前言

在投资领域,有一个普遍认同的原则:"收益与风险成正比"。这在动态且多变的Web3行业表现得尤为明显。尽管黑客事件依然频繁发生,影响广泛,但对于许多用户而言,成功规避或控制风险仍是一大挑战。

随着加密货币市场的回暖和链上资产活跃度的增加,黑客事件的频率也有明显提升,例如 Orbit Chain 遭遇攻击损失超 8000 万美元,KyberSwap 被盗超 4800 万美元等。这些事件更加突显了平衡收益和资产安全的重要性。

在这种背景下,找到一种既能获取收益又能有效规避风险的方法成为用户迫切的需求,Amulet V2应运而生。

Amulet 介绍

Amulet(护身符协议)是 Solana 生态中 DeFi 保险协议,于 2022 年第一季度立项,其早期目标是为用户提供简单可靠的保险服务。2022 年第二季度,Amulet 完成了约 600 万美金的种子轮融资,由 Gumi Crypto 领投,其它投资者包括 Solana Ventures, Animoca Brands、NGC Ventures、Longhash Ventures、Mirana Ventures、Defiance Capital 以及 SevenX 等基金。

Amulet V1的发展正值 Solana 生态的繁荣发展时期。在 FTX 和 Solana 生态遭遇波折震荡后,Amulet 经历了一段平稳的发展时期。在这期间,Amulet 团队基于对 DeFi 保险用户实际需求的理解和Web3行业核心痛点的分析,于近期升级并发布了投资加保险一体化收益平台。

Amulet 表示,Amulet V2作为升级版产品,将收益策略和内嵌保险结合在一起,提供了以用户为中心的一站式收益平台。该平台通过透明的风险评估和综合的风险管理,为用户提供资产保护。与此同时,Amulet V2的部署已经覆盖了 Solana、Ethereum 及主流L2等多个生态系统。

同时,Amulet 代币 $AMU 将于 2024 年 1 月 23 下午 5 点在 KuCoin、Gate.io、Bitget 以及 HTX 四家主流交易所同步首发上线。

收益与保险的巧妙结合

Amulet Vaults 和 AmuShield 作为 Amulet V2的核心功能,为用户同时提供收益机会与安全保障。

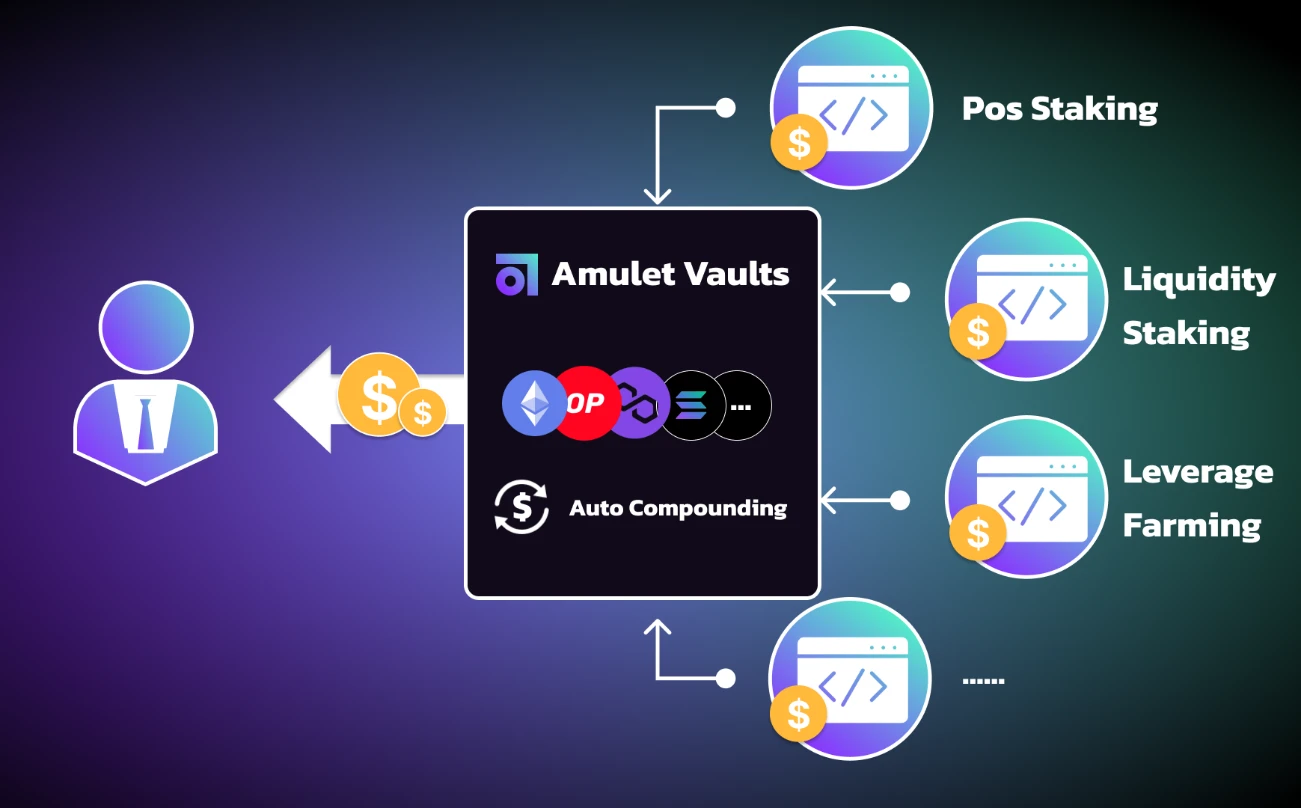

Amulet Vaults

Amulet Vaults 通过其全面的分析,为用户提供精选的收益机会,并通过综合的策略分析和透明的风险评估帮助用户在复杂多变的Web3市场中做出更为明智的投资决策。

Amulet V2使用 ERC-4626 代币化保险库标准,实现与众多Web3收益平台无缝整合。用户可以将其资产存入 Amulet Vaults,通过由智能合约管理的预定收益策略,例如 PoS 质押,流动性质押,杠杆挖矿等以产生收益。产生的收益有多种形式,包括质押收益以及额外的 AMU 代币,并且所产生的收益还将由平台自动重新投资以获取复合收益。

同时,为了最大化用户的收益,Amulet V2引入治理激励机制。在优化基本收益和提供 AMULET 代币奖励后,用户可通过治理激励再次提高年化收益率。

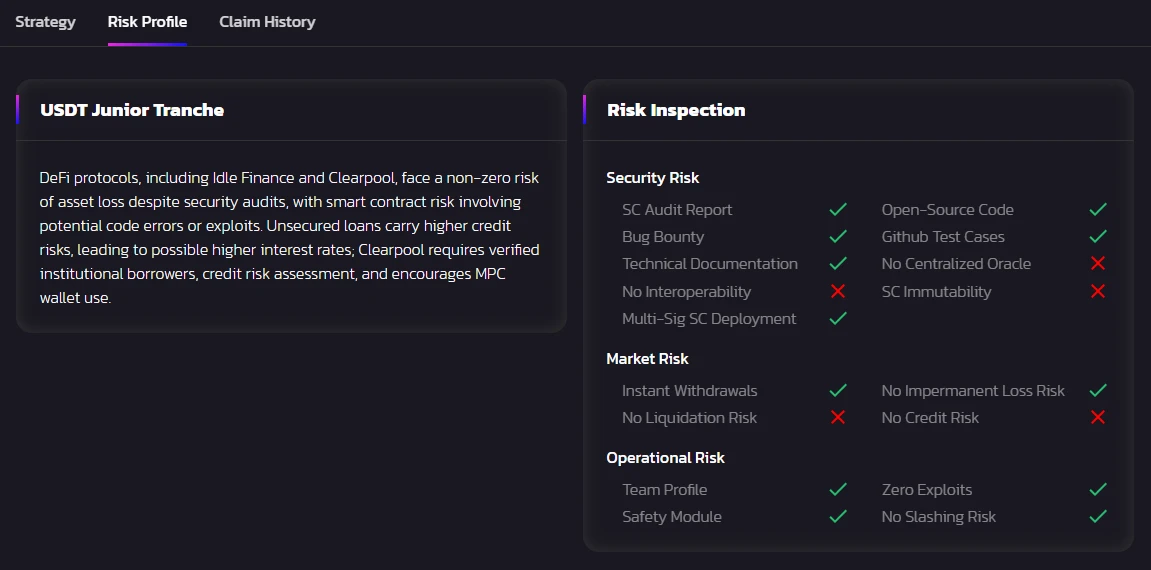

与其他收益平台相比,Amulet V2的独特之处在于其为每个收益策略均提供了全面、透明且完全客观的风险分析,主要涵盖安全风险、市场风险以及运营风险检查,旨在为用户在投资活动中赋予更强的决策能力,合理均衡收益与风险。

AmuShield

AmuShield 利用 24/7 的资产监控,紧急响应机制以及创新的参数化保险服务,保障用户资产安全,有效地应对各种意外情况。

全天候实时监控与紧急响应

AmuShield 支持实时监控 LP 代币价格,即每个策略底层 LP 代币的可提取资产金额。一旦 AmuShield 监控到收益策略底层资金池中的 LP 代币价格低于预设的正常水平,便会启动紧急资产找回机制,并进行资产提取。

参数化内嵌保险

AmuShield 设立专用基金“Amulet Safety Fund”,为用户提供坚实可靠的资产保护,在 Amulet V2初期阶段,Amulet 安全基金("ASF")包括$ 10 M AMU 代币和从 Amulet 策略产生收益当中收取的保护费用,同时 Amulet 计划在后期引入更多安全合作伙伴扩大安全基金规模,为用户提供更广泛的保护。需要注意的是,ASF 仅提供有限和动态的资产保护,以抵御实际损失,意味着 ASF 所提供的资产保护取决于其当前的可用资金。

当 AmuShield 监测到 LP 代币价格已经低于预设的正常范围,保险机制将会自动运行,为用户提供迅捷的资产补偿,该资产补偿可通过 Amulet V2平台直接领取,省去了繁琐的索赔申报流程,大大提高了赔偿效率。

代币经济学

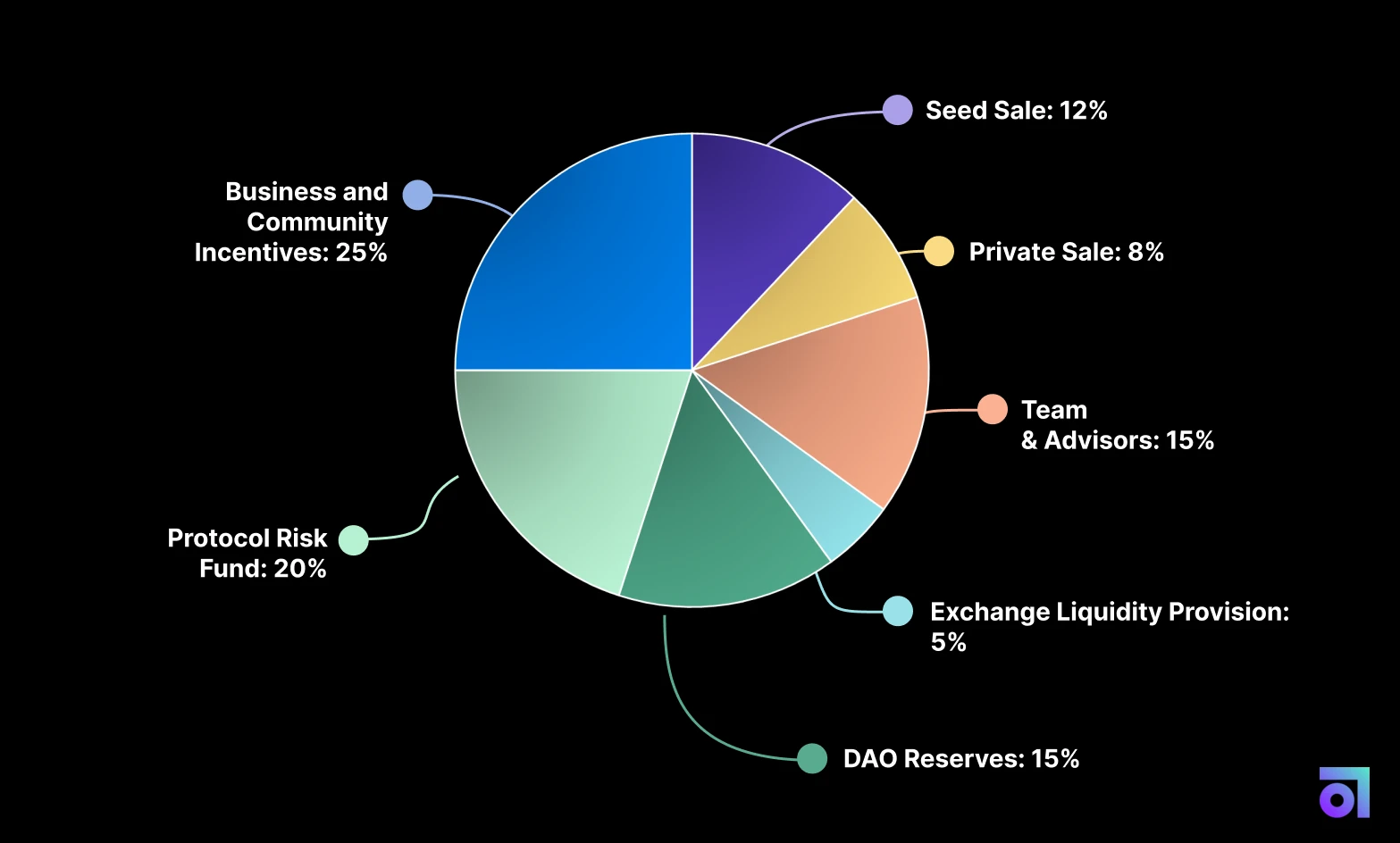

代币经济学方面,$AMU 作为 Amulet 协议的治理代币,赋予了社区成员在产品发展上的决策权,并且保证了平台的透明度和可持续发展。

$AMU 代币的初步总供应量设定为 10 亿(1, 000, 000, 000)枚。其中, 25% 的代币供应将全部被用于项目和社区激励,其余部分则用于募资、流动性启动以及团队激励。

代币治理

$AMU 代币治理将采用 veAMU 代币模式。

用户可通过质押 $AMU 获得 veAMU,veAMU 数量与质押的数额和期限成正比。

用户可使用 veAMU 对产品升级、功能调整、收益分配以及其他事项进行投票。

用户可使用 veAMU 参与项目收入分配决策,这将确保代币持有者的利益与协议的长期发展紧密结合。

代币激励

$AMU 代币赋予平台长期忠诚用户以及代币持有者额外奖励渠道,不仅为 Amulet 项目的激励机制提供动力,也为$AMU 代币的功效和协议的发展提供了更强的稳定性。

挖矿奖励:用户可通过质押直接获取$AMU 代币挖矿奖励,同时使用 veAMU 进一步提升$AMU 代币奖励分配。

治理奖励:积极参与协议治理的用户可以获得额外代币奖励,治理奖励能够有效提高协议治理参与度并且为用户的贡献提供回馈。

收益分成:Amulet 计划推出更多直接的收益分成计划,通过共享平台的收益,让用户直接受益于协议的发展,并且鼓励用户使用奖励代币参与协议治理。

未来计划

Amulet 团队表示计划在 2024 年进一步扩展其产品功能和市场覆盖范围,包括进行安全审计、正式上线、代币发行和社区扩张等关键环节,同时计划将平台推广至更多的区块链生态系统,以及推出更多自研的收益策略和保险服务。

Amulet 是集收益和内嵌保险于一体的服务平台,致力于打造一个高收益、安全、透明且具有资金保障的Web3收益平台。