Author: Chen Mo cmDeFi

The recent heated dispute between Aave DAO and Aave Labs over governance power at the protocol and product layers reflects the broader governance challenges across the industry. Here’s a breakdown of the issue. Who truly owns Aave?

1/6 · The Origin

Aave Labs replaced the frontend integration of ParaSwap with CoW Swap, and the resulting fees were directed to a private address of Labs. An anonymous DAO member, EzR3aL, exposed this on the governance forum, accusing Labs of "privatizing" protocol value. Labs' stance is that this belongs to frontend and product layer revenue, which rightfully belongs to Labs, and is unrelated to the protocol core.

2/6 · First, Let's Break Down Who Aave DAO and Aave Labs Are

- DAO represents the Protocol (protocol layer)

- Labs represents the Project (product layer)

The core dispute is whether Aave is a Protocol (managed by the DAO) or a Project (built by Labs)? And the implications for revenue rights.

Aave DAO is straightforward to understand. It is a unique type of governance organization in the Crypto world, composed of $AAVE token holders who exercise power through voting within the DAO. Almost 90%+ of crypto projects follow this structure; the term "governance token" originates from this. Its primary power is to vote on project proposals, deciding whether to implement certain updates and developments, as well as the future direction of the project.

Aave Labs is a development team responsible for building, updating, and maintaining the protocol (e.g., frontend interfaces, mobile apps). Typically, they also maintain the Aave brand and IP, so on social media and in the market, Aave Labs is often defaulted to being Aave. Its founders are also quite influential on social media.

Generally, Aave Labs and Aave DAO need to collaborate. For instance, Labs leads the development of many plans, optimizations of certain features, and even version upgrades like V3 and V4. These proposals are led by Aave Labs but ultimately decided by DAO vote. Usually, when their interests align, they have a mutually supportive relationship, together forming Aave.

3/6 · What Core Resources Do They Respectively Control?

Once conflicts of interest emerge, these two roles can be separated, as they are inherently independent entities. Let’s look at the core resources and power each holds:

Aave DAO controls the underlying core. For example, the smart contracts; treasury control is in the hands of the DAO. Although Labs can propose development plans, they require a DAO vote to be implemented. So it is the Protocol; the upper layer can be any product that operates. Theoretically, multiple frontend products can be built on top of one Protocol—Aave, Bave, Cave, etc.

Aave Labs controls the frontend, brand, product marketing, and partnerships. So it interacts directly with users and represents a quality product.

Therefore, supporters of Labs generally believe that the CoW Swap integration is purely a frontend behavior, unrelated to Aave's underlying architecture. Labs could even unilaterally decide not to integrate it, so any revenue generated should naturally belong to Labs. Conversely, DAO supporters view this as a form of appropriation because, with the existence of the AAVE governance token, all benefits should优先 flow to AAVE holders or remain in the treasury for the DAO to decide. Additionally, previously, ParaSwap revenue consistently flowed into the DAO. The new CoW Swap integration changed this status, further leading the DAO to see this as a grab.

Both sides have their arguments.

4/6 · Governance Dilemma

This highlights a rather awkward governance and power dilemma. From the perspective of $AAVE holders, they typically side with the DAO, because revenue entering the treasury benefits token holders. Although Labs has corresponding annual expenses, these can be reimbursed through the DAO. If a separate channel for profit can be opened, it seems community power is gradually being eroded.

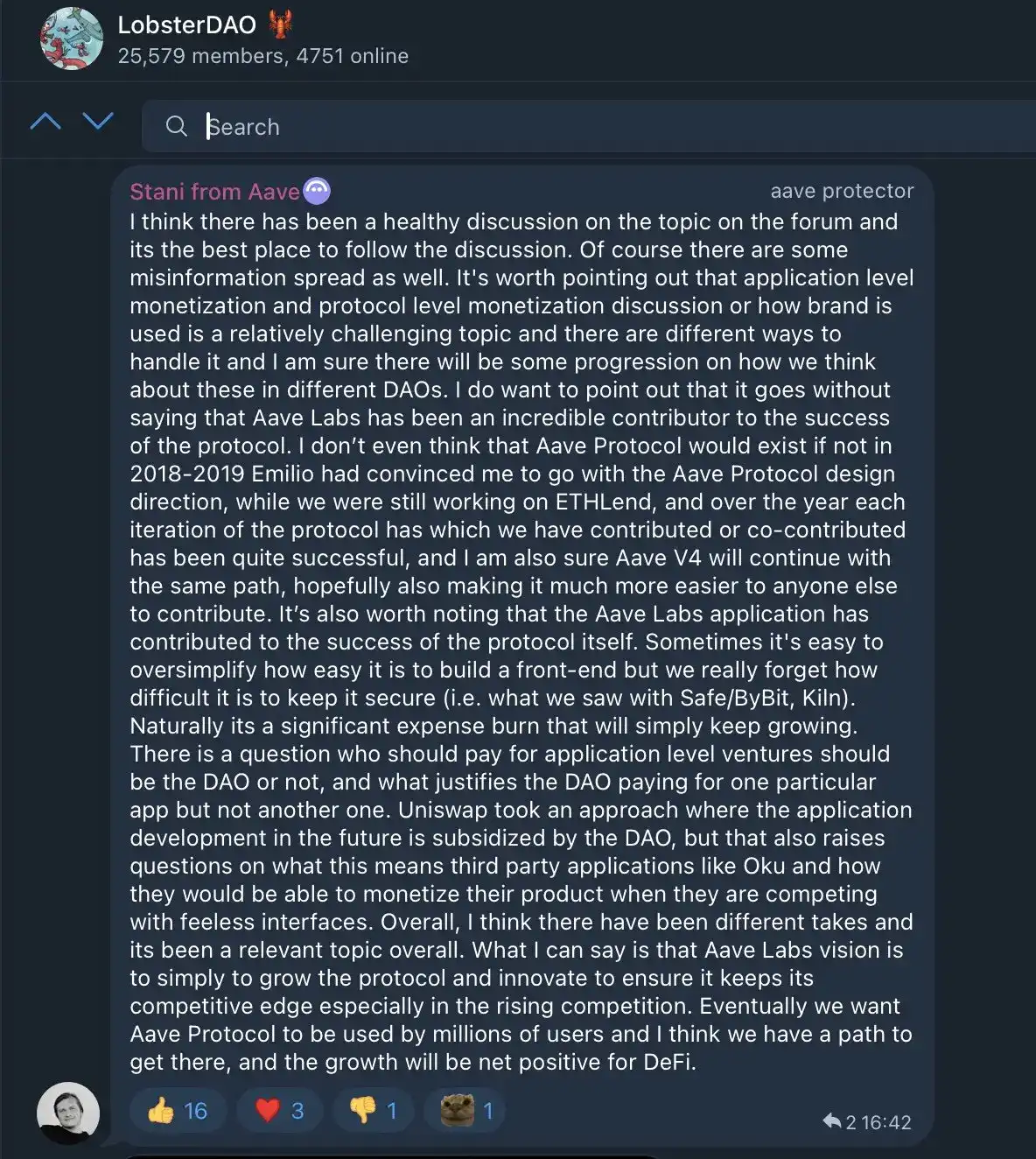

But from Aave Labs' perspective, although the theoretical core control lies with the DAO, and proposals ultimately require a vote to be implemented, from the first version of Aave to now, Labs has played a role in unifying and leading the overall situation, making huge contributions to the project's growth. As Stani said, "If it weren't for Emilio convincing me to adopt the Aave protocol design direction back in 2018-2019, when we were still working on ETHLend, I think the Aave protocol might not have existed at all."

Who is the true owner of Aave?

5/6 · Power Struggle

This governance dilemma exists in most projects. Governance tokens are bought with real money. Ideally, these holders collectively decide the project's future. When the team no longer holds voting power, they could even forcibly replace Labs.

But the reality is far from ideal. Even for projects with a certain market share, when internal team problems and disputes arise, the aftermath often leads to a loss of market position. Sushi is a good example. The DAO can exercise power, and the project can change hands. Although, thanks to smart contract design, even if a project undergoes a major reshuffle, the product functionality can remain perfectly stable. However, judging from past cases, the outcome of splits is usually not good.

The core issue here is that, for now, a DAO is a decentralized organization by nature. Although it has voting power, it struggles to operate efficiently. The community may include independent developers, VCs, and large holders. Once each role begins to exercise its power fully, a proposal can undergo multiple rounds of formulation, modification, and博弈 from the start. The success of a project requires a professional team and continuity. A DAO can hire a new team, but it may be difficult to quickly transition and iterate, easily losing market position. Therefore, the existence of Labs, on the surface,更像 the entity that can "control" the protocol (in collaboration with the DAO).

Personally, I lean towards the two parties eventually reaching a solution to balance the distribution of interests. But currently, everything is under discussion, and no governance vote has appeared. The potential risk behind this is that even if a reconciliation is ultimately reached, this incident has already exposed a divergence in expectations between the founding team and token holders.

Long-term, I remain optimistic about Aave's development because it is one of the few DeFi projects that has been market-verified with a strong moat. The矛盾 of governance power is a problem the entire industry needs to face. How Aave handles this incident may become a benchmark case for the industry in the future.

6/6 · Voices and Discussion

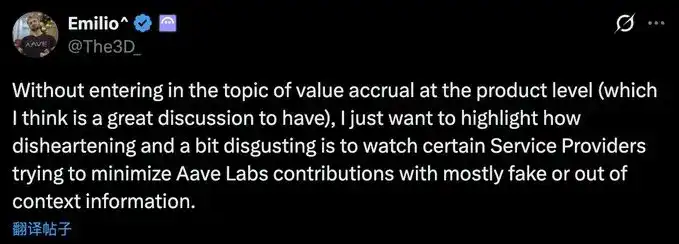

Arguments. Emilio believes someone is maliciously贬低 the contributions and value of Aave Labs. ACI team members pointed out that Aave Labs has repeatedly tried to exploit the DAO and been exposed.

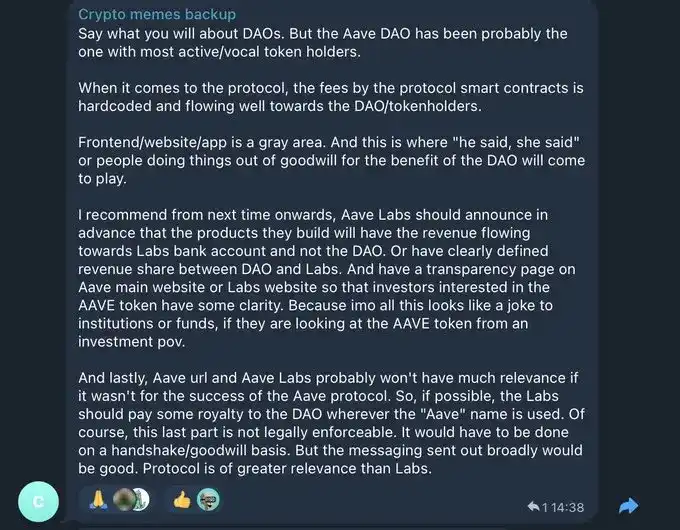

Community suggestions for Labs:

- Labs should announce in advance that revenue from products they build will flow to Labs, not the DAO.

- Or clearly define a revenue-sharing ratio between the DAO and Labs.

- Establish a transparent page on the Aave main website or Labs website providing clear information to help investors interested in the $AAVE token (especially institutions or funds) make judgments.

Although the DAO model is controversial, Aave DAO token holders are among the most active and vocal groups, demonstrating the community's vitality. The frontend, website, and application are focal points of controversy, where "each sticks to their own argument" situations easily arise, lacking clear definition.

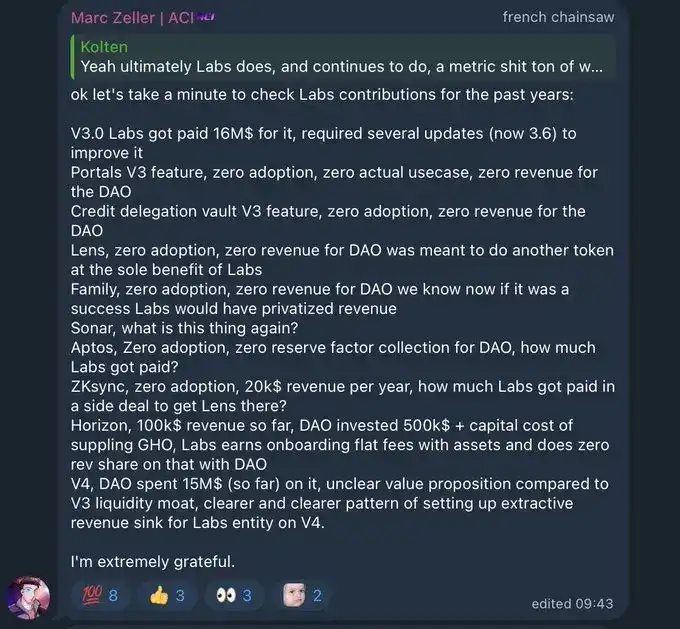

Some of Zeller's accusations against Labs for extracting protocol value:

The listed projects (Portals, Credit Delegation Vault, Lens, etc.) indeed indicate that many of Aave Labs' exploratory initiatives have not directly translated into protocol revenue or significant adoption rates.

It also mentions the V4 version. The DAO has spent $15 million so far. Compared to the liquidity moat of V3, the value proposition is unclear, raising concerns about whether this is a new trap for extracting revenue.

Failure is inevitable in the process of innovation. Not every feature or product can succeed. The DAO is, to some extent, investing in Aave Labs' R&D capability. My understanding is that Zeller is not否定 the contribution but calling for higher standards of accountability, transparency, and value alignment.

Recommended Reading:

Why Isn't Asia's Largest Bitcoin Treasury Company Metaplanet Buying the Dip?

Multicoin Capital: The Era of FinTech 4.0 Has Arrived

a16z's Heavily Funded Web3 Unicorn Farcaster Forced to Pivot, Is Web3 Social a False Proposition?