作者:Alana Levin

编译:深潮TechFlow

关于本轮加密周期中是否会迎来“山寨币季”(Alt Season),人们提出了许多疑问。一些人将目光投向 2024 年 1 月或 2025 年,期待非比特币类加密资产(山寨币)大幅升值,甚至创下历史新高。

在过去的周期中,比特币价格的显著上涨通常会引发许多长尾加密资产的类似表现,甚至有时这些资产的涨幅会超过比特币。然而,在过去几年里,这种模式似乎并未重现。当前,比特币的市场占比已达到 58%,自 2022 年 11 月以来一直呈稳步上升趋势。

那么,这一周期是否会跳过“山寨币季”?抑或是“山寨币季”尚未到来?又或者……“山寨币季”其实已经在一个完全不同的市场中悄然上演,而我们却没有察觉?

我的直觉是最后一种情况。真正的“山寨币季”正在加密股票市场上演。

什么是“山寨币季”的典型特征?

-

价格上涨吸引新资本→问题是,新资本从哪里来?

-

价格上涨导致利润轮换→问题是,谁在获利以及利润被重新部署到哪里?

如今,确实有新资本希望进入加密领域,但这些资金更多来自机构投资者,而非散户。相比之下,散户往往是快速的早期采纳者,而机构投资者则更为谨慎,通常需要外部的合法性认证作为推动力。而这种合法性认证正在发生:2024年,美国证券交易委员会(SEC)批准了比特币和以太坊现货交易所交易基金(Spot ETFs);SEC主席阿特金(Atkin)最近宣布了“加密项目”(Project Crypto);纳斯达克首席执行官阿德娜·弗里德曼(Adena Friedman)也公开支持股权的代币化(Tokenization of Equities)。类似的例子不胜枚举。

机构投资者带着新鲜资本涌入,而我猜测,这些资本大多被导向了加密股票,而非加密资产。股票市场对机构来说更熟悉且更容易接触。机构投资者已经拥有完善的运营体系(包括托管、合规流程、交易商关系等),而直接购买加密资产则可能需要全新的能力建设。而且,购买股票属于他们的职责范围——而直接购买加密代币(尤其是长尾资产)可能超出了其职责范围。

因此,机构正在将资金投入加密股票或与加密相关的股票中。例如:

-

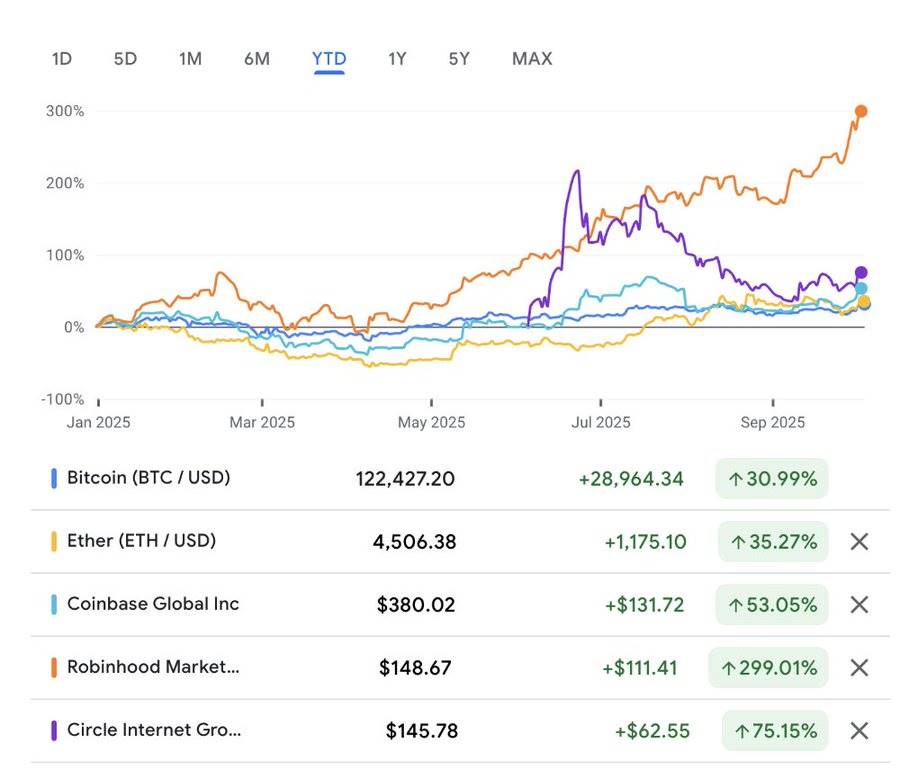

Coinbase 年初至今上涨 53%;

-

Robinhood 上涨 299%;

-

Galaxy 上涨 100%;

-

Circle 自 6 月 IPO 以来上涨 368%(若以首个交易日收盘价计算,则上涨了 75%)。

相比之下,比特币上涨 31%,以太坊上涨 35%,Solana 上涨 21%。加密股票的表现显然更为抢眼。

如果我们从比特币在 2022 年 12 月 17 日触底以来的表现来看,情况类似。

有理由相信这一趋势将继续。未来将有一系列加密股票 IPO 计划推出,更多处于后期阶段的公司可能在未来几年提交上市申请。

与典型的“山寨币季”一样,并非所有资产都会表现良好。我预计会有一定的资金轮动,例如交易者可能会从估值过高的资产(如 CRCL 当前的市销率为 26 倍)中获利了结,并将资金重新部署到其他资产中。

在加密市场中,我们经常看到不同的热点轮动,例如市场可能从DeFi资产转向游戏代币,再到AI相关代币。加密股票市场可能也会类似,一个“山寨币季”可能会看到资金从稳定币相关股票转向交易所股票,再到数字资产储备公司(或其他趋势)。

我认为,加密货币股票山寨币季最终可能看起来更像一个历史性的山寨币季,而不是加密原生市场中未来的任何山寨币季,原因有很多:

-

资产集中度。目前只有少数几家股票提供加密货币投资。这与以往加密货币周期的情况类似,当时买家认为有吸引力的代币可能不足 100 种。值得注意的是,这与如今的加密货币原生市场截然不同——后者拥有数百万种代币,因此部署分布更加分散。

-

杠杆利用。上一个周期中,许多加密原生的借贷平台相继倒闭,我们尚未看到它们的重建。然而,股票投资者可以使用杠杆,这意味着市场的繁荣可能更为显著(但崩盘也可能更加剧烈)。

我们或许会在未来迎来加密原生资产的“山寨币季”。但这需要时间,新的边际资本来源需要逐步建立起能够支持其投资加密资产的运营能力。

因此,就目前而言,这可能不是许多人期待的山寨币季——但无论如何,我们正处于山寨币季。