一、项目背景及介绍

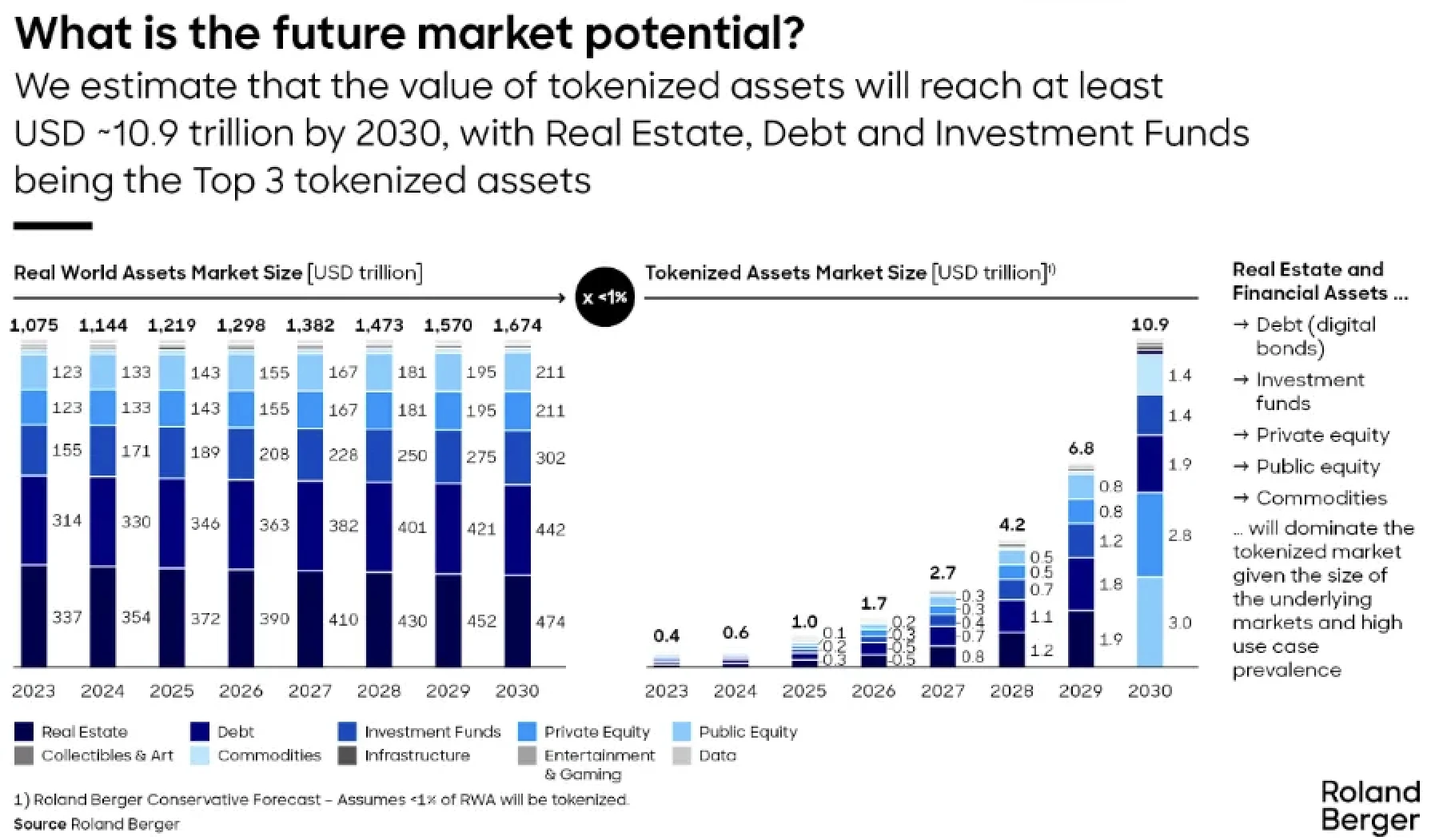

BlackRock 的 CEO Larry Fink 认为代币化是金融的未来和市场的下一步演变,他的这一立场可能会影响其他主要金融游戏参与者的态度。正如我们在之前关于 Dusk Network 的研究中所强调的,Real World Assets(RWA,真实世界资产)正在成为加密货币行业中的重要资产类别。截至 2024 年 5 月,RWA 市场已超过 66 亿美元,反映了投资者对这一创新金融产品的日益兴趣。将 RWA 代币化并将其引入区块链可以在 DeFi(去中心化金融)中提供收益机会。资产代币化市场预计到 2030 年将达到 10 万亿美元。

Source: Roland Berge

这个新兴市场的主要吸引力不仅仅是为 DeFi 提供收益机会。通过将资产数字化为代币,它实现了资产的碎片化——将国债、股票和房地产等资产分割为较小的份额。这一过程增强了流动性,并为拥有不同资本水平的投资者打开了投资机会的大门。

Chainlink 用下面的插图解释了资产代币化的运作方式。它的主要优点包括通过可互操作的代币化资产增加流动性和提高可访问性,使小额投资者能够以相对较低的资本投资高收益资产。此外,由于许多区块链的公共性质,它提高了透明度,并通过将真实世界资产的价值连接到 DeFi 生态系统中,增强了组合性。

Source: Chainlink

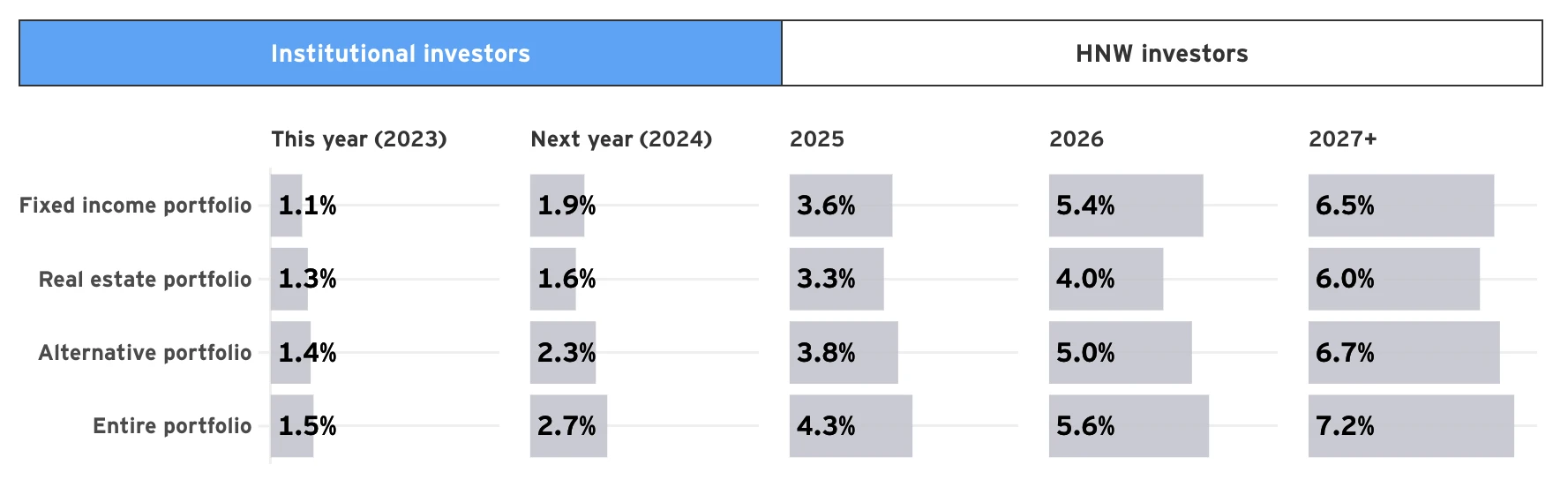

美国代币化政府债券的市值也从 2023 年的 1.14 亿美元增长到 8.45 亿美元,Franklin Templeton(富兰克林邓普顿)是这一资产类别的最大发行者,占市场的约 38% 。安永(EY)的最新研究表明, 64% 的高净值投资者和 33% 的机构投资者计划在 2024 年底前增加对代币化国债的投资。

虽然仍处于起步阶段,但资产代币化代表了区块链技术最有前景和潜力的应用之一。Ondo Finance(Ondo 金融)凭借其国债代币化服务,处于这一趋势的有利位置,投资者兴趣持续增长。

二、技术架构

Ondo 正在通过其去中心化协议改造金融,利用区块链提供机构级产品。通过将传统金融中的稳定资产代币化,Ondo 将可靠性与区块链的效率相结合。Ondo 有两个主要部门:资产管理和技术。资产管理部门创建并监督代币化金融产品,而技术部门则开发支持这些产品的协议。

目前,Ondo Finance 提供两种不同的投资选择:

(1)USDY(Ondo US Dollar Yield Token)

由短期美国国债和银行存款支持的代币化票据。

提供 5.30% 的年化收益率(APY),总锁仓量(TVL)为 3.1535 亿美元。

比传统的稳定币(如 USDT/USDC)更安全、更透明。

由 Ankura 信托公司管理,以确保合规性和投资者保护。

Source: Ondo Finance

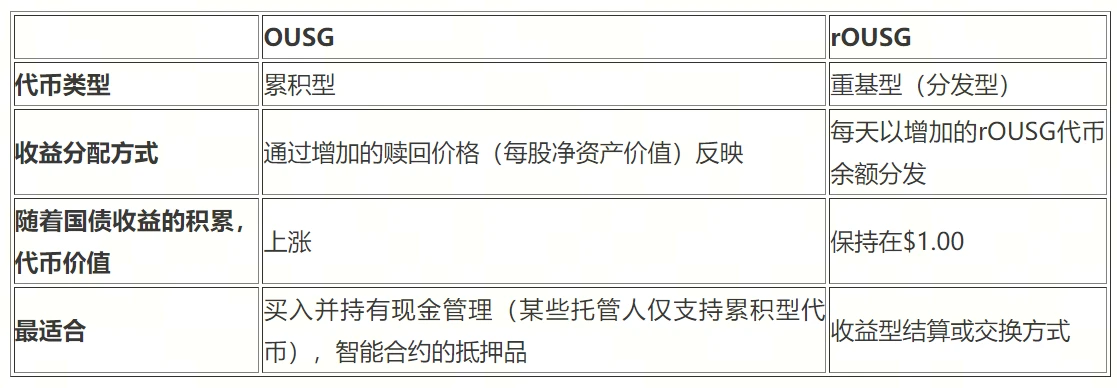

(2)OUSG(Ondo 短期美国国债)

为被动投资者提供低风险的代币化短期美国国债。

提供 4.81% 的年化收益率(APY),总锁仓量(TVL)为 2.2132 亿美元。

2024 年 3 月将投资从 BlackRock 的 SHV 转移到 BUIDL。

Ondo 最近推出了新版的 OUSG,名为 rOUSG,为投资者通过额外的 rOUSG 代币提供收益。

Source: Ondo Finance

三、产品及发展路线

Ondo Finance 旨在通过公共区块链技术连接传统金融和去中心化金融。他们的重点是创建安全、透明和合规的金融产品。

OUSG:代币化 BlackRock 短期美国国债 ETF。

OMMF:代币化 BlackRock 货币市场基金。

USDY:收益稳定币的替代品。

Flux Finance:支持代币化证券作为抵押品的协议。

在下一阶段,他们旨在代币化公开交易的证券,解决与流动性和基础设施相关的挑战。最终,Ondo 希望通过将区块链的优势扩展到更广泛的金融服务领域,在传统金融中创新,使用集中和去中心化机制的结合。这种方法将有助于将区块链技术的优势带到更广泛的金融操作中。

这些产品推动了显著增长,Ondo 的 TVL 从 4000 万美元增加到 5.34 亿美元。展望未来,Ondo 计划通过增加 USDY、OUSG 和 OMMF 的采用和流动性,扩展其代币化现金等价物的使用。这将涉及建立合作伙伴关系和开发跨链工具以促进这些过程。

由 Ondo Finance 团队创建的 Flux Finance 是去中心化借贷的一个重要进展。它基于 Compound V2,但增加了新功能。它支持 USDC 等开放代币和 OUSG(Ondo Short-Term US Government Bond Fund)等受限制代币。这意味着您可以自由借出 USDC,但使用 OUSG 作为抵押借款需要满足特定的许可要求,以确保合规性和安全性。Flux 使用类似于 Compound 的点对池(p2p ool)模式,允许用户以超额抵押的方式进行借贷。贷方可以赚取他们提供的稳定币的利息,而借款人可以使用他们的抵押品借入稳定币,并遵循资产的许可要求。Flux Finance 由 Ondo DAO 治理。

四、竞品情况

鉴于 Ondo 与像 BlackRock 这样的巨头建立了关系,Ondo 在加密 RWA 类别中似乎正在传统金融中崭露头角,补充其他 TradFi 公司。在去中心化金融领域,竞争正在加剧。Centrifuge 专注于代币化结构性信贷并使用 NFT 发行债务。Ethena 提供合成资产敞口,使用户能够在不持有资产的情况下进行交易。Maple Finance 向机构提供低抵押贷款,强调信用评估和放贷。Pendle 处理代币化收益交易,使用户能够分离和交易资产的收益部分。

Ondo Finance 脱颖而出有几个原因。它通过将传统金融与区块链整合,瞄准庞大的美国国债市场,具有广泛的市场覆盖率。其互补方法涉及与 BlackRock 等传统金融巨头合作,从而避免直接竞争。此外,Ondo 提供创新产品,如 USDY 和 OUSG,提供比传统稳定币更安全、更透明的替代方案。

五、代币经济

(1)ONDO 代币经济学摘要

市值排名:#54

全面稀释估值(FDV):$ 131.5 B,排名#16

流通供应量: 14.4 亿 ONDO(总供应量的 14.27% )

总供应量: 100 亿 ONDO

最大供应量: 100 亿 ONDO

下一次解锁: 167 万 ONDO(约$ 219 万), 5 天后

(2)代币分配

Source: Dropstab

(3)即将解锁事 I 件

2024 年 6 月 18 日: 167 万 ONDO(约$ 219 万)

2024 年 7 月 18 日: 167 万 ONDO(约$ 219 万)

2024 年 8 月 18 日: 167 万 ONDO(约$ 219 万)

2024 年 9 月 18 日: 167 万 ONDO(约$ 219 万)

2024 年 10 月 18 日: 167 万 ONDO(约$ 219 万)

2024 年 11 月 18 日: 167 万 ONDO(约$ 219 万)

2024 年 12 月 18 日: 167 万 ONDO(约$ 219 万)

2025 年 1 月 18 日: 19.4 亿 ONDO(约$ 25.5 B)

2026 年 1 月 18 日: 19.4 亿 ONDO(约$ 25.5 B)

2027 年 1 月 18 日: 19.4 亿 ONDO(约$ 25.5 B)

2028 年 1 月 18 日: 19.4 亿 ONDO(约$ 25.5 B)

(4)代币用途

ONDO 代币是 Ondo Finance 及其 Flux Finance 协议的治理代币。持有者有权对 Ondo DAO 内的各种提案进行投票,确保所有决策透明地在链上进行。要发起提案,个人必须持有或被委托至少 1 亿 ONDO 的投票权。目前尚不清楚未来是否会为 ONDO 持有者引入其他用途。

六、团队、融资历史与生态系统

Ondo Finance 团队拥有来自传统金融和Web3领域的多元化人员组合。创始人兼首席执行官 Nathan Allman 和总裁兼首席运营官 Justin Schmidt 均来自高盛。另一位重要成员 Katie Wheeler 则来自 BlackRock。此外,团队还包括来自 OpenSea、MakerDAO 和 Boson Protocol 的开发人员。这种专业知识的结合与 Ondo Finance 的独特愿景和目标高度一致。

Source: Ondo Finance

种子轮:在 2021 年 12 月,Ondo Finance 以每代币$ 0.013 的价格筹集了$ 400 万,实现了 99.87 倍的投资回报(ROI)。共售出 3 亿代币(总供应量的 3% ),由 Pantera Capital 领投,设有 1 年初始锁定期,随后为 24 个月释放期。

公募轮: 2022 年 5 月 12 日,以每代币$ 0.03 的价格筹集了$ 1000 万,实现了 43.28 倍的投资回报(ROI)。共售出 1 亿代币(总供应量的 1% ),在 Coinlist 上进行,设有 1 年锁定期,随后为 18 个月释放期。

A 轮融资: 2022 年 4 月,以每代币$ 0.02 的价格筹集了$ 2000 万,实现了 64.92 倍的投资回报(ROI)。共售出 10 亿代币(总供应量的 10% ),由 Founders Fund 领投,设有 1 年初始锁定期,随后为 24 个月释放期。

Ondo Finance 已经形成了若干关键合作伙伴关系,以加强其区块链和金融服务:

Aptos Foundation:这次合作将显示世界资产与区块链技术的整合,从代币化美国国债产品 USDY 开始。

Thala Labs:合作推出 USDY 在 Thala 的 AMM 池中使用,并将其作为抵押债务头寸(CDP)的抵押品,增强流动性和 DeFi 解决方案。

Wintermute:合作以提高美元收益稳定币 USDY 的流动性,提供跨多个区块链平台的全天候流动性。

BlackRock:通过对 BlackRock 的 BUIDL 基金进行 9500 万美元的投资,展示了扩展代币化努力和与 Ondo 产品整合的承诺。

七、总结

Ondo Finance 脱颖而出有几个原因。它通过将传统金融与区块链整合,瞄准庞大的美国国债市场,具有广泛的市场覆盖率。其互补方法涉及与 BlackRock 等传统金融巨头合作,从而避免直接竞争。此外,Ondo 提供创新产品,如 USDY 和 OUSG,提供比传统稳定币更安全、更透明的替代方案。

利好因素:

代币化行业将迎来显著增长,Ondo Finance 与 BlackRock 的合作,战略性地定位于将数万亿美元引入Web3。

Ondo Finance 的 TVL 自 2024 年初以来实现了大幅增长。 真实世界资产在加密领域代表着一个新鲜而有前景的叙事,具有强大的早期采用潜力。

Ondo Finance 致力于发展其产品,以满足客户需求。

大多数 OUSG 的投资最初是在 BlackRock 的 iShares Short Treasury Bond ETF(SHV)中。2024 年 3 月,他们转向 BlackRock 的 USD Institutional Digital Liquidity Fund(BUIDL),与 Ondo 的资产代币化重点一致。

Ondo Finance 是加密 RWA 领域的领先者,成为首选。

Ondo Finance 持有 BUIDL 当前供应量的约 38% 。

利空因素:

ONDO 代币的用途显示出显著的集中化风险。

尽管所有持有者都可以参与治理,但最大的持有者拥有最大的影响力。

大约 85% 的总 ONDO 供应量由 Ondo Finance 团队控制。

在 TradFi 和加密货币的交汇处运营,Ondo Finance 进入了一个相对未开发的市场,监管构成了重大挑战。

不良债务是包括 Ondo Finance 的 Flux 在内的 DeFi 协议的主要风险。当借款人的抵押品价值低于其债务时,就会发生不良债务。如果借款人的权益变为负数,Flux 将使用其储备金来缓解损失。为了尽量减少波动性并降低不良债务风险,Flux 仅接受稳定资产作为抵押品。