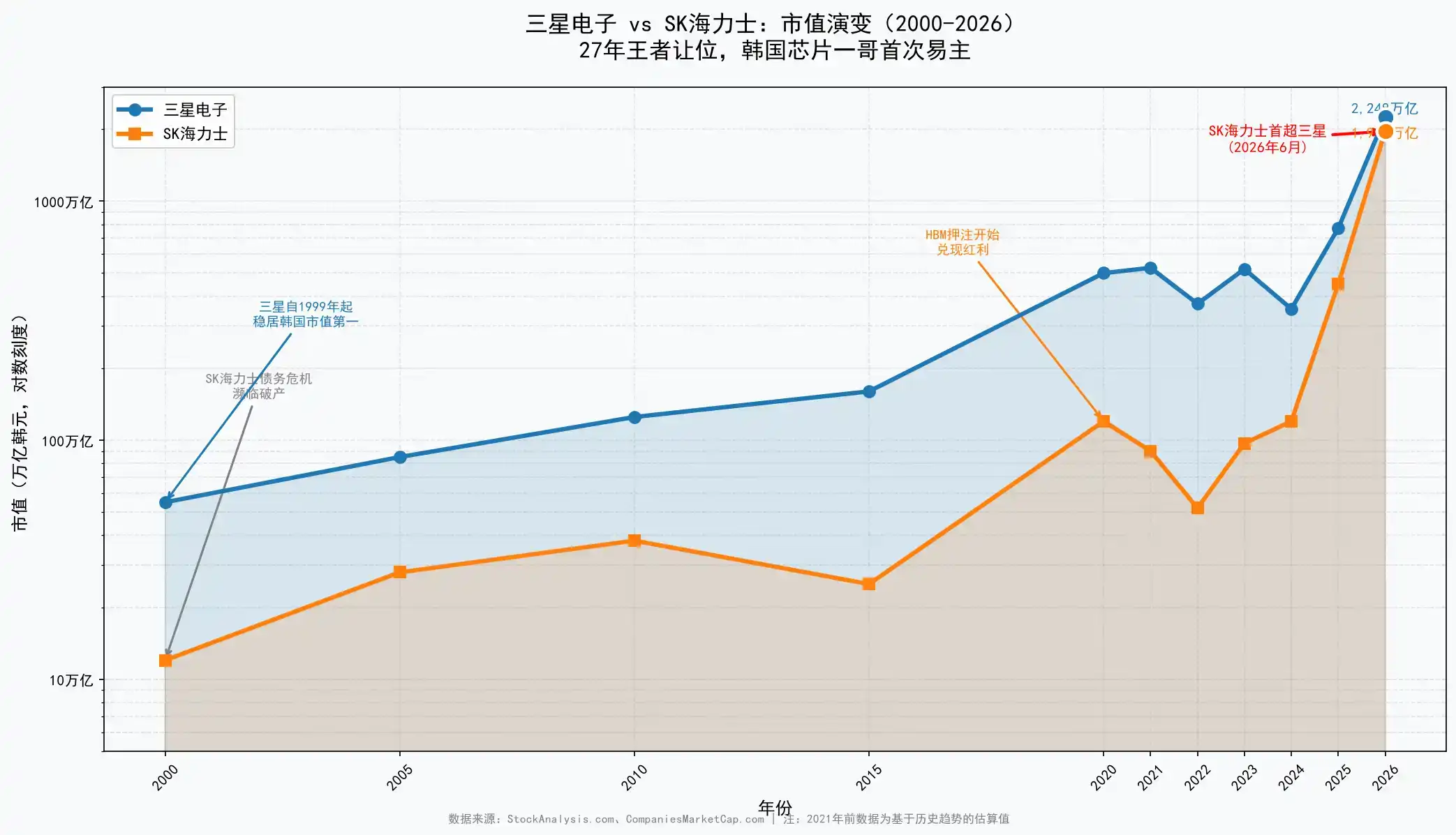

On June 22, 2026, SK Hynix, once burdened with $14 billion in debt and teetering on the brink of bankruptcy, saw its market capitalization surpass that of Samsung Electronics, which had dominated the Korean capital market for 27 years, to become South Korea's most valuable listed company. Behind this lies a precise, historic gamble—as the AI wave propelled High Bandwidth Memory (HBM) from a niche product to the core of computing power, SK Hynix, with a 59% market share and staggering daily net profits exceeding 2 billion yuan, completed the most dramatic comeback in business history.

The moment that rewrote the history of South Korea's capital market occurred during the trading session on June 22, 2026.

SK Hynix's total market capitalization exceeded that of Samsung Electronics for the first time, making it South Korea's highest-valued listed company. This marked the first time since 1999 that Samsung Electronics relinquished its title as South Korea's "market cap leader." At the intraday peak, SK Hynix's market cap reached 2,080 trillion won (approximately $1.35 trillion), while Samsung Electronics reported a market cap of 2,066 trillion won.

From a debt-ridden enterprise on the verge of collapse to a trillion-dollar empire surpassing the national symbol Samsung Electronics, SK Hynix accomplished one of the most astonishing comebacks in business history over two decades. This is not merely an exchange of rankings between two companies but also a microcosm of how the AI wave is reshaping the global semiconductor industry's power structure.

HBM: From Niche Product to Core Infrastructure of the AI Era

SK Hynix's comeback is essentially a history of "betting right on HBM."

High Bandwidth Memory (HBM) was once a niche category within memory chips. However, in the training of large AI models, GPUs require extremely high-speed data throughput with memory—an NVIDIA H100 requires 80GB of HBM, the H200 requires 141GB, and the latest B200 requires 192GB. Globally, only three companies can produce HBM: SK Hynix, Samsung, and Micron.

SK Hynix has established a near-monopoly advantage in this segment. According to TrendForce data, SK Hynix held a 59% share of the global HBM market in 2025. More critically, in the most lucrative HBM4 segment, Counterpoint Research predicts SK Hynix's market share will reach 54% in 2026 and has already secured over two-thirds of the HBM4 orders for NVIDIA's next-generation Vera Rubin platform, with some institutions predicting the share could exceed 70%.

This advantage is directly reflected in financial data. In the first quarter of 2026, SK Hynix's consolidated revenue reached 52.58 trillion won, a year-on-year increase of 198.1%, breaking the 50 trillion won mark for the first time; net profit reached 40.35 trillion won, nearly quadrupling year-on-year. A simple calculation shows that SK Hynix earned an average net profit of over 2 billion yuan per day in the first three months of this year.

An operating profit margin of 72% not only exceeded NVIDIA's but also far surpassed that of traditional DRAM business. According to Counterpoint Research estimates, the operating profit margin of SK Hynix's HBM business ranges between 75% and 83%, about 10 percentage points higher than its ordinary DRAM business. The HBM business now accounts for approximately 40% of the company's revenue, becoming a veritable profit engine.

Samsung's Dilemma: The Cost of Being Broad

Compared to SK Hynix's sharp focus, Samsung Electronics' problem lies in its "breadth" becoming a burden.

Samsung's business spans memory chips, smartphones, semiconductor foundry, home appliances, and more. Its 2025 revenue scale of 333.6 trillion won far exceeds that of SK Hynix, but the drag from non-memory businesses disperses resources and strategic focus.

In the memory chip sector, Samsung's layout in HBM is noticeably lagging. Although Samsung is also advancing the development of HBM3E and HBM4, it trails behind SK Hynix in customer certification and mass production progress. This has resulted in Samsung watching its competitor exclusively enjoy the premium during the period of most explosive AI computing demand.

What troubles Samsung even more is the simultaneous slowdown of its other businesses. The smartphone business's market share has declined from 54% to 45%; the semiconductor foundry business, due to technological gaps, has failed to secure orders from high-end customers, facing underutilization issues. The profits that the memory business should provide are continuously diluted by losses from other segments.

Furthermore, ongoing labor-management disputes between management and employees are intensifying. Following SK Hynix's milestone bonus agreement last year, Samsung's labor conflicts pose additional challenges to its profit recovery. While SK Hynix employees reap rich rewards from the AI红利, Samsung's organizational cohesion is being tested.

From $14 Billion in Debt to a Trillion-Dollar Empire

The story of SK Hynix's rise is almost a microcosm of the South Korean semiconductor industry.

Its origins can be traced back to Hyundai Electronics, founded in 1983. Relying on government support and chaebol capital injections, Hyundai Electronics rapidly caught up, focusing on DRAM chips, and grew into South Korea's second-largest semiconductor company by the 1990s. In 1999, Hyundai Electronics merged with LG Semiconductor to form Hynix, under the Hyundai Group.

However, the semiconductor downturn in the early 2000s almost pushed the company into bankruptcy. At that time, SK Hynix was saddled with $14 billion in debt and teetered on the brink of collapse. The South Korean government promoted industry consolidation, leading to a duopoly in the DRAM sector with Samsung and Hynix. Subsequently, through several key restructurings and counter-cyclical technological investments, Hynix gradually recovered.

The real turning point was the early bet on HBM. When the market still viewed HBM as a niche product, SK Hynix had already identified it as the future direction for high-performance computing. This strategic vision yielded超额回报 in the AI wave—today, HBM has transformed from a common commodity into a key infrastructure component supporting ChatGPT and advanced AI models.

SK Hynix's comeback has also altered the ecology of South Korea's capital market. The head of South Korea's Financial Supervisory Service recently expressed "regret over not preventing the launch of single-stock leveraged ETFs" and stated that the negative impact of high-risk products related to Samsung and SK Hynix has significantly increased. Retail investor demand for leveraged ETFs of these two stocks remains high, and regulators are considering separate stabilization measures.

Beyond Market Cap: Deep Restructuring of South Korea's Economic Landscape

The significance of SK Hynix's market cap surpassing Samsung extends far beyond a capital market ranking.

Bank of Korea Governor Shin Hyun-song recently stated explicitly that the benefits brought by the expansion of the semiconductor industry are increasingly being transmitted to the overall economy through corporate profits, consumption, and investment improvements. As companies like SK Hynix become new engines for the national economy, South Korea's growth model is shifting from being traditionally driven by consumer electronics to being driven by AI infrastructure.

From a global perspective, this event marks the transformation of the memory chip industry from "commoditization" to "high-value specialization." Traditional DRAM and NAND are highly cyclical commodities with volatile prices. However, HBM, deeply tied to AI computing power, is shedding its commodity attributes and becoming a high-end product with long-term pricing power.

Under the Cycle, No King Reigns Forever

However, SK Hynix's ascension does not mean it can rest easy.

Around 2028, new capacities from Micron's New York fab, SK Hynix's Yongin complex, and Samsung's Pyeongtaek expansion are expected to be released concurrently. TrendForce predicts that memory chip price increases will last at least until the end of 2027, but the landing of new capacity could alter the supply-demand balance. At that point, whether the scarcity premium of HBM will shrink will test the depth of SK Hynix's moat.

Furthermore, Samsung is unlikely to surrender its throne willingly. Samsung still possesses deep accumulation in 3D NAND and advanced process technologies. Once it achieves a breakthrough in HBM4, market competition will intensify rapidly. Today, the market cap difference is only about 14 trillion won, and the suspense over the change of the crown is far from over.

But on this day, June 22, 2026, SK Hynix indeed rewrote history. A company reborn from a debt crisis, through a precise bet on the core infrastructure of the AI era, surpassed the behemoth that had ruled South Korea's capital market for 27 years. This is not the终点, but the latest footnote in the ongoing reshuffle of power within the global semiconductor industry.