short something, your maximum gain is 100% unlevered, as the price can only go to zero (vs. an infinite maximum loss on the upside). Therefore, timing is extremely important.

The best time to short is right before the merge is supposed to happen. This will be when expectations are at their highest, and you will have a short time between entry into the trade and when the merge will or will not happen. If the merge is unsuccessful, the dump will be quick and vicious given the market’s high expectations vs. the objective reality. That will allow you to exit your trade quickly, with profits in hand.

I would suggest using put options for this strategy. Referring back to the futures curve above, the March 2023 futures have the lowest discount. That means that, as a short, you pay the least. That also means the March 2023 put options will be the most attractive. If I were to short, I would buy 1,000 strike March 2023 ETH puts on September 14. You know a-priori your maximum loss, which is the premium paid for the put options. Should the merge go through successfully, this allows you to eliminate unbounded losses. Your downside target is a swift move through your strike below $1,000.

Catharsis

Writing these essays is a great way for me to really think through my trades and ultimately bolster my confidence in the positioning of my portfolio. If I can’t logically explain the thinking behind the construction of my portfolio, then I need to re-examine my trading decisions. During the process of writing past essays, I have altered my portfolio significantly and lost faith in previously held beliefs because I couldn’t defend them well in written prose.

My attempt at applying Soros’ theory of reflexivity to the ETH merge increased my confidence. I questioned what I should do leading into the merge, and after putting these thoughts down on proverbial paper, I know what to do. Buy The Fucking Dip!