Author| Max Wong @IOSG

Introduction

Pump.fun launched in early 2024 as a permissionless Meme Launchpad on Solana, allowing anyone to create and trade tokens within seconds via a Bonding Curve mechanism. Starting as a niche experiment, it quickly became one of the highest-revenue-generating applications on any public blockchain.

From 2024 to 2025, Pump.fun's daily protocol revenue consistently matched or even surpassed Hyperliquid's, a notable feat given the Meme market's inherent strong cyclicality. The native token $PUMP was issued via a $600 million ICO at $0.004, with an FDV of $4 billion.

Over the past few months, revenue hit all-time highs and the token's value doubled, but $PUMP's current price is around $0.0019, down approximately 80% from its all-time high of $0.086 (corresponding to an FDV of $8.6 billion). The current market cap is about $679 million, with an FDV of $1.9 billion. The gap between the revenue trend and valuation is evident.

This report examines Pump.fun's product evolution and ecosystem strategy, stress-tests whether its revenue is inflated, and determines if the current valuation is a pricing anomaly or a reasonable discount for real risks.

Product Portfolio

Pump.fun is no longer just a Launchpad. Since late 2024, it has expanded into adjacent businesses, broadening revenue streams and deepening its control over on-chain speculative activity.

Launchpad (Core Product)

The original product and the starting point of its brand identity. Anyone can deploy a token for a small fee.

PumpSwap

PumpSwap is Pump.fun's self-built AMM DEX, launched in March 2025, with a straightforward goal: recapture the graduation fees previously going to Raydium (Raydium charged 6 SOL per graduated token). After a fee update in May 2025, the protocol takes 0.05% from each trade, LPs get 0.20%, and token issuers get 0.05%.

Features include: creating liquidity pools for any token for free, adding liquidity to existing pools, and trading all tokens listed on PumpSwap.

Padre / Pump Terminal

Padre was acquired by Pump.fun and renamed Terminal, positioned as a professional trading terminal, currently supporting Solana, BNB, Base, and ETH.

Features are similar to other terminals: Trenches (view newly migrated/soon-to-migrate tokens), customizable interface, sniping and instant buys, multi-wallet strategies, bundle detector.

Pumplive

Pumplive is an in-platform live streaming feature where streamers can associate a token when creating a stream.

The logic is "the publisher is the exchange," similar to models of Parti and Kick/stake.com: streamers want to drive volume as they take a cut of the total fees; token holders want more volume and buying pressure. The more a streamer broadcasts, the more active the token, and the greater the trading volume.

Ecosystem Initiatives

Since TGE, with approximately $1 billion in cash reserves, Pump.fun has been continuously launching new product lines (the Padre acquisition is one example) while working on several initiatives:

Pumpfund

A $3 million BiP (Build in Public) hackathon launched on January 19, 2026. Based on a $10 million valuation benchmark, it provides $250,000 in grants to each of 12 projects. The selection criteria favor market-driven projects with public attention, not the conventional VC review process.

Glass Full Foundation

GFF is a liquidity injection program launched in August 2025. Through 5 transparent wallets, it deployed approximately $1.7 million (2,022 SOL) into 10 tokens (including Tokabu 21.3%, House 20.6%, USDUC, NEET, MASK, FART, etc.),筛选倾向 community participation.

Project Ascend

A creator incentive program launched in 2025,核心是 dynamic tiered creator fees (0.95% to 0.05%), aiming to increase creator earnings 10x while accelerating the CTO (Community Takeover) application process.

Comprehensive Metrics (All Products)

The table below aggregates the three product lines. 2025 is actual data, 2026 is the expected run rate.

Currently, about 32.7% of total revenue comes from non-Launchpad products, indicating initial success in diversifying revenue sources.

Currently, about 32.7% of the platform's total revenue comes from non-Launchpad products, clearly indicating initial success in its goal of diversifying revenue sources and seeking growth in other areas.

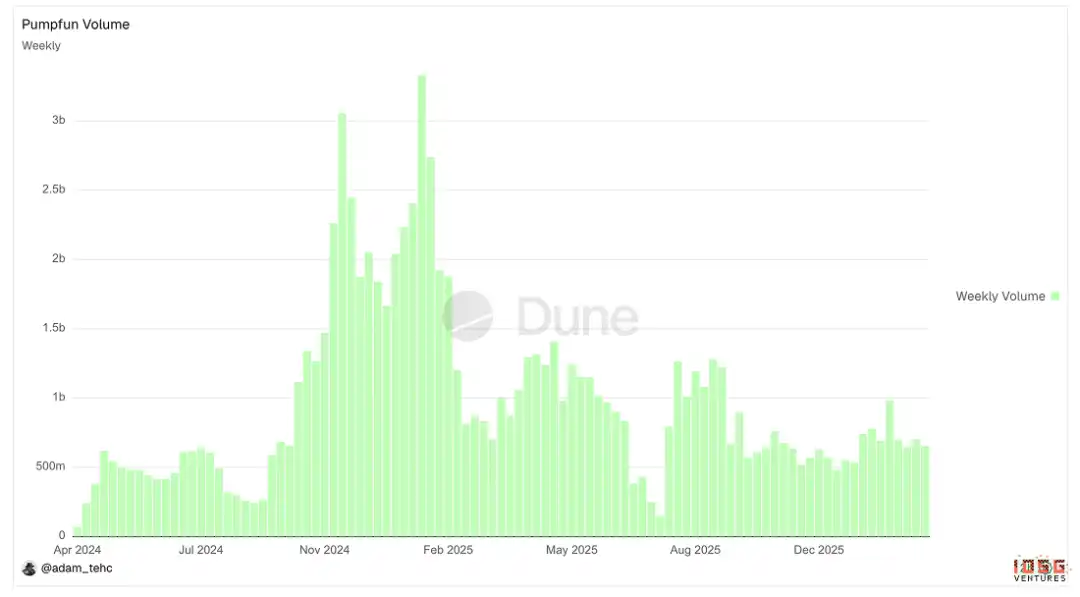

▲ Pumpfun Trading Volume Chart

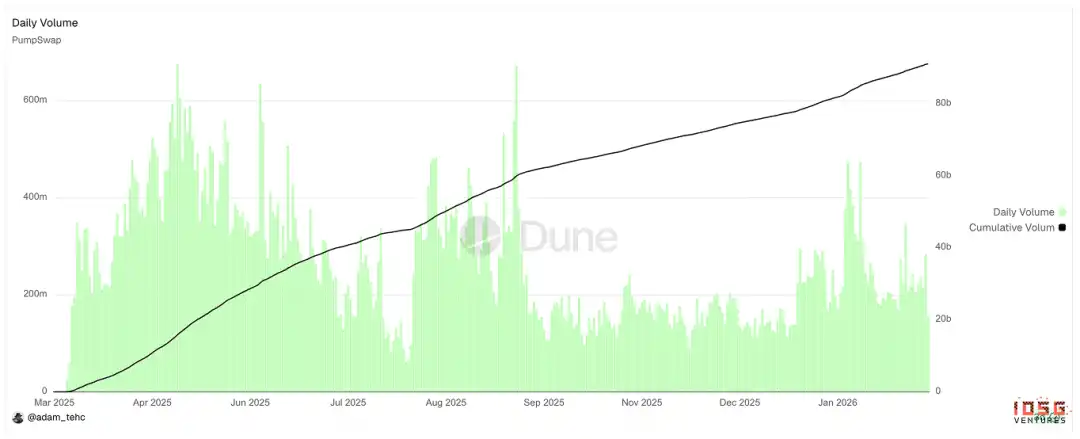

▲ Pumpswap Trading Volume Chart

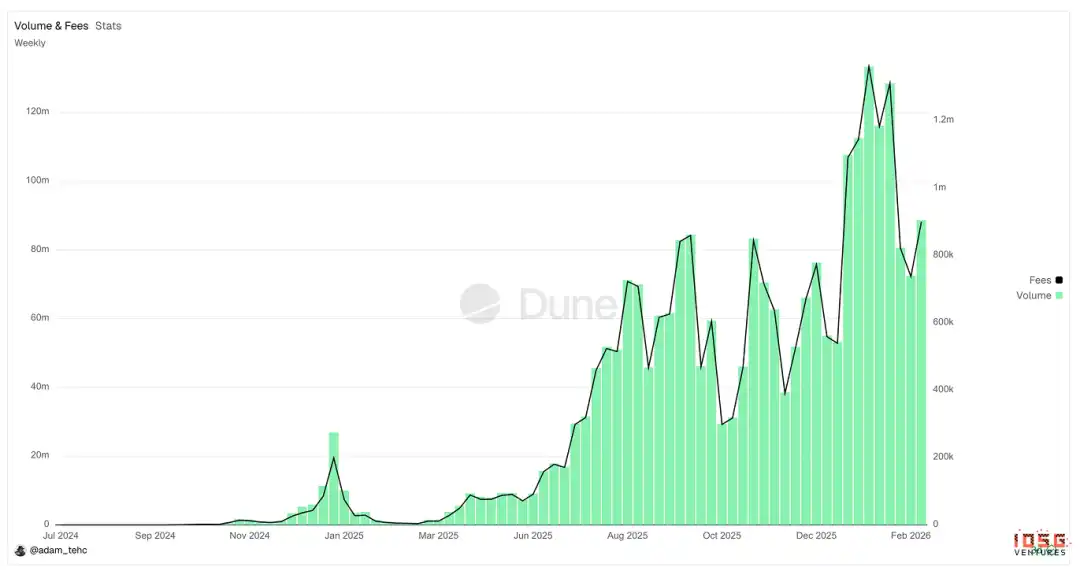

▲ Padre/Pump Terminal Trading Volume Chart

Does Pump.fun Have Wash Trading?

$PUMP's surface-level metrics look strong, but the core question is: does the trading volume reflect real economic activity, or is it inflated by users and bots?

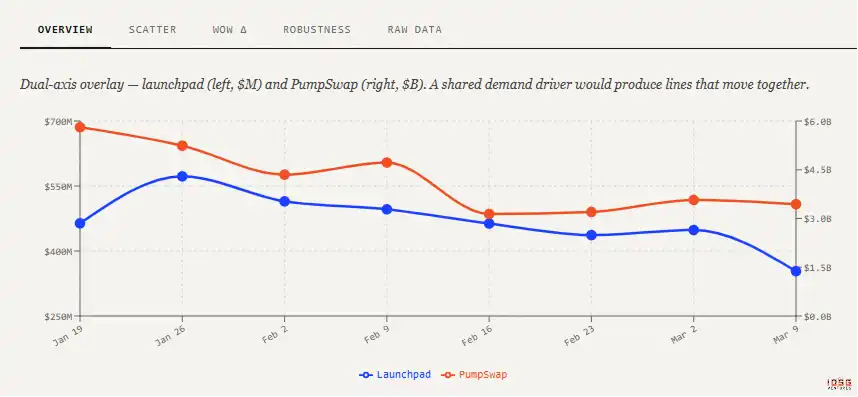

Trading Volume Correlation Analysis

The logic is simple: in a natural market, Launchpad and PumpSwap volumes should be positively correlated with a time lag. High Launchpad activity signifies genuine speculative interest, with some funds flowing into PumpSwap via the graduation mechanism, supporting post-listing trading.

If significant wash trading exists, this relationship breaks. Launchpad volume is artificially inflated, tokens graduate based on fabricated curve activity, and enter PumpSwap with no real buyers. The result is a spike in Launchpad volume while PumpSwap volume stays flat or drops, correlation tending towards zero or negative.

The most telling combination of signals: a surge in graduation rate (more tokens artificially reaching the curve threshold), coupled with low and rapidly decaying trading volume per token on PumpSwap, and PumpSwap liquidity depth not growing in sync with the number of graduated tokens.

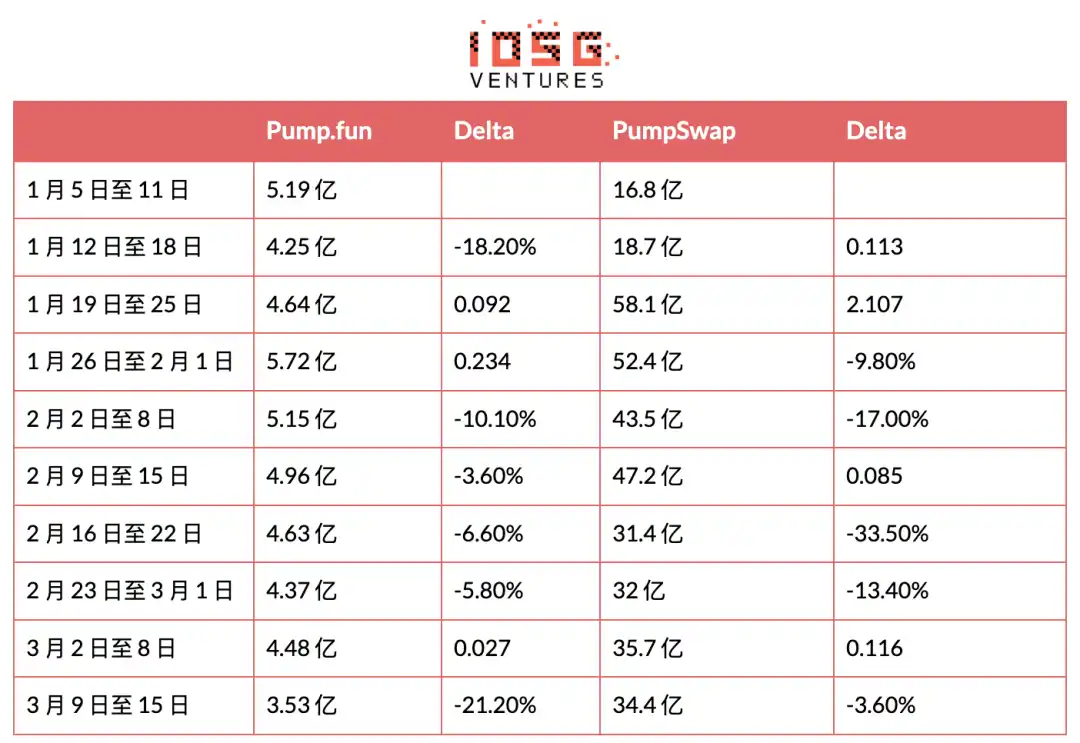

Data from January 2026 to present:

(The first two data points were excluded from correlation analysis due to anomalies caused by PumpSwap fee and market maker policy adjustments)

Findings:

Launchpad volume is stable, fluctuating between $400M and $570M over 8 weeks (~40% range). Given the large number of bundlers and wash traders maintaining a volume floor, this is unsurprising.

PumpSwap is more volatile, ranging from $3.5B to $5.8B in the same period (~60% range), primarily driven by a surge in Meme trading demand in mid-January and additional team incentives, but no corresponding increase was seen on Launchpad.

r = 0.579, moderate positive correlation. With a sample size n=8, p0.63, not reaching the significance threshold, but the direction and strength are consistent with the organic growth hypothesis.

University of Pisa Paper

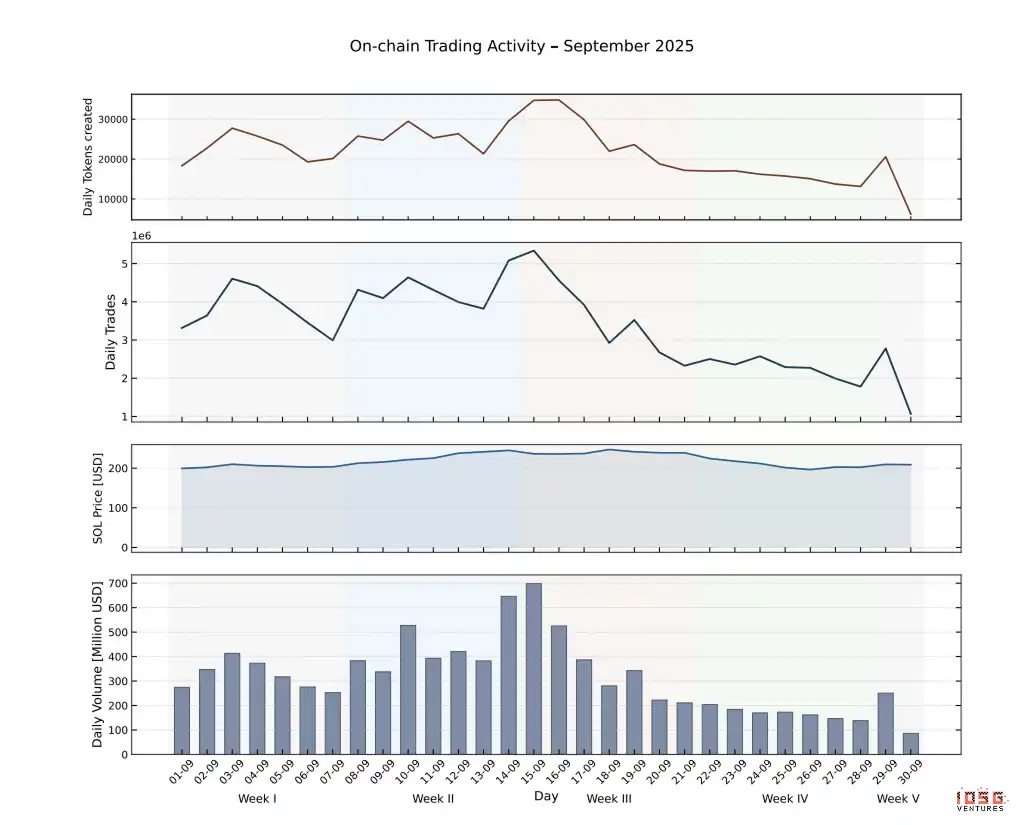

Researchers from the University of Pisa conducted a comprehensive on-chain analysis of the Pump.fun Launchpad, covering all transactions for 655,770 tokens issued between September and October 2025, distinguishing bot vs. human trades using Solana transaction log metadata.

Four findings directly address the fake trading issue.

Large Manual Buys Are the Strongest Predictor of Graduation

The strongest predictive signal for graduation is the rapid accumulation of SOL through a small number of large transactions. The median successful graduation requires only about 457 trades, taking about 4.4 minutes from token creation to graduation. This pattern (large, low-frequency capital injections from different wallets) is consistent with coordinated artificial speculation (Telegram group calls, KOL hype) or serial pump-and-dumps, not high-frequency wash trading bots. Conversely, bot-dominated tokens accumulate many small trades but stagnate before graduation.

Bot Activity Actually Suppresses Graduation

After the early curve stage, tokens with active bots had a systematically lower probability of graduation. The graduation requirement at the time was accumulating ~85 SOL in the curve. If bots were inflating volume to rush graduation, bot-active tokens should have a higher graduation rate, but the data shows the opposite.

The reason is structural: at graduation, the Bonding Curve transitions from a virtual reserve to a real AMM reserve, causing a discrete drop in effective liquidity depth. Selling before graduation (under the virtual reserve-supported depth) is more profitable than selling after.

The study also found that the top 10 token issuers in September 2025 each issued over 2,000 tokens in a single month. For each token, statistically anomalous selling sequences initiated by wallet clusters were observed before reaching the graduation threshold. Bundled traders and snipers accumulated positions early and sold into the retail demand attracted by the rising curve.

Paper Conclusion: Most bots on the platform are front-runners, extracting value from human counterparties upon entry and exit, not wash traders inflating the graduation threshold. Bots snipe/hoard large supplies, then dump to retail near graduation. This is different from wash trading.

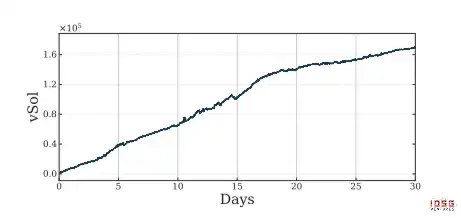

Sustained Positive SOL Net Flow, Structurally Incompatible with Wash Trading

The paper calculated the SOL net flow for the full dataset (total SOL used for the curve minus total SOL extracted from selling). During the one-month observation window, the ecosystem accumulated a net retention of approximately 160k SOL (~$32 million at September 2025 prices).

This is a hard test for wash trading: circular trading volume between related wallets would result in net capital flow near zero, as buys and sells cancel out. A net retention of $32 million is structurally incompatible with large-scale circular volume, indicating real external retail capital is continuously flowing into the Launchpad, paying the 1.25% fee per trade causing drain, funding protocol revenue.

The paper's findings align with our trading volume correlation analysis conclusion: a significant portion of Launchpad volume is generated by bundled traders and snipers through pump-and-dumps, creating a volume floor, but it is not wash trading. The distinction is crucial: wash trading generates zero net protocol revenue (fees cancel between related wallets), whereas pump-and-dumps generate real fees on every trade (from real retail counterparties paying the platform). The ~$390 million ARR confirms the platform monetizes real retail volume through a pump-and-dump ecosystem, not fabricating fake metrics.

Token Economics

Buybacks

The Pump Foundation currently uses 100% of the revenue from all product lines for open market buybacks of $PUMP. Since announcing the 100% revenue buyback on July 15, 2025, over 8 months:

27% of the circulating supply has been bought back, clearing 9.6% of the total supply.

Comparison: Hyperliquid has only destroyed 4.1% of its total supply (~12.3% of circulating supply) since initiating buybacks in November 2024.

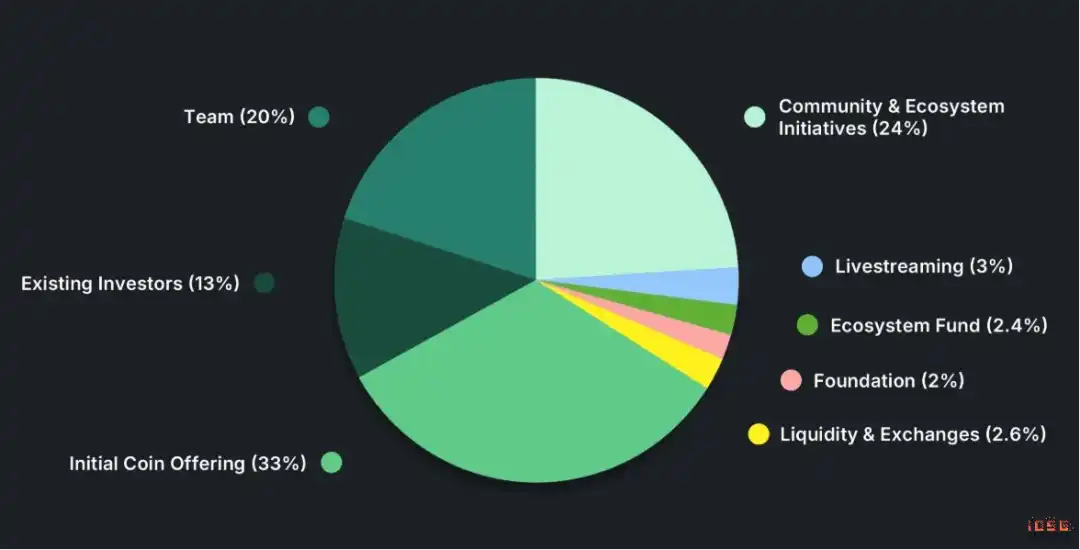

Supply Structure & Unlocks

Total Supply: 1,000,000,000,000 PUMP

Circulating Supply: 430,000,000,000 (43%)

The discount stems from three aspects:

#Market Skepticism About Revenue Sustainability

The market views Pump.fun's platform-wide volume as speculative, cyclical, and tied to short-term Meme activity. Investors treat current profitability as temporary. At the current P/E ratio, buybacks are financially accretive, but valuation models don't incorporate them because the underlying assumption is that revenue will compress significantly. The debate isn't whether Pump.fun is profitable now, but whether it will be in 24 months.

#Lack of Institutional Coverage

We interviewed 15 tier 1 secondary funds and VCs about their views on $PUMP. Only 1 out of 15 was actively tracking $PUMP using bottom-up analysis. Most institutions haven't modeled the new product suite, broken down revenue by product line, or stress-tested volume sustainability.

The lack of coverage creates a narrative vacuum, where pricing is driven more by market sentiment than financial analysis. In contrast, $HYPE has deeper institutional support, more research coverage, and a clearer product positioning, supporting a higher and more stable valuation multiple.

There's also a self-reinforcing effect: assets related to Meme infrastructure are default-categorized as speculative and transient, and trading behavior follows suit. The market needs time and data across multiple cycles to update this cognitive framework. Until Pump's revenue withstands a broader crypto market downturn and institutional coverage expands, valuation compression may persist, regardless of current cash flows.

#Management Trust Not Yet Established

Investor concerns focus on: long-term vision beyond Memes, capital allocation discipline, product roadmap execution, transition from viral growth to a sustainable platform economy.

Markets typically assign lower valuation multiples to founder-led, high-growth platforms until they demonstrate resilience through market volatility, proving growth can translate into a sustainable platform economy. This discount is likely to persist until Pump demonstrates continued revenue diversification and robust execution through products like PumpSwap and Pump Terminal.

Perguntas relacionadas

QWhat is the core argument presented in the IOSG report regarding Pump.fun's trading volume?![]()

AThe report argues that Pump.fun's trading volume is not primarily driven by wash trading but by real economic activity, specifically 'pump and dump' schemes orchestrated by bundlers and snipers. This is supported by a positive correlation between Launchpad and PumpSwap volumes and a university study showing a net positive SOL capital inflow, which is structurally incompatible with wash trading.

QAccording to the analysis, what are the three main sources of the discount in $PUMP's valuation?![]()

AThe three main sources of the valuation discount are: 1. Market skepticism about the sustainability of its meme-driven, cyclical revenue. 2. A lack of institutional coverage and research, leading to a narrative vacuum. 3. Investor concerns about long-term vision, capital allocation, and the need to build trust in management's ability to transition to a sustainable platform economy.

QWhat key finding from the University of Pisa study contradicts the 'wash trading' narrative?![]()

AA key finding was that the ecosystem had a net capital inflow of approximately 16,000 SOL (worth ~$32 million at the time) over the observed period. Since wash trading between related wallets would result in a net flow close to zero, this substantial positive inflow is structurally incompatible with large-scale circular trading and indicates real external retail capital is flowing into the platform.

QHow does Pump.fun's revenue share buyback program compare to Hyperliquid's?![]()

APump.fun's program has been more aggressive. In the 8 months since its 100% revenue share buyback began, it has repurchased 27% of the circulating supply, clearing 9.6% of the total token supply. In contrast, Hyperliquid has only burned 4.1% of its total supply (approx. 12.3% of circulating) since its buyback started.

QWhat is the purpose of Pump.fun's expansion into products like PumpSwap and Pump Terminal?![]()

AThe expansion aims to diversify revenue sources and deepen control over on-chain speculative traffic. PumpSwap recaptures fees that were previously paid to external DEXs like Raydium when tokens 'graduate'. Pump Terminal (acquired from Padre) serves as a professional trading terminal to capture more of the trading activity and fees across multiple chains.