从链上数据看,比特币分布正在发生变化,这背后展示出怎样的深层原因?加密行情短期将受哪些因素影响?比特币是否将因港府新政进入牛市?香港新政与美日等国有何不同?香港将于6月1日开始实行加密新规,本文将围绕上述问题进行探讨。

比特币分布发生趋势逆转,香港处于难得机遇期

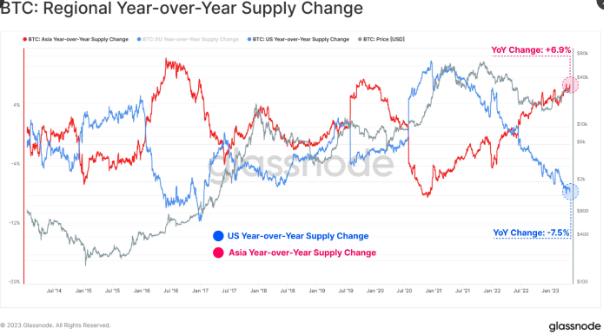

自从今年美国收紧加密市场监管之后,加密代币也出现了一些显著变化,以前位于美国的比特币不断向位于亚洲的钱包转移。Glassnode最近发布的一组比特币同比区域供应变化图,从图中可以观察在美国和亚洲交易时间持有BTC供应形成的变化图。在这张图中,可以注意到,几乎相等但相反的供应变化,这表明以前位于美国的代币继续转移到位于亚洲的钱包。

🔵美国同比供应变化:-7.5%

🔴亚洲同比供应变化:+6.9%

具体而言,在美国严监管背景下,加密交易所退出或资金流失是重要的原因之一。Kaiko在5月17日发推称,最近几周,Binance.US 在美国交易所的市场份额减少了一半,ETH 交易量的跌幅尤其大。Coinbase的交易份额今年以来也出现一定下滑。

这背后原因一方面是FTX爆雷之后,沉重打击美国市场信心,加密资金出逃甚至进一步危机美国加密银行,如硅谷银行等;另一方面,美国金融业发达,对于加密金融具有一定排斥性。哥伦比亚商学院教授、零知识咨询公司的管理合伙人Austin Campbell就表示:加密金融除了监管外,还有两个挑战。其一是美国传统金融机构通常不是技术人才的聚集地。因此,他们有时很难吸引到相关专业知识的人才,这对于完成这些任务非常困难。其二,我认为,在美国,我们已经拥有相当发达的资本市场,而且这些市场大多运转良好。这里的边际成本相对于收益较低,与许多其他司法管辖区相比,收益较低。

在美国驱赶加密金融之时,香港新政为加密市场寻找到一个极具吸引力的“避风港”。香港此轮新政,不同于美国、日本以及新加坡,虽然香港加密市场监管处于早期,但整体规划相对成熟。之前美国加密金融监管整体保持宽松,但却缺乏真正立法,SEC和CFTC对于谁该监管比特币和以太坊都尚未达成共识,致使很多机构想要寻求合规但无从着力。港府新政也不同于日本,日本受早期门头沟事件影响,立法较早较严,这很大程度上保护了投资者,比如日本FTX交易所用户在去年就未有大损失,但在加密市场发展过程中少有创新;港府新政也不同于新加坡的监管宽松,其政策制定相对更为谨慎。港府新政有望使香港成为真正的Web 3金融交易中心,伴随6月1日新政开始落地,加密资产的分布和重心转移预计将进一步加快。

港府新政对短期市场有何影响

今年2月,香港证监会就适用于虚拟资产交易平台营运者的建议规定展开谘询。香港证监会官网最新消息称:“有关适用于获证券及期货事务监察委员会发牌的虚拟资产交易平台营运者的建议监管规定的咨询期于2023年3月31日结束,回应者普遍支持适用于持牌虚拟资产交易平台的建议监管规定。经修订的建议监管规定将于2023年6月1日生效。香港证监会表示,本会注意到,回应者对容许持牌虚拟资产交易平台向零售投资者提供服务表示大力支持。本会将落实有关容许持牌虚拟资产交易平台向零售投资者提供服务的建议。”在这条消息背后,最引人注目的是“本会将落实有关容许持牌虚拟资产交易平台向零售投资者提供服务的建议”,加密市场行情受此影响较大。

除了香港加密新政可以催发牛市的预测,对于哪些代币会被港府批准上线也是市场普遍关注热点,下图为当前部分传统金融市场已经上线的代币。

考虑到港府审慎监管态度,大概率港府首先会批准比特币和以太坊等,后续会根据运作情况逐步放开一些加密资产。在逐步放开的过程中,什么代币会上线会让市场充满猜测空间,这大概率又会进一步引发炒作预期。另外,一个值得关注的问题是对于大陆用户会有如何影响?有大V认为,这可以参照美股在国内。

短期仍然需要警惕DCG 风险

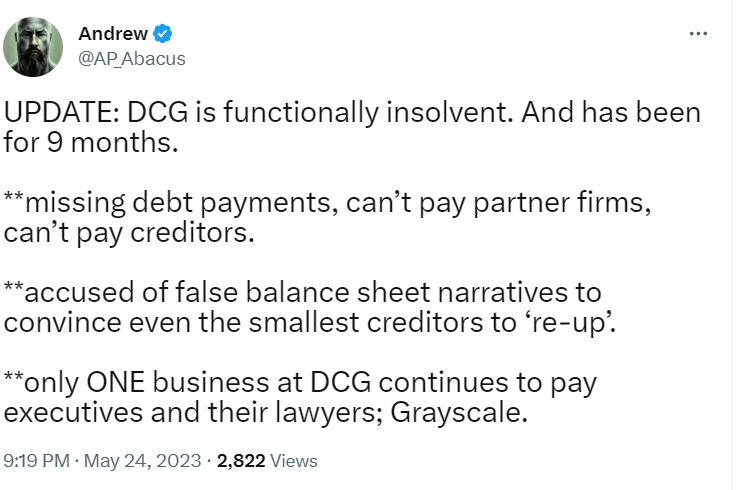

虽然我们在短期内看好港府新政对于加密市场产生的积极影响,不过潜在风险并非没有。从行情和消息面看,5月23日,香港证监会官方人士表示“散户最快下半年可在发牌交易平台买卖虚拟资产”,当日行情走势开始变强;5月28日,香港证监会正式宣布虚拟资产交易平台营运营牌照自6月1日起申领,市场交易热情高涨,比特币走出短期颓势。但5月24日比特币大挫背后的危机,我们并不能忽略,简而言之,那就是DCG的债务危机。

5月24日,市场大V Andrew(@AP_Abacus)发推表示,DCG 已经资不抵债,而且已经9个月了。其拖欠债务,无法支付合作伙伴公司,无法支付债权人。被指控以虚假的资产负债表叙述说服最小的债权人“重新启动”。DCG 只有一项业务,继续支付高管及其律师的费用;灰度。

Andrew(@AP_Abacus)此前曾多次准确爆料DCG等内募,准确度相对较高,市场受此消息影响,极为恐慌。加之,5月22日,Gemini曾发布公告称,Digital Currency Group(DCG)未支付5月11日到期的约6.3亿美元欠款。市场当日在多空博弈之后,选择向下,那么,在港府新政热潮之后,市场将如何变化呢?毫无疑问,利好出尽,DCG债务危机仍将在很大程度上影响市场,投资者须保持警惕。