This past weekend, the two leading lending protocols on Solana, Jupiter Lend and Kamino, got into a public spat.

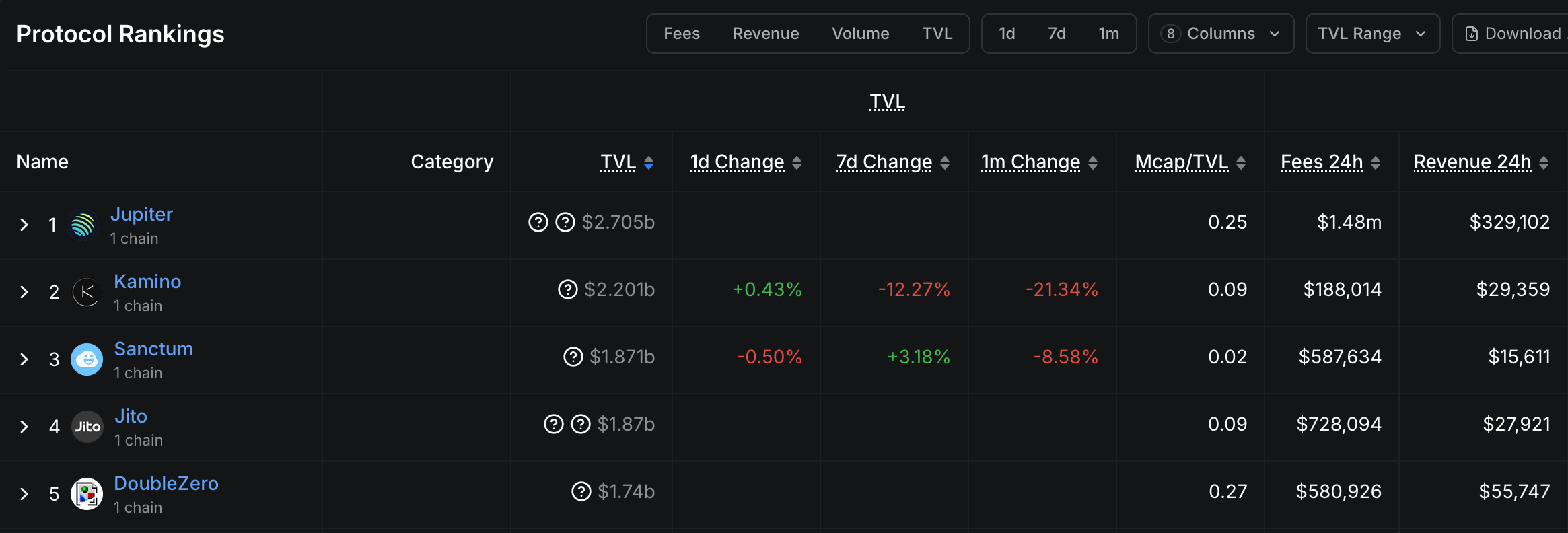

- Odaily Note: Defillama data shows that Jupiter and Kamino are currently the two protocols with the highest TVL in the Solana ecosystem.

Origin of the Incident: The Tweet Jupiter Quietly Deleted

The origin of the incident can be traced back to August of this year. During the promotional phase before the launch of its lending product, Jupiter Lend, the official Jupiter account repeatedly emphasized that the product featured "risk isolation" (related posts have been deleted), meaning risks would not cross-contaminate between different lending pools.

However, the final design of Jupiter Lend did not align with the market's common understanding of a risk isolation model. In the general market view, a DeFi lending pool that can be called risk-isolated is one that uses design mechanisms to segregate risks between different assets or markets, preventing a single asset default or a market crash from affecting the entire protocol. The main features of this structure include:

- Pool Segregation: Different asset types (such as stablecoins, volatile assets, NFT collateral, etc.) are allocated to independent lending pools, each with its own liquidity, debt, and risk parameters.

- Collateral Isolation: Users can only use assets within the same pool as collateral to borrow other assets, cutting off cross-pool risk transmission.

But in fact, Jupiter Lend's design supports rehypothecation (reusing deposited collateral elsewhere in the protocol) to improve capital efficiency, meaning the collateral deposited into the vaults is not completely isolated from each other. Jupiter co-founder Samyak Jain's explanation for this was that Jupiter Lend's lending pools are isolated "in a sense" because each pool has its own configuration, caps, liquidation thresholds, liquidation penalties, etc., and the rehypothecation mechanism is merely to better optimize capital utilization efficiency.

Although Jupiter's product documentation for Jupiter Lend contains more detailed explanations than the promotional content, objectively speaking, the "risk isolation" mentioned in its early promotions did have a certain deviation from the market's common understanding, creating a suspicion of misleading users.

Escalation: Kamino Launches an Attack

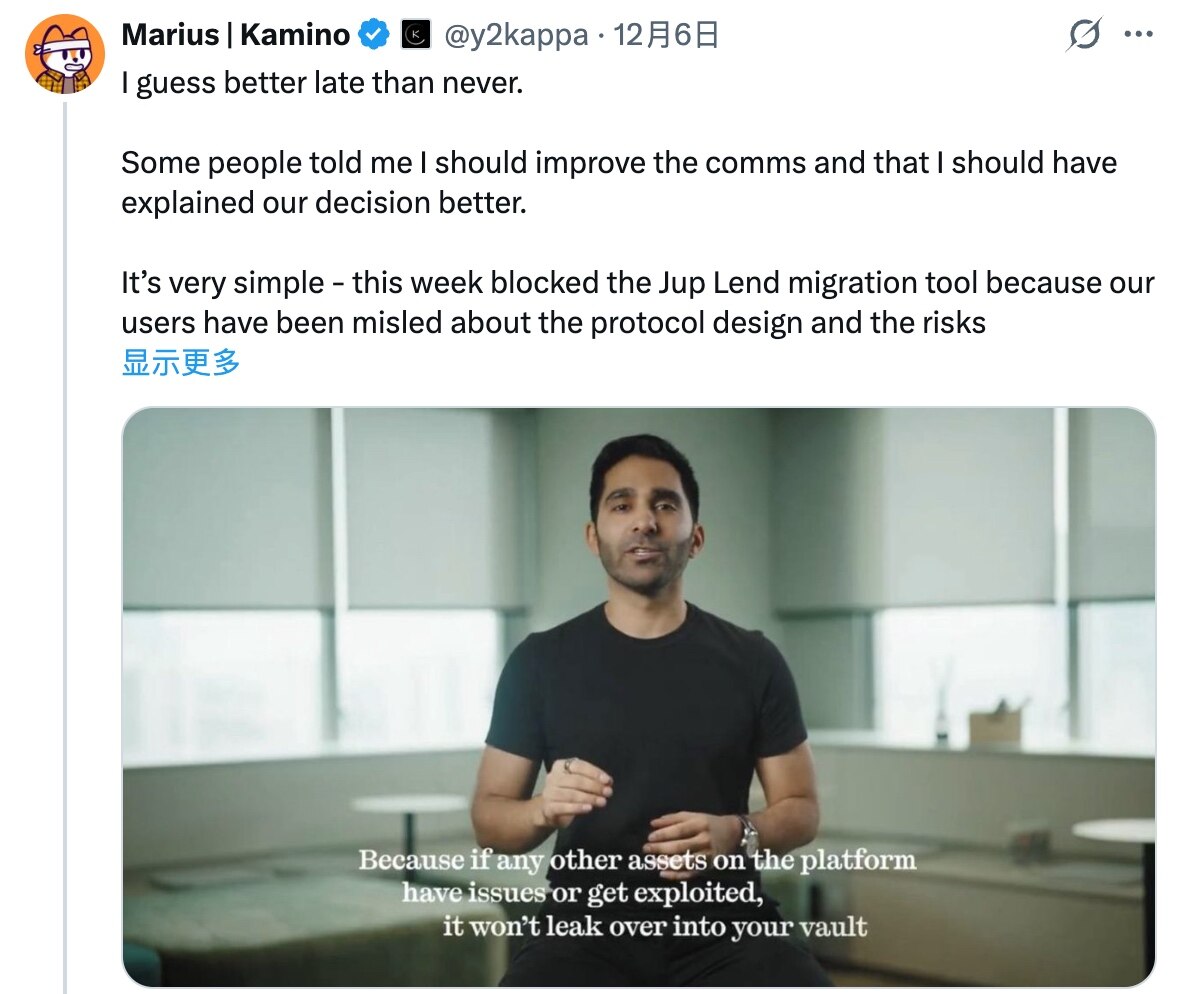

On December 6th, Kamino co-founder Marius Ciubotariu seized this opportunity to publish a post criticizing Jupiter Lend and blocked Kamino's migration tool to Jupiter Lend.

Marius stated: "Jupiter Lend repeatedly claims there is no cross-contamination between assets, which is complete nonsense. In reality, in Jupiter Lend, if you deposit SOL and borrow USDC, your SOL will be lent out to other users engaging in recursive farming using JupSOL, INF, etc. You bear all the risk of these recursive farms blowing up or the assets collapsing. There is no isolation here, there is complete cross-contamination, contrary to what was advertised and what people were told... In both traditional finance (TradFi) and decentralized finance (DeFi), information about whether collateral is rehypothecated and whether there is contagion risk is material information that must be clearly disclosed, and no one should offer vague explanations for it."

After Kamino's offensive, discussions surrounding Jupiter Lend's product design quickly ignited the community. Some agreed that Jupiter was涉嫌虚假宣传 (suspected of false advertising) — for example, Penis Ventures CEO 8bitpenis.sol angrily accused Jupiter of blatantly lying and deceiving users from the start; others believed that Jupiter Lend's design model balanced safety and efficiency, and that Kamino's attack was merely for market competition with impure motives — for example, overseas KOL letsgetonchain stated: "Jupiter Lend's design achieves the capital efficiency of a pooled model while incorporating some risk management capabilities of modular lending protocols... Kamino cannot stop people from migrating to better technology."

Under pressure, the Jupiter team quietly deleted the early posts, but this triggered a larger wave of FUD. Subsequently, Jupiter Chief Operating Officer Kash Dhanda also came forward to admit that the team's previous social media claims about Jupiter Lend having "zero contagion risk" were inaccurate and apologized, stating that a correction should have been issued simultaneously with the deletion of the posts.

Core Contradiction: The Definition of "Risk Isolation"

Summarizing the current opposing attitudes within the community, the fundamental divergence seems to lie in the different definitions different groups have for the term "risk isolation".

From the perspective of Jupiter and its supporters, "risk isolation" is not a completely static concept; there can be some design flexibility within it. Although Jupiter Lend is not the commonly understood risk isolation model, it also does not belong to a completely open pooled model. While it shares a common liquidity layer that allows rehypothecation, each lending pool can be configured independently, with its own asset caps, liquidation thresholds, and liquidation penalties.

From the perspective of Kamino and its supporters, any allowance of rehypothecation is a complete negation of "risk isolation", and as projects, they should not use vague disclosures and false advertising to deceive users.

Upper Echelon Sentiment: Some Fuel the Fire, Others Mediate

Apart from the dispute between the two parties and the community, another noteworthy point in this turmoil is the attitude of various upper echelon entities within the Solana ecosystem.

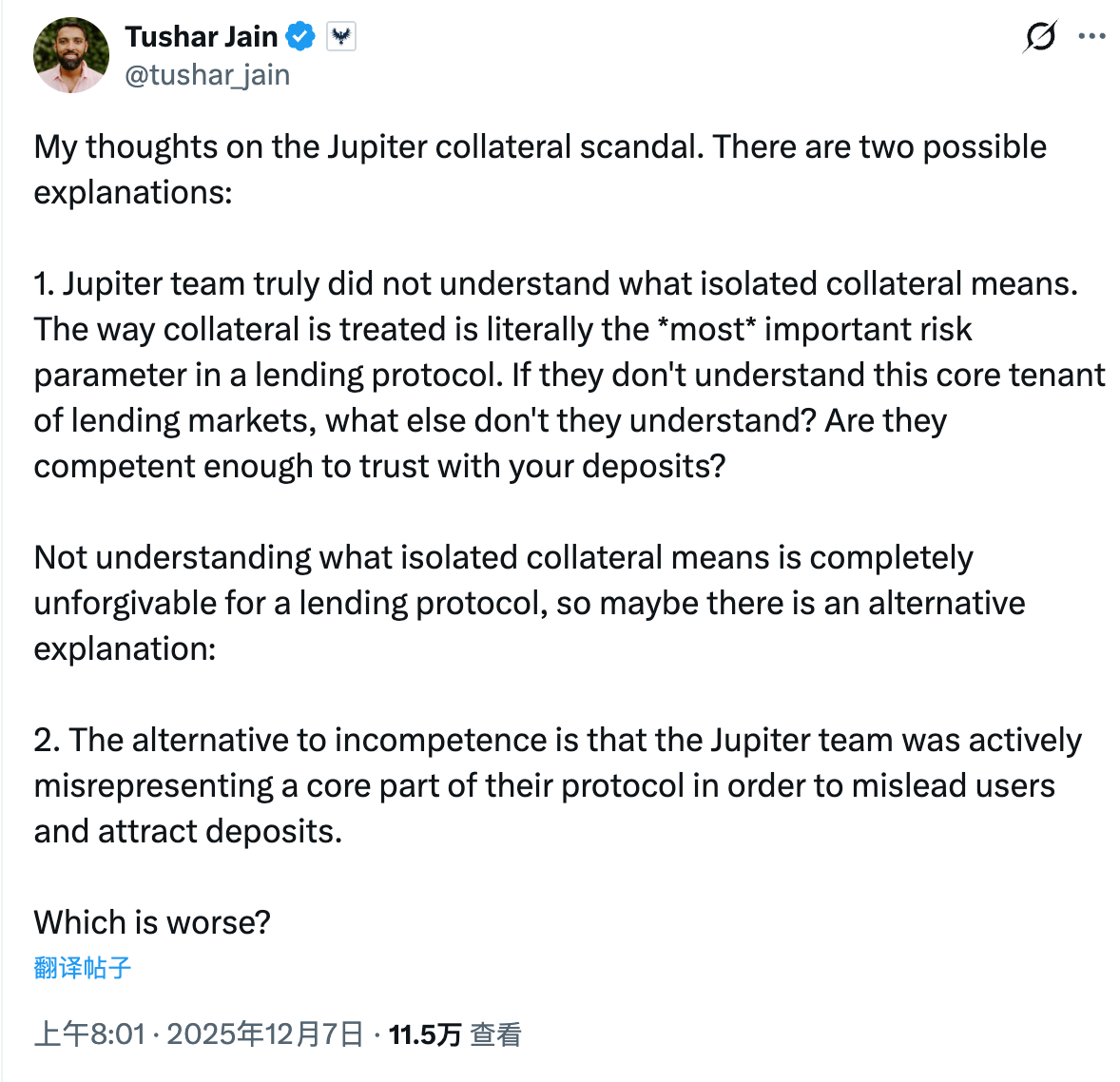

First is the venture capital fund Multicoin, which holds significant influence (perhaps the most) within the Solana ecosystem. As an investor in Kamino, Multicoin partner Tushar Jain directly posted questioning whether Jupiter was "incompetent or malicious, but neither possibility is forgivable" — objectively speaking, his remarks significantly intensified the turmoil.

Tushar stated: "There are two possible explanations for the controversy around Jupiter Lend. One is that the Jupiter team genuinely does not understand what isolated collateral means. Collateral treatment is the most important risk parameter in a lending protocol. If they don't understand this core principle of lending markets, what else have they not figured out? Is their expertise sufficient to make people feel comfortable depositing funds? For a lending protocol, not understanding the meaning of isolated collateral is completely unforgivable. The other possibility is that the Jupiter team is not incompetent but is actively misrepresenting the core parts of its protocol to mislead users and attract deposits."

Clearly, Tushar's motive is very clear: to seize this opportunity to help Kamino打击竞争对手 (strike a blow against its competitor).

Another important upper echelon statement came from the Solana Foundation. As the parent ecosystem, Solana obviously does not want to see its two leading contenders excessively opposed, leading to internal consumption within the ecosystem.

Yesterday afternoon, Solana Foundation President Lily Liu posted on X addressing both projects and mediating: "Love you both. Overall, our lending market size is currently around $5 billion, while the Ethereum ecosystem's size is about 10 times that. As for the traditional finance collateral market, it's countless times larger than that number. We can choose to attack each other, or we can choose to set our sights further — first work together to capture share from the entire crypto market, and then advance together into the vast world of traditional finance.

Simple summary — Stop arguing, or Ethereum will benefit!

Underlying Logic: The Battle for Solana's Lending Supremacy

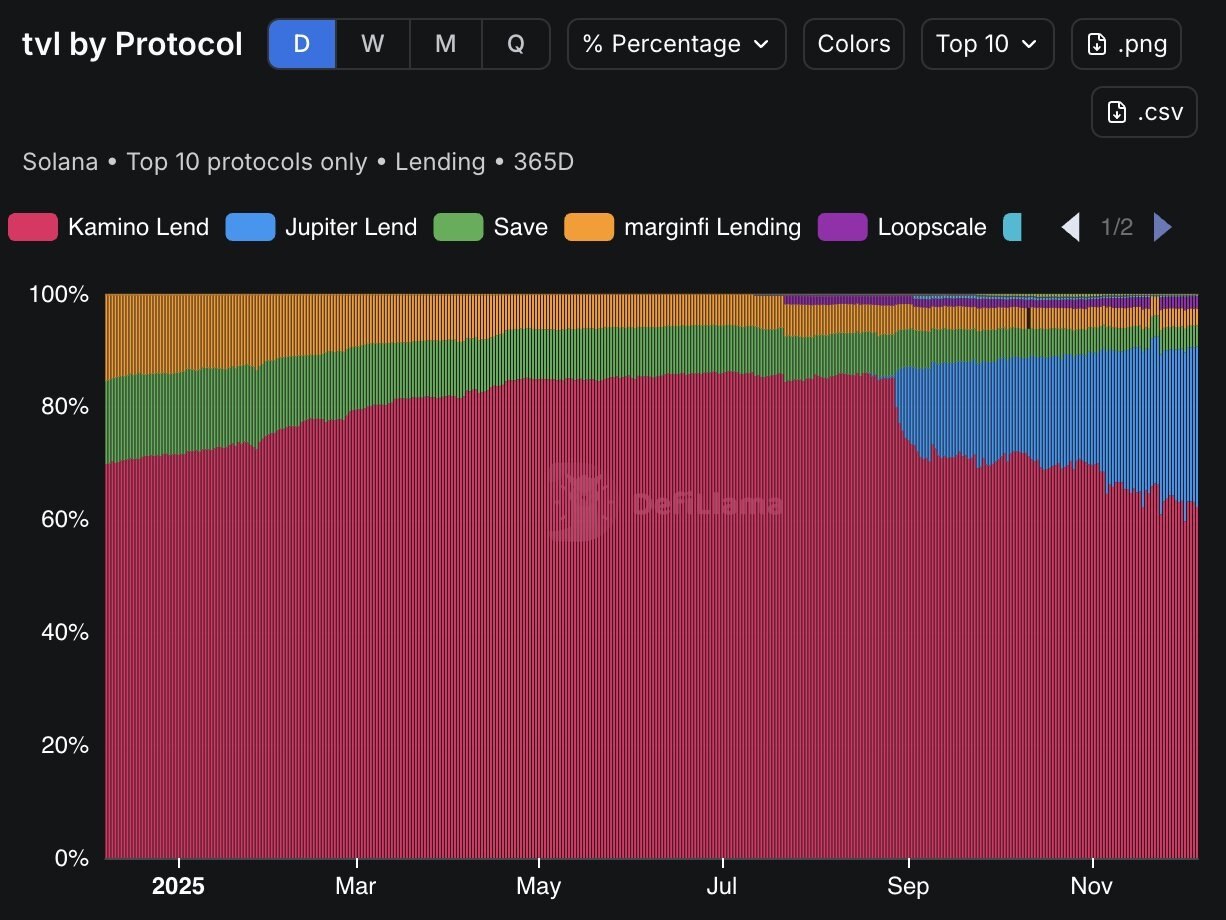

Looking at the data development of Jupiter Lend and Kamino and the market environment, although this turmoil arose suddenly, it seems like an inevitable collision that was only a matter of time.

On one hand, Kamino (red in the chart below) long held the position of the leading lending protocol on Solana, but Jupiter Lend (blue in the chart below) has captured a significant market share since its launch, becoming the only entity currently challenging the former within the Solana ecosystem.

On the other hand, since the major bloodbath on October 11th, market liquidity has tightened significantly, and the overall TVL of the Solana ecosystem has continued to decline; additionally, the subsequent blow-ups of multiple projects have made the DeFi market extremely sensitive to "safety".

When the market was better and incremental funds were sufficient, Jupiter Lend and Kamino were relatively harmonious, as there was profit to be made, and it seemed like it would only increase... But when the market turned into a存量博弈 (stock game), the competitive relationship between the two became more tense, and security issues正好又是当下最有效的进攻切口 (happen to be the most effective point of attack at the moment) — even though Jupiter Lend has not had any security incidents historically, mere design suspicions are enough to trigger user vigilance.

Perhaps in Kamino's view, now is the perfect opportunity to deal a heavy blow to its opponent.