原创 | Odaily星球日报

作者 | 南枳

曾在 22 年倍受争议的 Pixelmon,在本月初宣布了 800 万美元的融资后,又与 MON Protocol 携手推出代币 MON,并宣布将于本月底进行代币公售。

Odaily星球日报将于本文梳理这款曾经创下 7000 万美元 NFT 销售额记录的链游的相关信息,解析其愿景以及代币发售流程。

Pixelmon 解析

市场机会在哪?

Pixelmon 表示,NFT 技术近年来得到了广泛采用,最初由数字艺术家和收藏家推动,他们发现 NFT 是消除中间商、安全转移特有图片或底层 IP 所有权、从二级市场赚取版税的完美手段;相信游戏将迅速成为第一个受益并推动区块链和 NFT 技术大规模采用的消费市场。

在市场首次尝试通过区块链去中心化游戏资产所有权时,使用了 NFT 作为游戏付费渠道,将赚钱嵌入到游戏中,从而将 NFT 价格合理化为一种付费玩游戏和赚钱的关系(即 Play to Earn)。这种策略的问题在于:

无人关注创造高质量游戏产品和体验迭代;

底层业务目标针对的是 NFT 购买者而不是游戏玩家;

不可持续的经济体系,新的购买者在没有真正的“消费者”(玩家)的情况下维持了旧的经济体系。

简而言之,Pixelmon 认为目前的链游更多是一种庞氏经济体,难以通过可持续性收入长期生存。

Pixelmon 想如何破局?

Pixelmon 表示,其目的是创建一个去中心化游戏 IP 所有权系统,为 Play to Own 提供正确的激励,建立基于免费游戏的收入模式。而其中的关键在于区分用户,将“艺术品和商业 IP 收藏家”与“游戏用户”区分开来,建立一套互促的生态系统。

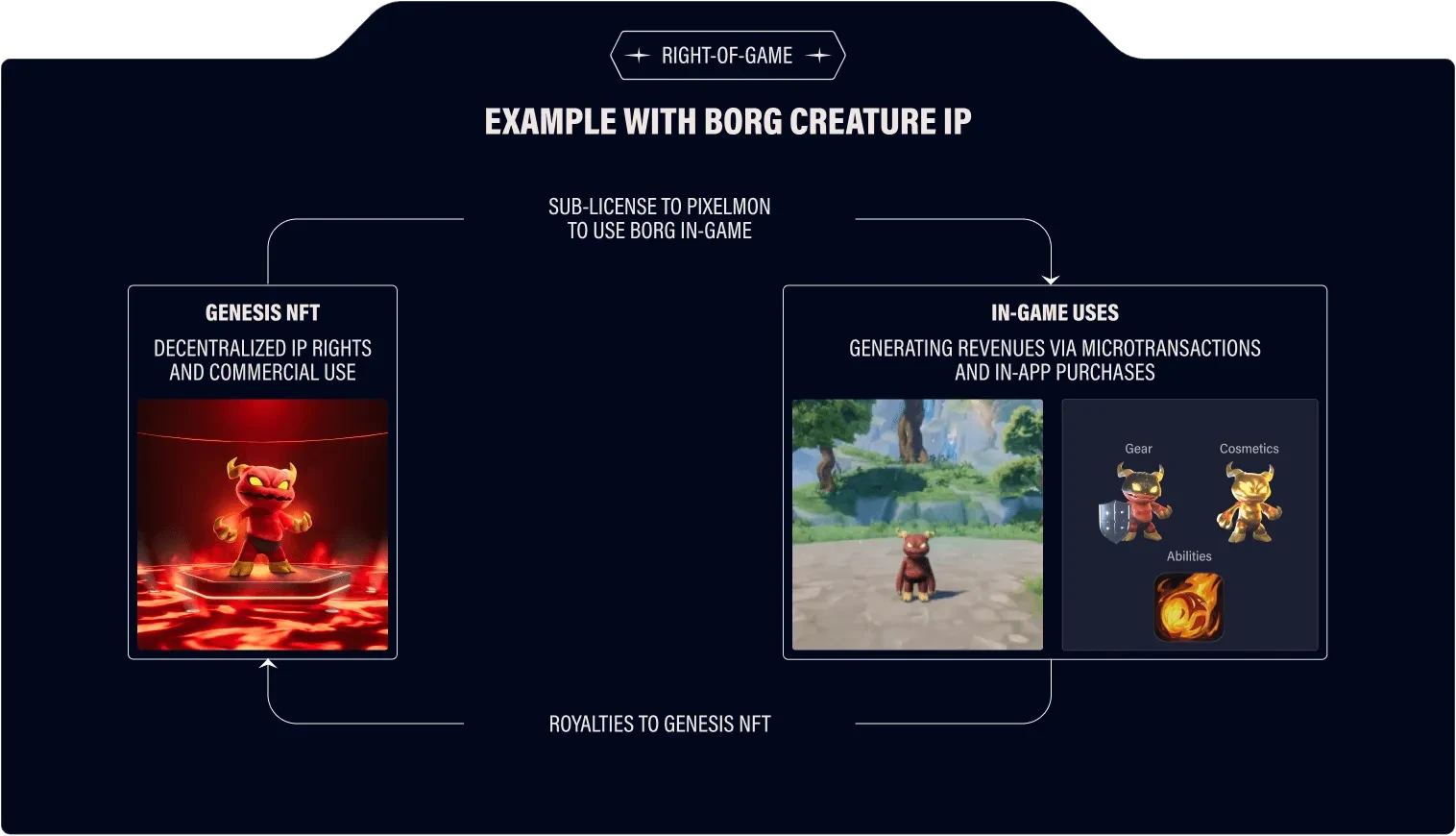

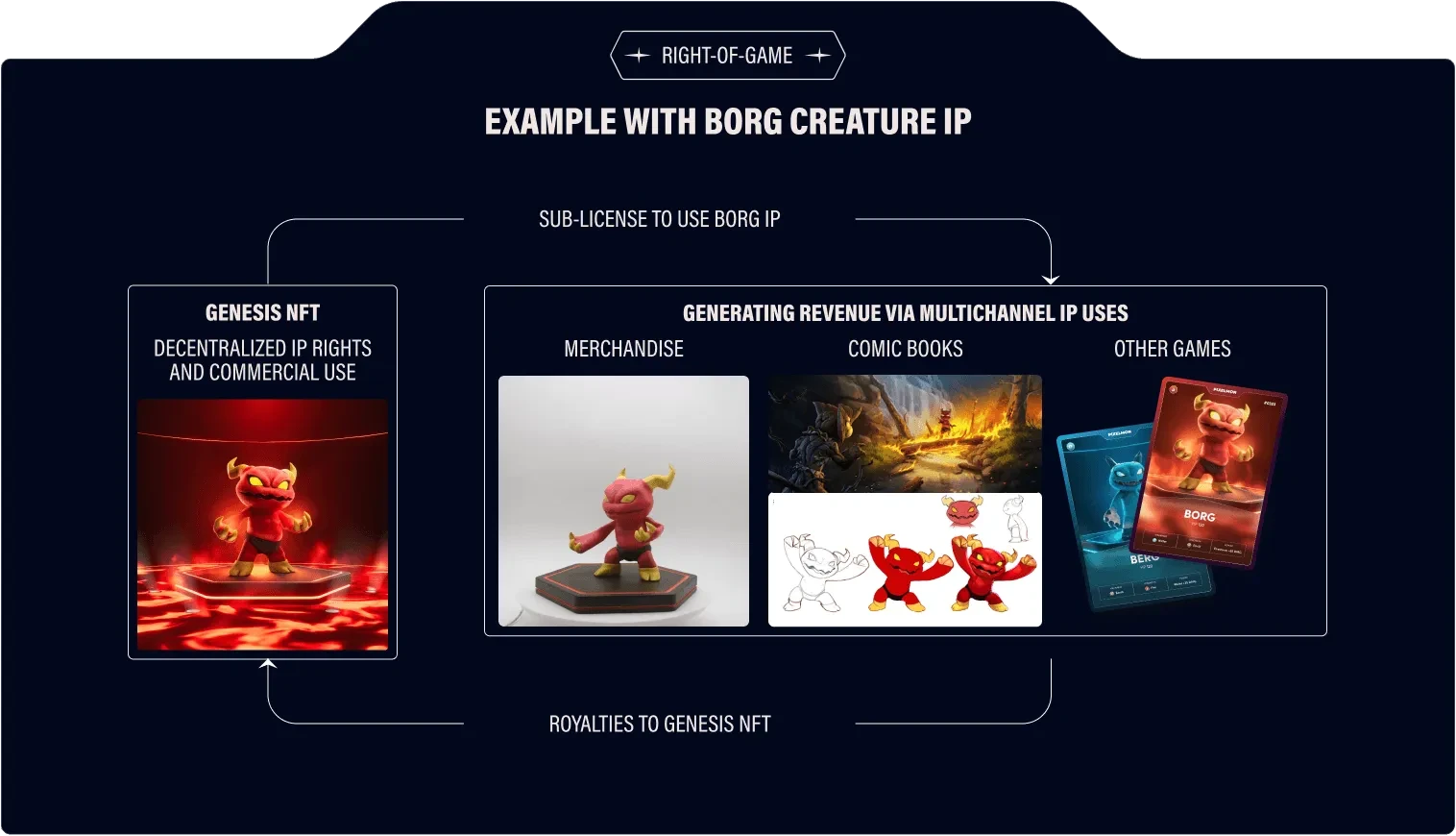

Pixelmon 构建了两套 NFT,将其命名为游戏所有权(Right-of-Game、RoG)系统,它由创世 NFT 和 游戏内 NFT 组成。

Genesis NFT 包括特定资产的 IP 所有权,面向有兴趣获取艺术品,希望发掘、谈判和商业化与该艺术品相关的 IP 的各方。而游戏 NFT 是面向消费者/游戏玩家的产品。

通过免费游戏与游戏内 NFT,降低游戏入场门槛,相应地能够引入大量的基础用户,据 Pixelmon 白皮书表示,游戏玩家是 Pixelmon 游戏的最终消费者,也将成为生态系统的增长引擎。而庞大的用户群体能够为游戏 IP 带来附加价值,并随着用户数的增多实现价值的线性增长。

而 Genesis NFT 则是 RoG 系统的关键。虽然这些 NFT 不具备游戏内功能,但将获得游戏内资产的空投,同时还可获得来自游戏生态活动的费用奖励。

另一方面 Genesis NFT 将作为 IP 所有权、特许使用权费用(franchise)的凭证。Pixelmon 表示,通过去中心化的 IP 和特许使用权费,Genesis NFT 持有者有动力去发掘、谈判和落地 IP 的商业化应用,相应地赚取特许使用权费。

综上,Pixelmon 想通过免费游戏引入大量的游戏用户,构建生态用户基础,然后在生态的基础上发展每个角色的 IP,例如宝可梦那样赋予每个角色单独的、突出的 IP 价值。

理想过于丰满

诚然,此前也有过少数Web3原生 IP 破圈、创造价值的案例,例如 2022 年中国李宁曾推出以 BAYC #4102 形象为主题的“中国李宁无聊猿潮流运动俱乐部”系列服装,还曾在线下推出 BAYC 快闪店。Pudgy Penguins 推出的玩偶“Pudgy Toys”上架亚马逊两天内售出超 2 万个。但终究只是少数个例,PFP 类型的 NFT 可以认为是专注于 IP 发展的产品,然而并未有多少 PFP NFT 实现长期存活以及破圈传播,更不谈与一个庞大的游戏生态所结合。

因此,Pixelmon 所提出的链游模式确实可以说是一条新颖的、理论可行的道路,但作为首批探索该模式的链游,仍将面临较多的挑战。

融资背景与代币发售

虽基于发展模式分析,Pixelmon 的发展道路仍然较为漫长,但从项目融资背景、市场预期等方面来看,Pixelmon 仍具备一定实力。

本月初,NFT 项目 Pixelmon 宣布完成 800 万美元种子轮融资,Animoca Brands、Delphi Ventures 和 Foresight Ventures 以及 Amber Group、 9GAG 创始人 Ray Chan 和 Immutable 联合创始人 Robbie Ferguson 等参投。Pixelmon 称,该团队计划利用新融资推动休闲和中核游戏的开发。

而在更早的 2022 年,Pixelmon 曾进行过一轮 NFT 发售,发售价达 3 ETH,累计销售额达 7000 万美元,后因披露的游戏内容品质不及预期而暴跌 90% 。而后 Pixelmon更换项目领导团队并推出新的路线图,经过两年的重新建设,目前 NFT 价格回升至 1.65 ETH,游戏品质也有大幅提升。

代币经济学

Pixelmon 的合作伙伴 IP 管理协议 Mon Protocol 宣布推出 MON 代币,代币总量共 10 亿枚,MON 总量的约 36% 将通过两种分配机制直接分配给 Pixelmon 社区,MON 总供应量的约 29% 将通过生态系统基金间接专用于 Pixelmon 和 Mon Protocol 社区。

MON 是 Mon Protocol 的治理和实用代币,而 Mon Protocol 将在 Pixelmon 生态中作为 IP 协议进行首次应用。而在 Pixelmon 生态中,MON 代币将发挥游戏内代币、IP 治理权代表等作用。

代币预售

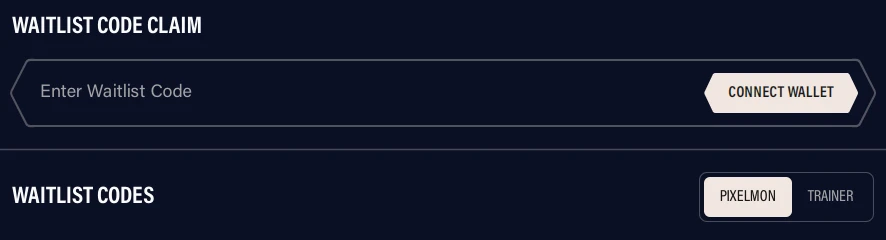

MON 代币预售将以固定价格发售,其流程和要求如下:

参与代币预售的钱包首先需要获取 Waitlist Code,每个 Waitlist Code 等效于一手认购机会;

每一手能够认购 2, 888 枚 MON,一共将预售 62, 092, 000 枚代币;

若出现超额认购,将通过抽奖形式进行选取;

Waitlist Code 将由 Pixelmon 所推出的两个 NFT 系列产生,分别为 Pixelmon Gen 1 和 Golden Trainer,前者具有 3 个以上 Waitlist Code,后者有 2 个以上,根据稀有度的不同所分配的 Waitlist Code 数量将进一步增加。

认购将以 ETH 进行,目前官方未披露具体价格,仅预告每手价格约在 200 美元至 300 美元之间。若以 250 美元折中计算,则代币单价为 0.0865 USDT,对应 FDV 达 8650 万美元。

结论

Pixelmon 的代币定价相较于主流链游几千万、上亿的市值属于中等水平,并且刚宣布了大额融资,具备一定短期潜力。但其项目愿景十分宏大,能否成功落地现在仍难以给出定论。

注:「GameFi 猎手」是Odaily星球日报推出的专注于 Web3 游戏的全新版块,定期更新热门项目动态、拆解经济模型以及分享交互教程。寻求报道,请联系微信:AmadeusL。