Мировой поток капитала меняется. На фоне роста регуляторного давления, периодических шоков ликвидности и усиливающейся конкуренции в криптоотрасли крупные компании все чаще делают ставку на физическое золото.

Наблюдения аналитиков The Kobeissi Letter показывают, что такой подход превращается в заметный тренд.

Биткоин против золота: во что выгоднее инвестировать в 2025 году

Tether и новый курс на физическое золото

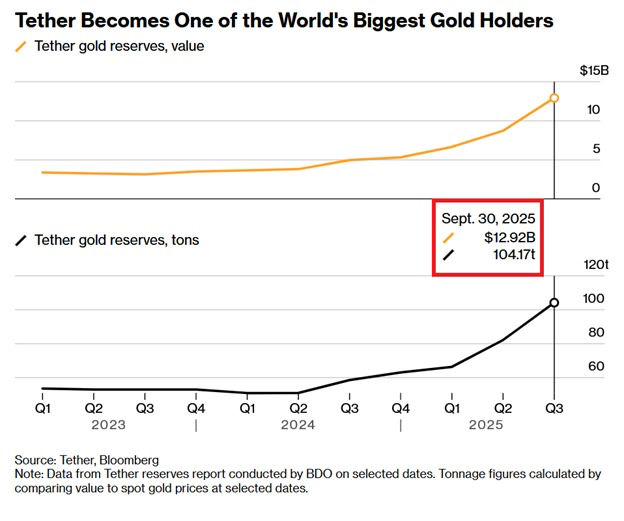

По данным The Kobeissi Letter, в сентябре объем золотых резервов Tether достиг $12,9 миллиарда. Такой показатель соответствует 104 тоннам физического золота. Стоимость золотого портфеля удвоилась с начала года. Физические запасы выросли в два раза по сравнению со вторым кварталом 2024 года.

Средний темп закупок превышает 1 тонну золота в неделю в 2025 году. Такой уровень превращает компанию в одного из крупных покупателей металла на глобальном рынке. Общий объем резервных активов Tether превысил $180 миллиардов. На золото приходится около 7%, и эта доля стала заметной частью структуры активов.

По последней публичной информации, Tether увеличила свои вложения в биткоин еще на 961 BTC. Такая покупка оценивается примерно в $97,34 миллиона. Общий объем биткоинов на балансе компании достиг примерно 87 000 BTC. При текущей цене биткоина в $102 766 такая позиция оценивается примерно в $8,94 миллиарда. Стоимость золотого портфеля остается выше и достигает $12,9 миллиарда. Получается, что физическое золото стало крупнейшим резервным активом компании.

Tether является эмитентом самого популярного стейблкоина в мире. Действия такой компании способны задавать ориентир для всей индустрии и формировать поведение других крупных игроков.

Почему криптокомпании делают ставку на золото

Золото помогает криптокомпаниям снизить риски и укрепить резервы. Металл сохраняет ликвидность в любых условиях и не зависит от резких колебаний криптовалют. Такой актив вписывается в практичный подход к управлению крупными балансами, особенно во времена общей финансовой нестабильности.

При этом внутри индустрии возникает заметная дилемма. Долгое время многие участники сообщества воспринимали биткоин как цифровой аналог золота и уверяли, что он способен заменить традиционные защитные активы. На этом строилась значительная часть идеологии рынка. Покупки физического металла крупнейшими криптокомпаниями выглядят для некоторых как отход от этих убеждений и шаг в сторону более консервативной финансовой модели.

Для самих компаний вопрос стоит иначе. Их задача — создавать устойчивую структуру активов и снижать зависимость от волатильности цифровых инструментов. Золото дает им возможность сбалансировать резервы за пределами крипторынка и подготовиться к любым рыночным сценариям. Такой подход стал элементом долгосрочной стратегии, где на первый план выходит надежность, а не идеология.

Макрообстановка усиливает интерес к золоту

Свежие данные подтверждают, что интерес к золоту остается высоким. 12 ноября фьючерсы на металл открылись на отметке $4 132,20 за унцию, поднявшись на 0,6% по сравнению с предыдущим днем. Цена удерживается выше $4 000 с начала недели. Движение следует за откатом от октябрьских максимумов выше $4 300, но общий рост остается уверенным.

Рынок находится под влиянием смешанных факторов. Продолжительный шатдаун правительства США усиливает интерес к защитным активам, тогда как сильный фондовый рынок поддерживает интерес к риску. Завершение шатдауна восстановит поток данных, необходимых для оценки перспектив ставок. Такие ожидания напрямую влияют на динамику золота. Более низкие ставки исторически поддерживают спрос на металл.

Напомним, ранее редакция BeInCrypto писала о том, что конец шатдауна в США вряд ли станет отправной точкой для нового бычьего ралли биткоина.