注:本文来自@Loki_Zeng 推特,其是@Foresight_News专栏作者,原推文内容由MarsBit整理如下:

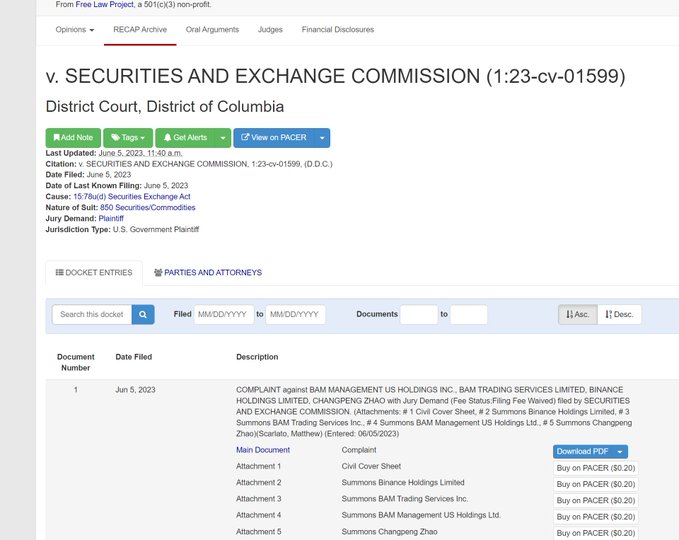

找到了SEC的起诉文件

https://courtlistener.com/docket/67474542/v-securities-and-exchange-commission/

描述:美国证券交易委员会提交了针对 BAM MANAGEMENT US HOLDINGS INC.、BAM TRADING SERVICES LIMITED、BINANCE HOLDINGS LIMITED、CHANNGPENG ZHAO 的投诉,即起诉的目标是3家Binance的实体+CZ本人

第一项指控:Binance在CZ的领导下提供证券的三项核心服务:交易所、经纪-交易商、清算。Binance意识到按照美国法律从事这些业务需要注册,但选择了不注册,以逃脱监管。

第二项指控:Binance and BAM Trading非法提供和销售未注册证券,包括BNB Vault、Staking、Simple Earn。用户没有完全获取实际信息,包括潜在的风险。

注:这一条指控类似之前对Gemini的指控

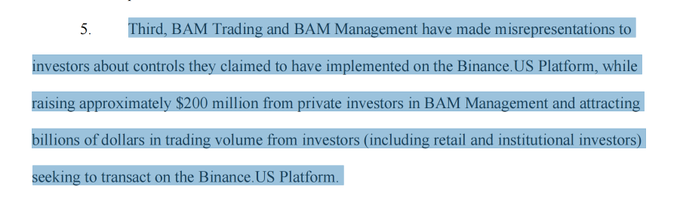

第三项指控:Binance and BAM Trading对Binance US做出了虚假称述。并藉此获得了大约2亿美元的投资和数十亿美元的交易额。

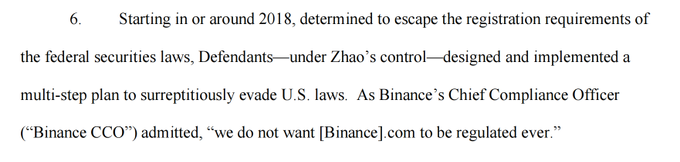

SEC认为,Binance从2018年开始通过一个多步计划逃脱美国监管。 Binance CCO承认:【我们永远不希望Binance受到监管】

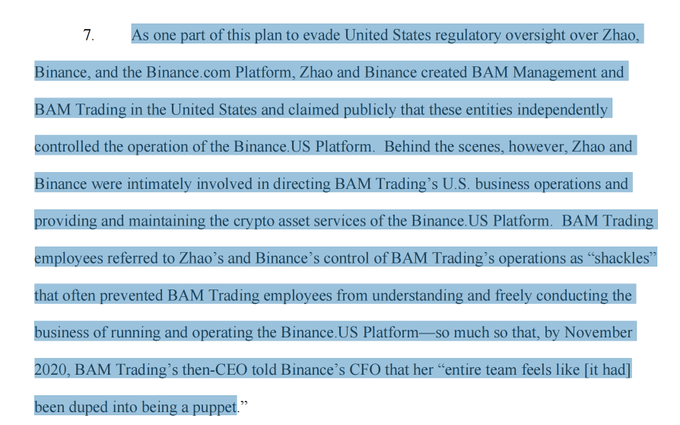

Binance成立了BAM Management 和BAM Trading两家主体用于Binance US的运营。尽管名义上独立,但CZ和Binance仍保持对Binance US的控制直到2020年11月。

BAM Trading 的时任CEO曾向Binance的CFO表示,【整个团队(BAM Trading)被当成了傀儡】

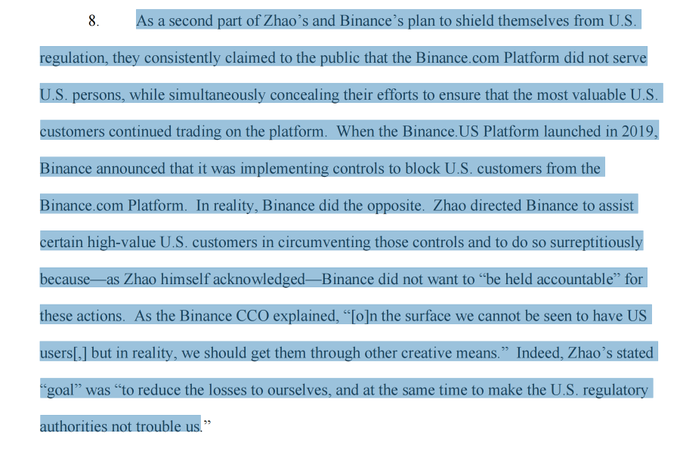

SEC认为尽管自19年US站成立后,Binance一直在宣成Binance主站 不服务美国用户,并采取了相关措施避免。

但在实际行动上,CZ指示币安秘密协助某些【高净值用户】摆脱限制。

SEC认为CZ的目的是【不会使得监管找麻烦】的同时【减少损失】

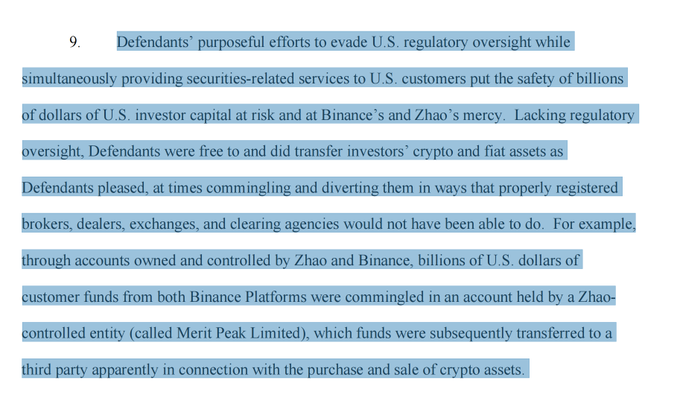

这种做法使得数十亿美国投资者的资金被置于风险之中,由Binance和CZ直接控制。

Binance和CZ拥有自由转移资金的能力,它们也这样做了,例如,2个平台(Binance US和Binance)的资金被转移到同一个实体(Merit Peak Limited),并在之后转移到了第三方地址。

注:这解释了之前【币安混合用户资金】的传闻,关键点不在于【用户资金】,而在于这些资金属于Binance US的美国投资人。

第10条是对CZ的谴责,不重要。

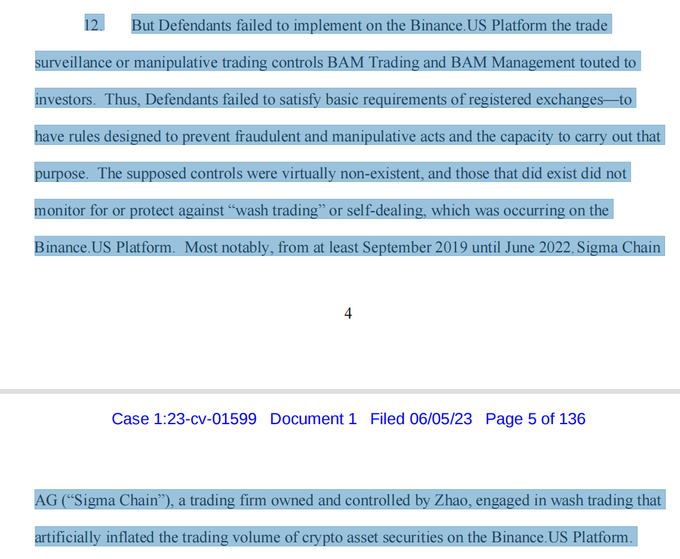

BAM Trading and BAM Management声称监控(上文没说是什么监控)是为了避免Binance US上的市场操纵行为。

但SEC认为BAM Trading and BAM Management未能实施有效的交易监视或操纵交易控制(按照这里说的,前文的【监控】应该指的是合规层面的内控工作)。

SEC认为那些有效的措施都不存在,存在的都是无效的措施。

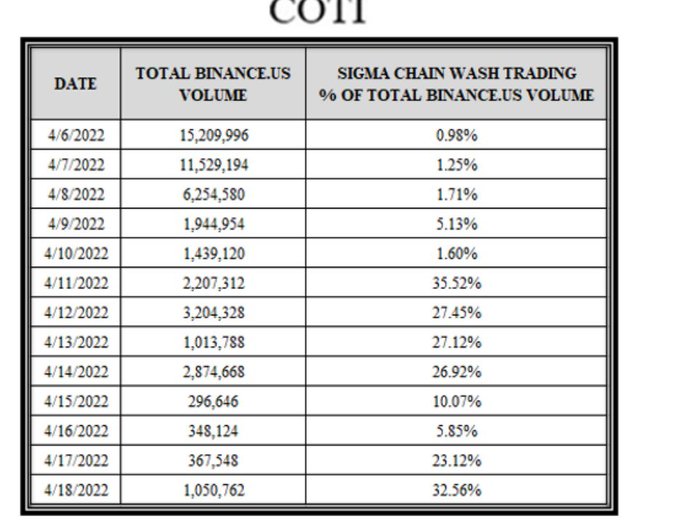

至少能够确定的一点是:CZ控制的Sigma Chain AG在Binance在2019-2022年期间从事虚假交易,夸大了Binance US的交易量。

SEC最后总结:

依据《证券法》和《交易法》,CZ和上述的几家公司违反并将继续违反:

1)发行和销售未注册证券

2)在Binance平台上影响未注册证券的交易

3)组合核心证券市场功能并故意逃避登记

4)明显违反利益冲突原则

注:有说法称是13条指控,指的是SEC一共总结了13条,不是说有13条罪名

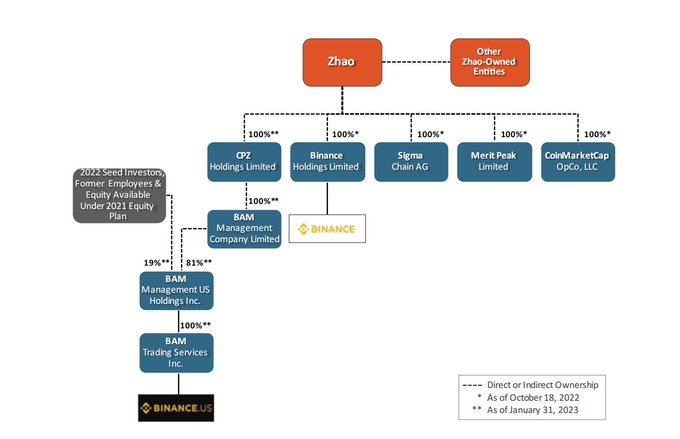

相关主体架构

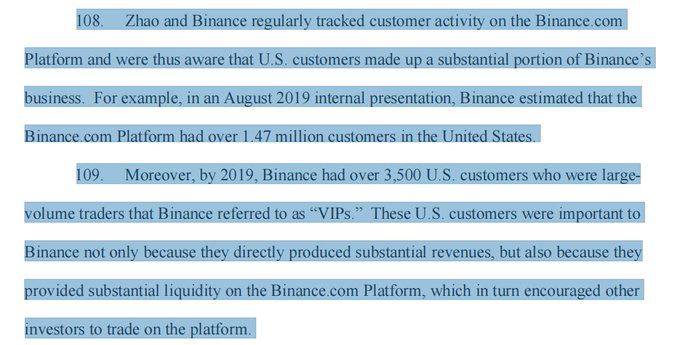

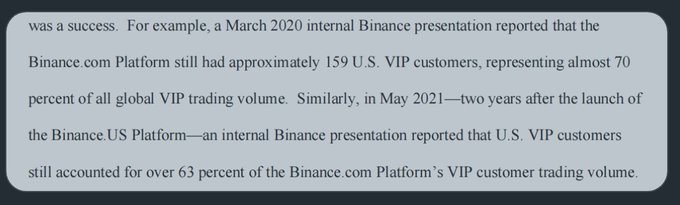

Binance2019年的内部报告显示其有147万名美国用户,有3500名【VIP】,这些VIP提供了大量的交易量和流动性

接下来详细介绍了Binance的顾问和CZ的规避方法,包括让美国使用VPN、使用新的KYC等... 到2021年5月,美国VIP仍占据币安VIP交易量的63%。

SIGMA CHAIN的刷量占比,最高占到日交易量的35.5%

详情中还提到了发行的BNB和BUSD都是未注册证券,CZ的许多公开发言甚至6年前的论坛发言也被当做佐证的一部分.

除了BUSD和BNB以外,Binance和Binance US还提供其它【未注册证券】的交易,包括: SOL/ADA/Matic等

总结:性质上还是民事诉讼,最坏情况就是关停Binance US,Binance主站彻底退出US市场,并且罚款。

关于理财/Staking认定为证券可以参考Coinbase/Gemini的案子。

如果这几项指控成立,罚金预计不会低,但大概率也就仅此而已。

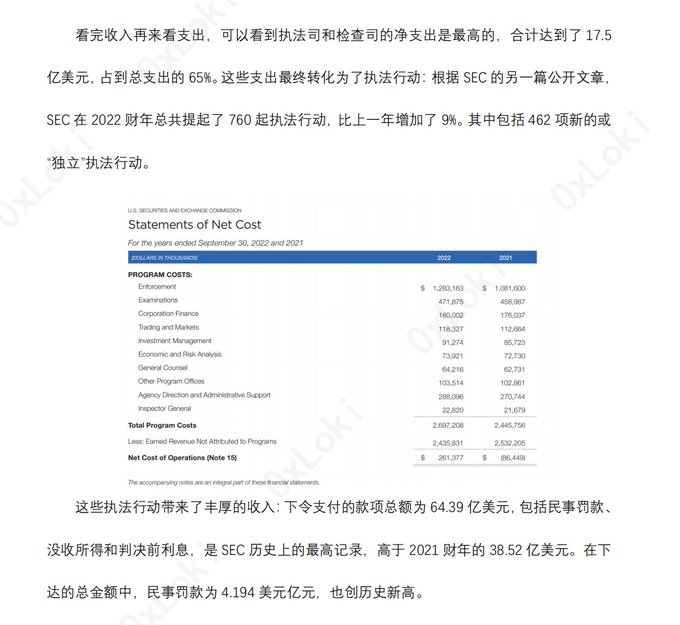

补充另外一个维度的数据:2022财年SEC共发起760项执法行动,下令支付总额为64.39亿美元。

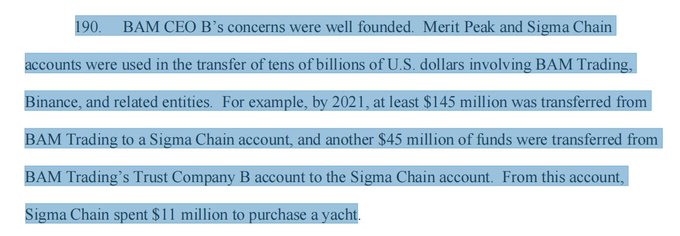

关于1100万美元的游艇:原文说的是在2021年,至少145M资金从BAM Trading转到Sigma Chain,另外45M资金从信托账户转到Sigma Chain。

然后SigmaChain用1100万美元买了游艇。没有一句话表明这1100万是客户的钱,拿自己/自己实控公司的钱买游艇有啥问题?