Крупнейший эмитент стейблкоинов Tether вновь оказался под пристальным вниманием экспертов. Сооснователь DeFi-студии Pink Brains под ником Ignas провел критический анализ структуры резервов компании.

Так, он усомнился в рациональности долгосрочного хранения стейблкоина. При этом его основная претензия касается дисбаланса рисков и отсутствия выгоды для конечных пользователей.

Зачем вы храните USDT?

Аналитик задался вопросом, почему инвесторы держат USDT вместо USDC.

По его мнению, кроме очевидных причин, таких как торговля на определенных рынках или возможность получить случайный более высокий доход по кредитованию, долгосрочное хранение не имеет смысла. Он считает, что стейблкоин-максимализм нерационален, так как ни USDT, ни USDC не передают доход своим держателям.

«В итоге пользователь принимает на себя 100% риска, но не получает никакой прибыли, кроме временного убежища от волатильности крипторынка. Более того, у держателей USDT нет доли в капитале компании Tether», — отметил он.

По теме: ЕЦБ оценил риски использования стейблкоинов в Европе как минимальные

Растущая доля высокорисковых активов

Новость о понижении рейтинга USDT до «слабого» от S&P вызвала бурные обсуждения, хотя, по мнению аналитика, сообществу не стоило занимать оборонительную позицию.

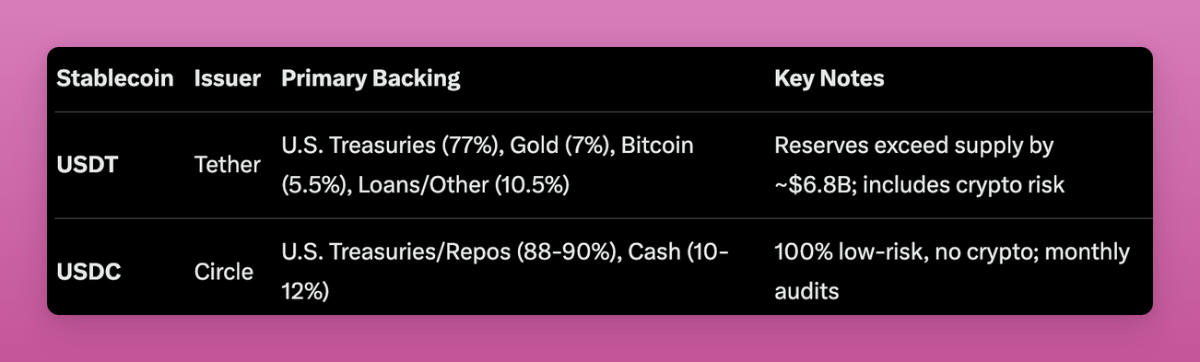

Он отметил, что Tether покупает биткоин (BTC), который составляет 5,5% от обеспечения. Это в свою очередь помогает росту цены самой первой криптовалюты. При этом Circle просто держит казначейские облигации США и эквиваленты наличных средств, согласно Ignas.

«Но если инвестор ищет чистый прокси-трейд, для этого есть Strategy, акции которой растут вместе с биткоином, тогда как USDT не дает никакого потенциала роста», — объяснил он.

Кроме биткоина, Tether также скупает золото, которое сейчас составляет 7% от обеспечения. Эксперт задается вопросом: зачем его покупать вместо большего количества биткоина, если компания не настроена «по-медвежьи» к первой криптовалюте?

«Сейчас около 23% обеспечения USDT — волатильные активы. S&P называет их “высокорисковыми”. Год назад этот показатель был всего 17%», — сказал он.

Ignas иронизирует, что при нынешней динамике Tether ничего не мешает за несколько лет поднять долю волатильных активов до 50%. Компания будет зарабатывать все больше и больше, а держатели USDT по-прежнему не получат от этого никакой выгоды.

По теме: S&P запустил индекс Digital Markets 50 для отслеживания криптовалют и блокчейн-компаний

Кредиты «на стороне»

Еще 10,5% обеспечения — это кредиты третьим аффилированным и неаффилированным организациям, продолжает Ignas. Это могут быть криптотрейдинговые фирмы, майнинговые и другие операции.

Аналитик напомнил, что в 2021 году Tether выдал 1 млрд USDT в кредит Celsius — обеспеченный биткоином — в рамках категории «обеспеченных займов» в резервах. Тогда такие займы составляли 8–10% от резервов стейблкоина.

«Tether не раскрывает личности заемщиков или условия кредитования по соображениям приватности. При этом аудитор только выборочно проверяет сделки, чтобы убедиться, что у займов есть обеспечение и что оно превышает сумму долга», — отметил он.

По теме: Metaplanet заняла еще $130 млн под залог биткоинов для новых покупок

Лучше USDC?

Пользователь под ником Maz напомнил, что проблемы есть и у других стейблкоинов. Так, он напомнил о случаях депега USDC и DAI.

Agnis в свою очередь ответил, что DAI был активом другого типа, и его профиль риска сейчас также высок. А отвязка USDC, по его мнению, также говори о том, что долгосрочное хранение «любого стейблкоина» не стоит сопутствующего риска.

Вместе с тем аналитик отмечает, что его слова — не FUD в отношении Tether, потому что потенциальный крах USDT вызвал бы массовый отток капитала из крипторынка и навредил бы в том числе и его собственному портфелю.

Он резюмировал, что не держит и не планирует держать USDT, но признает, что «Tether молодцы, так они «пампят его биткоин-запасы».

По теме: риски стейблкоинов — что может пойти не так и как защититься

Эта статья не содержит инвестиционных советов или рекомендаций. Каждое инвестиционное и торговое решение связано с риском, читатели должны самостоятельно проводить исследование перед принятием решений.