原创 | Odaily星球日报

作者 | Loopy

今日,原生 USDC 正式进入 Cosmos 生态,Circle 官方宣布 CCTP 已接入 Noble 链。Noble 链是一条 Cosmos 生态内的链,这一链的主旨既是为 Cosmos 生态引入稳定币。

目前,CCTP 部署完成后,Circle 跨链转账协议(CCTP)已于 11 月 3 日在 Noble 的测试网上线,预计将于 11 月 28 日在主网上线。

而本次开发由Circle、Noble 和 dYdX 团队合作完成,其目的是方便USDC 在不同网络间向 dYdX 链的转移。尽管主要目的在于 dYdX,但得益于方便的 IBC 跨链,无疑这将使整个 Cosmos 生态获益。这一功能将通过以简单、便捷且安全的方式将 USDC 引入 Cosmos 之中。

dYdX 的市场负责人 Nathan Cha 表示,DeFi 的一个主要原则是为所有用户提高可触达性。dYdX 非常乐于见到这样的合作。

而对于 Cosmos 用户来说,CCTP 的引入,又和其他跨链桥、其他稳定币有何不同?这就要从 CCTP 独特的“铸造-燃烧”机制说起了。

独有的“销毁-铸造”机制

CCTP 即 Cross-Chain Transfer Protocol,是 Circle 推出的无需许可的官方跨链桥。

CCTP 与常见的桥有所不同的是,这一桥并非采用常见的“锁仓-铸造”模式,而是采用“销毁-铸造”模式。

在较为主流的“锁仓-铸造”机制中,桥协议于两个链上建立流动性池,通过在原始链一侧锁定代币、目标链一侧铸造代币来实现代币在不同链间的流动。

由于 USDC 合约的权限由 Circle 控制,第三方桥并不能铸造原生 USDC。CCTP 则可在原始链上销毁原生 USDC,并在目标链上铸造等量的原生 USDC。

用户跨链之后,CCTP 会在原始链上销毁 USDC。随后 Circle 会进行取证,包括观察和证明原链上的 USDC 销毁交易,原链应用程序需要请求来自 Circle 的「签名证明」才能进行销毁,同时也必须在获得「签名证明」后才能在目标链上授权铸造指定数量的 USDC,完成铸造后访客将 USDC 发送至接收者的钱包地址。

在这个过程中,并不存在资金池,当然也没有数以亿计的资金沉淀。这一流程优化了资本效率和流动性体验。对用户来说更关键的是,在不同链上收到 USDC 都是原生 USDC,由 Circle 直接提供美元担保,无需担心目标链的 USDC 和原始链的原生 USDC 脱锚。

而在应用上,Circle 给出的主要用例包括交易、借贷、支付、NFT 和游戏,例如跨链 Swap、跨链存款、跨链购买 NFT 等。

没有资金池,跨链是否更安全?

在传统的“锁仓-铸造”模式的跨链中,弊端十分明显。为了维持池子中两个币种 1: 1 的价格锚定,需要 LP 提供者进行做市,而池中大量锁定的代币也成为绝佳的黑客攻击目标。

Odaily星球日报曾盘点史上规模最大的十次跨链桥攻击。2022 年 3 月,Ronin Network 的跨链桥遭到攻击,损失总额高达 6.24 亿美元。这也是史上最大规模的跨链桥被盗事件。Chainalysis 研究发现,仅 2022 年,跨链桥攻击事件就已造成超过 20 亿美元的资金损失。

此外,“锁仓-铸造”的模式天然将桥的两端划分为“原始链”和“目标链”,两侧代币分别为原生资产和桥资产,大量被铸造的代币与原生资产并不相同。若桥出现安全问题,目标链被铸造的资产将会面临脱锚风险。

在 2022 年 11 月的“pGALA 事件”中,部署于以太坊主网的 GALA 代币并未出现任何问题。而 pNetwork 跨链桥出现了安全问题,由其在 BNB Chain 发行并铸造的 pGALA 被巨量增发, 1 枚 BNB Chain 的 pGALA 不再拥有对应的 1 枚以太坊 GALA 作为支撑,pGALA 随即归零。

对于资产发行方来说,在各链上流动性割裂的问题也影响着资产的使用。(CCTP 的文档显示,这一点才是 Circle 最在意的——“统一整个生态系统的流动性”。)

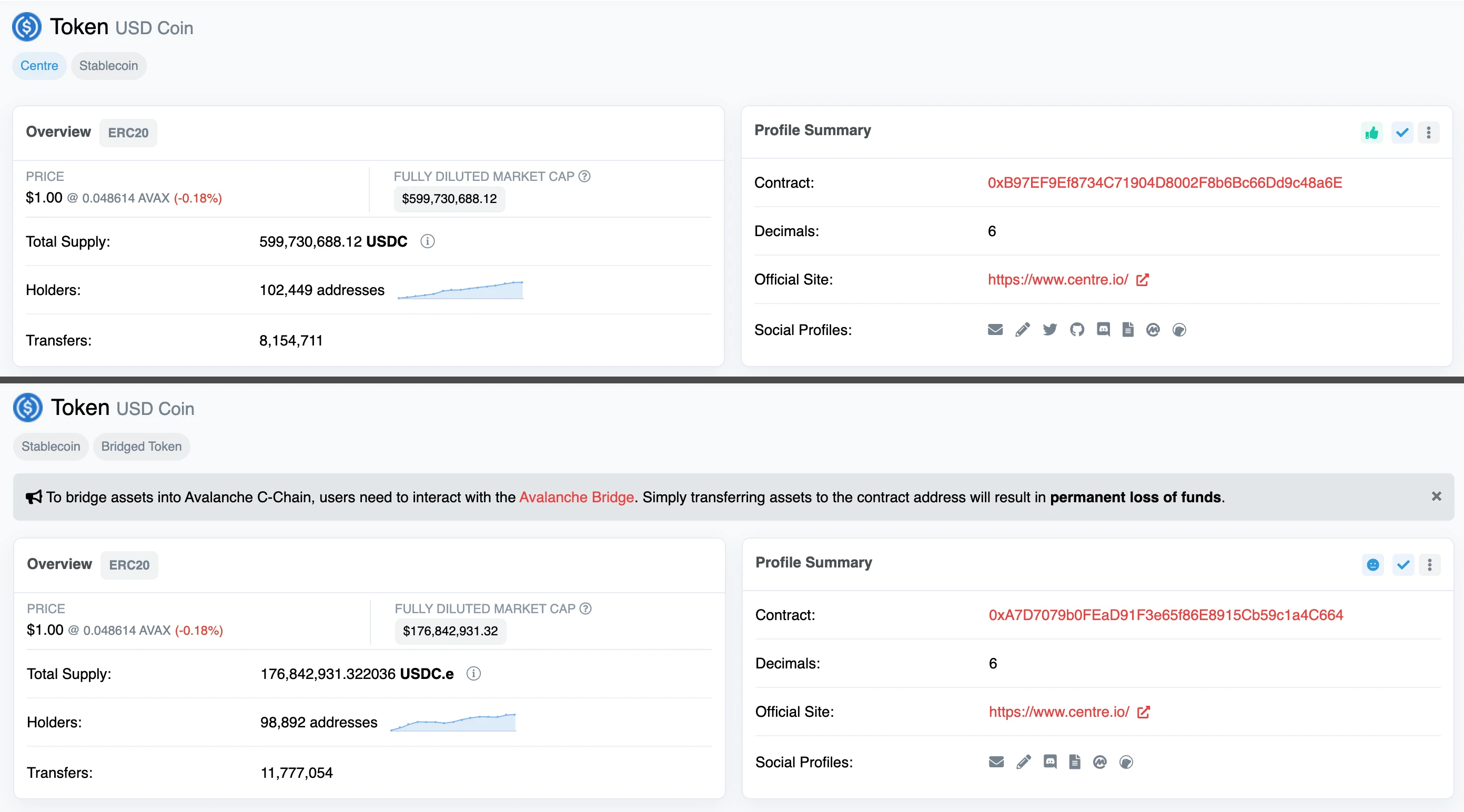

以 Avalanche 为例,目前在这一网络存在两种主流的 USDC 代币。5.99 亿枚由 Circle 发行的原生 USDC,合约尾号为“8a6E”。1.76 亿枚 Avalanche 官方桥发行并铸造的 USDC.e,合约尾号为“C664”。

(跨链资产 USDC.e 不由法币支持,而是由以太坊链的 USDC 通过桥支持)

对于用户来说,这两种 USDC 使用体验并无区别,均为价值 1 美元、可在各大 DEX 使用。但有趣的是,若用户同时持有这两种 USDC,钱包中将会同时出现两种币。而在 Avalanche 的 DeFi 世界里,基于两种不同的 USDC 所构成的大量交易对更是混乱,用户总会在不经意间进行“用一种 USDC 兑换另一种 USDC ”的低效交易。

同一链拥有两种 USDC,是一种更为直观的体验流动性割裂的方式。而这种割裂,将其放到更加广阔的多链生态里则更为明显。

为了在多链使用 USDC,大量的非原生 USDC 被由桥所发行。而原生的 USDC 此时在做什么?在被作为 LP 锁定在资金池里。这种锁定模式无疑将会牺牲大量的资本效率。

一般来说,主流的桥为了提供充足的流动性,总需要在桥的两端分别锁仓大量的代币。这些代币虽然可以支撑日常的交易,但长期停留在 LP 池中,却让市场上可以流通的代币减少了。我们可以粗略认为,为了支持一部分代币的跨链流动,需要把相当一部分的资金沉淀在池子里,无法被有效利用。

这无疑在某种程度上降低了代币流动性和资本效率。CCTP 对于加密世界中的多方都将产生一定影响,首当其冲便是跨链桥。稳定币在各大主流跨链桥中都是交易量较高的币种。CCTP 对跨链桥的市场份额或将形成强烈的冲击。

而除了既存互操作性协议外,LP 们或许也并不欢迎 CCTP 的到来。传统跨链桥的锁仓模式需要大量 LP 提供资金,而在各大跨链桥上,稳定币跨链 LP 做市一直是一个低风险赚取收益的标的。

Cosmos 的稳定币困局

本次 CCTP 在 Noble 的部署,对于 Cosmos 和 Circle 来说都是值得记录的大事件。但有趣的事,dYdX 却是另一个积极推进协议部署的合作方之一。

看似无关的 dYdX,实则将极大的受益于 USDC 的原生部署。2022 年 6 月,dYdX 宣布将转移至 Cosmos 生态,并在即将到来的 dYdX V4 版本中实现迁移。这也是第一次出现知名的以太坊原生 DeFi 应用选择逃离。

但在进入 Cosmos 生态之后,Cosmos 生态和 EVM 生态的与众不同让 dYdX 面临着和生态内大多应用相似的困境——稳定币匮乏。

Odaily星球日报在查询了多个主流大型 CEX 发现,它们大多不支持 Cosmos 网络的稳定币充提。而 dYdX 作为链上合约交易所,其对稳定币的需求无疑是巨大的。Cosmos 生态与 EVM 生态间充沛的稳定币流动性,对 dYdX 无疑有着巨大的帮助。

在 Terra 崩溃之前,Cosmos 生态内部的稳定币需求此前严重依赖于 Terra 链上的算法稳定币 UST。而在 UST“归零”之后,Cosmos 生态遭受了不小的打击。此后 Cosmos 的原生稳定币也一直是空缺状态。

尽管 Cosmos 拥有 Axelar 跨链的 USDC、通过 Nomad 桥跨链的 USDT、USDC 等,但这些代币均非原生代币,在安全事件频出的背景下,跨链桥的安全口碑毕竟还是不如原生发行的代币稳健。而且,不同跨链产品所发行的稳定币也因映射格式不统一原因导致流动性被分散。

直至今年 6 月,Tether 才正式官宣将通过 Kava 网络发行原生 USDT。这也为 Cosmos 这个繁荣且历史悠久的老牌生态弥补上了稳定币的缺位。

至此,在 USDT、USDC 两大稳定币双双进入 Cosmos 网络。Circle、Noble 和 dYdX 团队之间合作,看上去对于三者而言都是一场颇为美好的共赢。而对于 Cosmos 生态来说,稳定币这“最后一块拼图”的补完,是否能将近期重新翻红的 ATOM 带领向更远大的未来呢?