原文来自Jarrod Watts

编译|Odaily 星球日报 Golem(@web 3_golem)

预测市场本可以终结“庄家永赚”的时代,但遗憾的是,大多数预测市场仍在为自己牟取利益。

在本文中,我将阐述为什么预测市场目前为何无法服务于用户,以及我为何相信预测市场的下一阶段是通过用户生成市场(user-generated market)实现创作者经济。

我将涵盖的要点包括:

- 探索从负和博弈到接近零和博弈的预测市场的转变;

- 引入创作者经济和收益分享将如何推动预测市场的爆炸式增长;

- 预测市场中的直播机会。

庄家已死

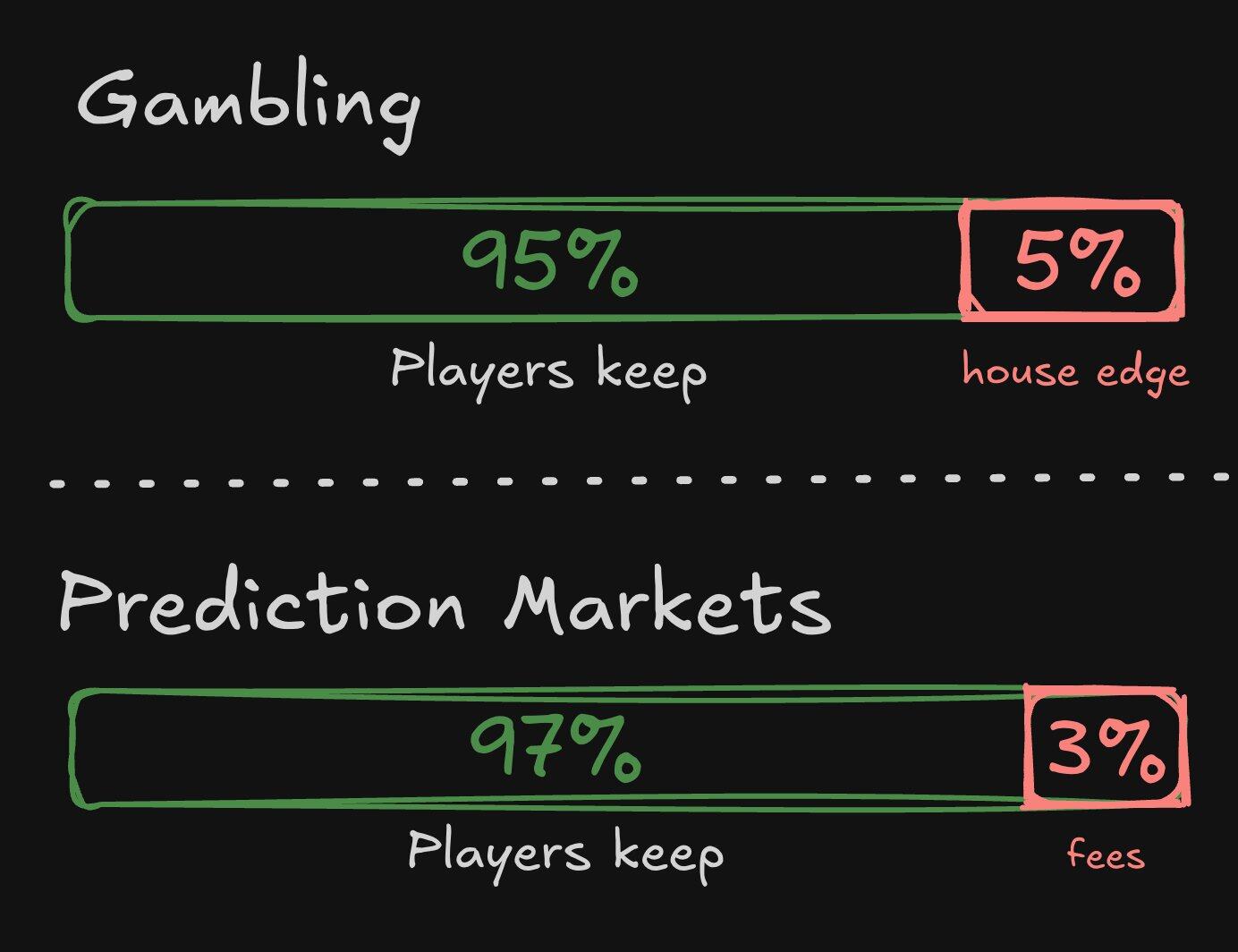

大多数形式的赌博,包括体育博彩,都是负和博弈,玩家输钱给庄家。预期玩家回报率 (RTP) 之和被设置在 100% 以下的不同水平,以系统性地从玩家那里榨取资金。大多数人都明白这一点,但仍然愿意赌博,用金钱换取我们从预期中获得的多巴胺。

预测市场可以消除庄家来改变这种现状,通过允许玩家在开放市场中互相 PvP。预测市场是零和博弈,赢家从输家那里拿钱,与交易类似。

这在客观上比传统的赌博/体育博彩要好,虽然你的道德准则可能不认同,但这些产品显然有着巨大的市场需求——公平存在总比榨取利润更好。

但是当预测市场开始收取费用时,这种说法就站不住脚了。大多数平台(Polymarket 除外)通常会从玩家的入场金额或预期利润中抽取 2-3% 左右。

预测市场费用使其从零和博弈变成了负和博弈

预测市场收取费用的结果是,它们重新引入了赌博中的负和博弈,这意味着玩家会随着时间的推移向赌场/平台流失资金。

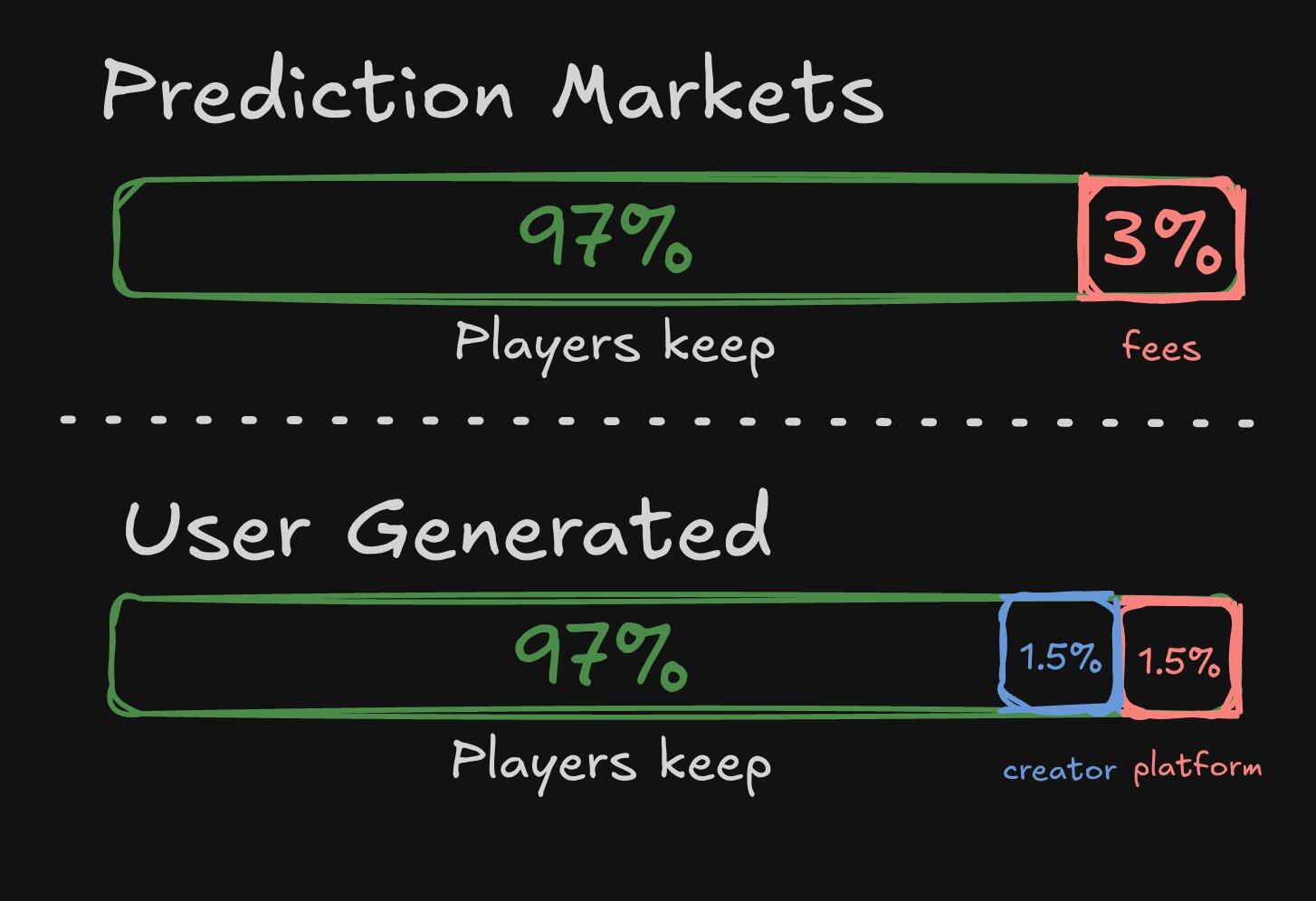

然而,我相信有一种强有力的替代方法可以利用这些费用,从而提高用户的参与度,即创建用户生成市场。

预测市场作为创作者经济载体

我认为预测市场应该:

- 允许用户无需许可即可创建市场;

- 引入收益分成机制,允许市场创作者赚取一定比例的佣金。

引入市场创作者收益分成机制

这样做可以将用户转变为共同创作者,他们可以创造新的市场(以及围绕这些市场的UGC),从而推动平台的增长,而无需团队直接承担制作成本。Roblox 和 Fortnite 就是实施此模式的典型案例——它们都将部分收入用于支付社区地图创作者的报酬。

在预测市场中,创作者可以创建与其社区/利基市场相关的市场,为用户提供新的参与方式,并从中赚取收益。因为预测市场的应用场景几乎无限,也就意味着可以适用于无数的创作者。

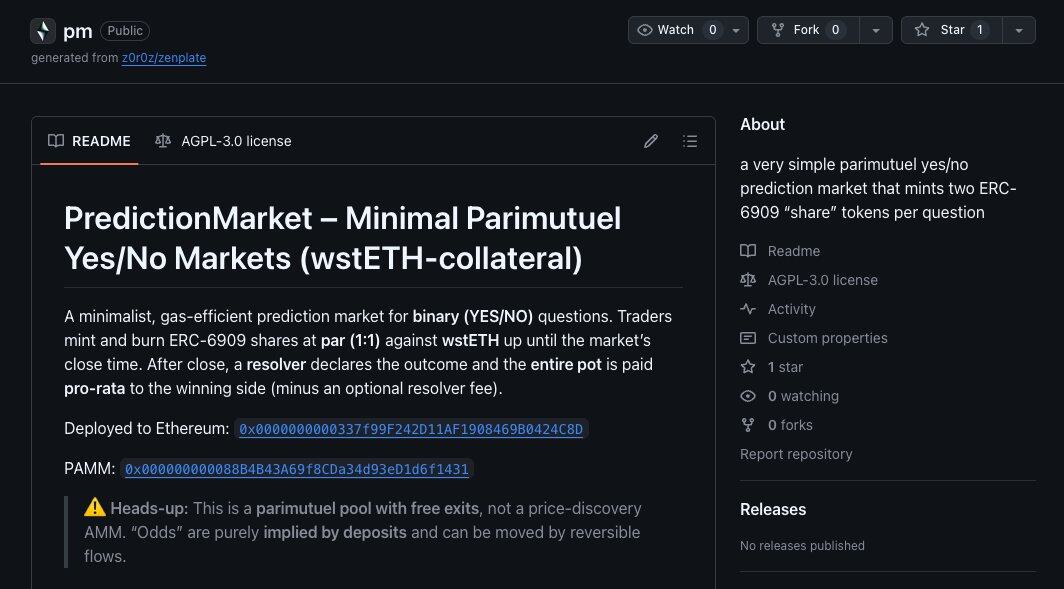

虽然存在技术限制,但在我撰写本文的研究过程中,我发现了一个 GitHub 代码库,其中包含用于创建用户生成预测市场的智能合约。它还包含一个 AMM 变体,以解决用户生成市场带来的一些流动性问题。

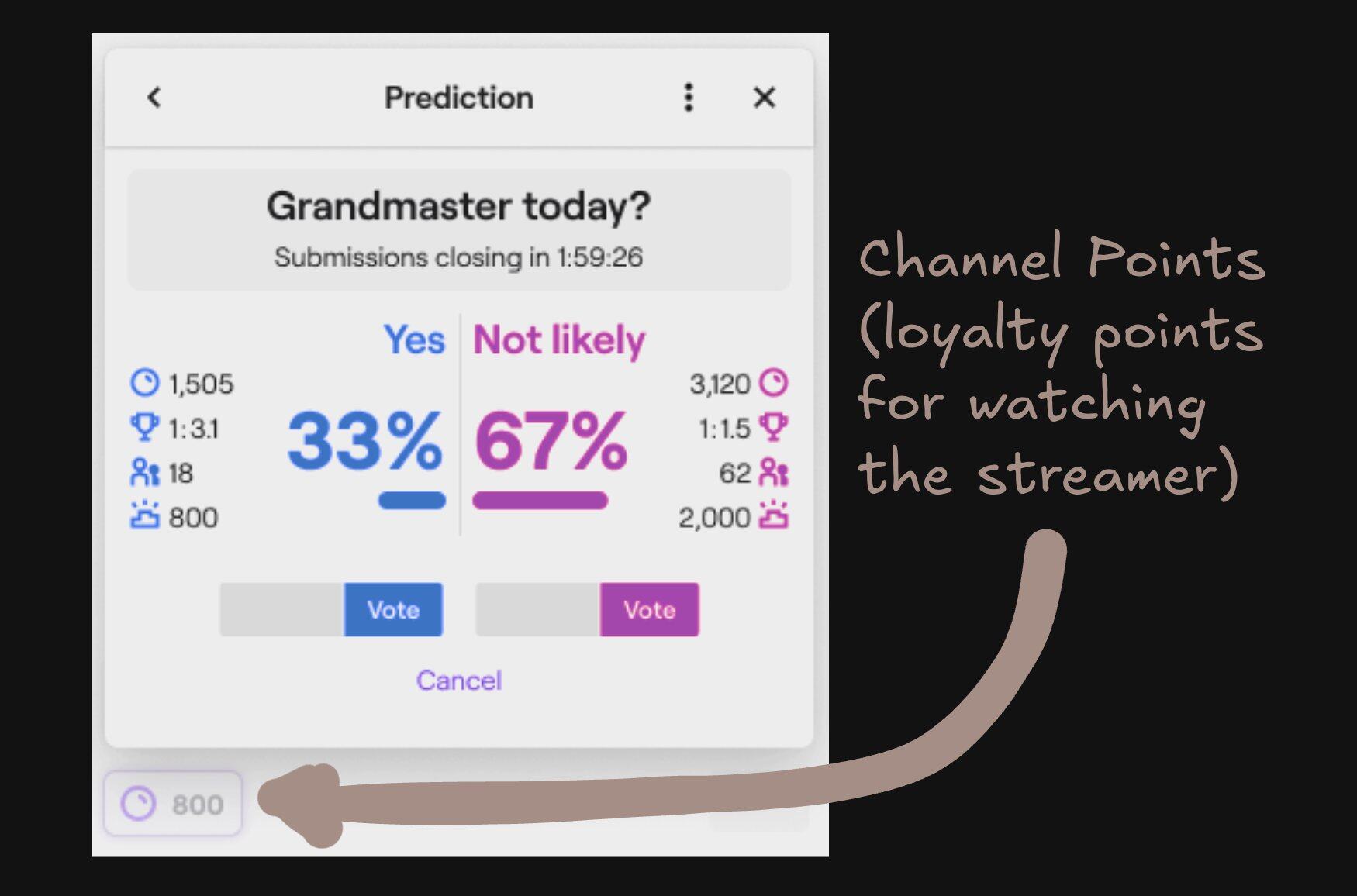

主播生成预测市场

用户生成预测市场自然会发展为主播为其观众创建的实时、快速市场。在这些预测市场中,主播可以发起投票,观众可以参与并实时观看结果。

这使得创作者可以创建短期预测市场,观众可以投票支持“我会赢得这场比赛吗?”之类的问题。Twitch 已经实现了此功能,但它使用的是其原生频道积分,而不是 USDC。

Twitch 直播预测市场示例

这类激活方式是双赢的——主播通过收益分成获得报酬,而观众则更加投入于直播。我认为这对未来的主播和内容创作者来说都是一个巨大的机遇。

结语

预测市场已经取得了令人难以置信的成功,但用户生成预测市场的规模化仍是一个巨大的机遇(也可能存在技术挑战)。用户成为大使并创作直接宣传预测市场平台的内容所带来的后续效应是显而易见的,让我们期待有此理念的产品诞生落地。