On December 10, 2025, local time, the Federal Reserve lowered the benchmark interest rate by 25 basis points to 3.50%-3.75% in a 9-3 vote, marking the third consecutive meeting with a rate cut. The policy statement removed the description of the unemployment rate as "low." The latest dot plot maintains the forecast of a 25 basis point rate cut in 2026.

Additionally, the Federal Reserve will purchase $40 billion in Treasury bills within 30 days starting December 12 to maintain ample reserve supply.

Full Text of the Interest Rate Decision

Available data indicate that economic activity is expanding at a moderate pace. Job growth has slowed this year, and the unemployment rate has risen as of September. More recent indicators are consistent with this situation. Inflation has increased compared to the beginning of the year and remains elevated.

The Committee's long-term goals are to achieve maximum employment and 2% inflation. Uncertainty about the economic outlook remains high. The Committee is closely monitoring risks on both sides of its dual mandate and believes that downside risks in employment have increased in recent months.

To support these goals and considering changes in the risk balance, the Committee decided to lower the target range for the federal funds rate by 25 basis points to 3.50% to 3.75%. In assessing the appropriate timing and magnitude of any further adjustments to the target range for the federal funds rate, the Committee will carefully evaluate incoming data, the evolving economic outlook, and the balance of risks. The Committee is strongly committed to supporting maximum employment and returning inflation to its 2% target.

In evaluating the appropriate monetary policy stance, the Committee will continue to monitor the implications of incoming information for the economic outlook. The Committee would be prepared to adjust the stance of monetary policy as appropriate if risks emerge that could impede the attainment of the Committee's goals. The Committee's assessments will take into account a wide range of information, including labor market conditions, inflationary pressures and inflation expectations, and financial and international developments.

The Committee believes that reserve balances have declined to ample levels and will initiate purchases of short-term U.S. Treasury securities as needed to maintain ample reserve supply on an ongoing basis.

Voting in favor of this monetary policy action were: Chair Jerome H. Powell, Vice Chair John C. Williams, Michael S. Barr, Michelle W. Bowman, Susan M. Collins, Lisa D. Cook, Philip N. Jefferson, Alberto G. Musalem, and Christopher J. Waller. Voting against were Stephen I. Miran, who preferred to lower the target range for the federal funds rate by 1/2 percentage point at this meeting; and Austan D. Goolsbee and Jeffrey R. Schmid, who preferred to maintain the target range for the federal funds rate unchanged at this meeting.

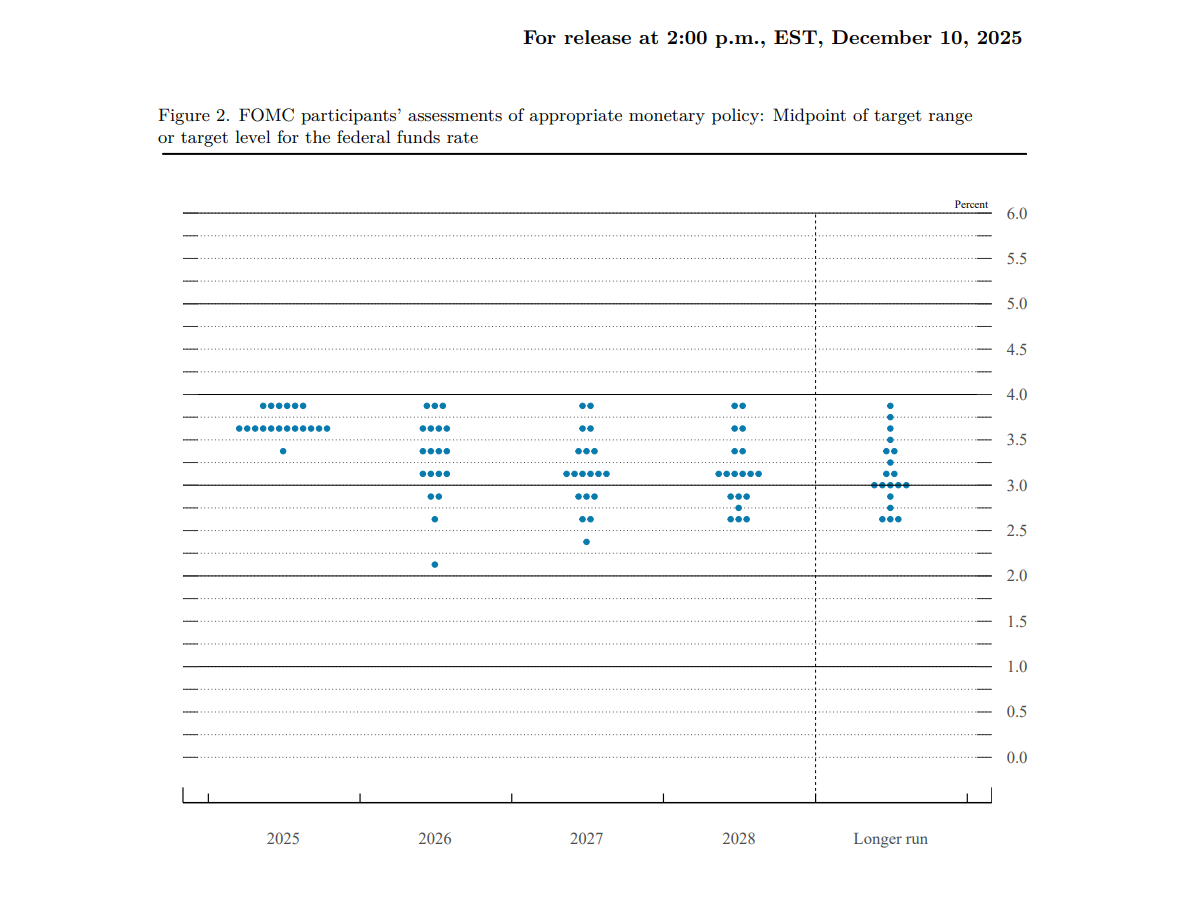

Median Fed Dot Plot: Cumulative 25 Basis Point Rate Cut in 2026

Decisions Regarding Monetary Policy Operations

To implement the monetary policy stance announced in the Federal Open Market Committee's statement on December 10, 2025, the Federal Reserve makes the following decisions:

The Board of Governors of the Federal Reserve System unanimously voted to lower the interest rate on reserve balances to 3.65%, effective December 11, 2025.

As part of the policy decision, the Federal Open Market Committee voted to direct the Open Market Trading Desk at the Federal Reserve Bank of New York, until further notice, to execute transactions in the System Open Market Account in accordance with the following domestic policy directive:

"Effective December 11, 2025, the Federal Open Market Committee directs the Desk:

To conduct open market operations as necessary to maintain the federal funds rate in a target range of 3.50% to 3.75%.

To conduct standing overnight repurchase agreement operations at an offering rate of 3.75%.

To conduct standing overnight reverse repurchase agreement operations at an offering rate of 3.50%, with a per-counterparty limit of $160 billion per day.

To increase the System Open Market Account's holdings of securities by purchasing Treasury bills and, if necessary, other U.S. Treasury securities with remaining maturities of three years or less, to maintain ample levels of reserves.

To reinvest all principal payments from the Federal Reserve's holdings of U.S. Treasury securities at auction. To roll over all principal payments from the Federal Reserve's holdings of agency securities into Treasury bills."

In related actions, the Board of Governors of the Federal Reserve System unanimously voted to approve a 25 basis point reduction in the primary credit rate to 3.75%, effective December 11, 2025. In taking this action, the Board approved requests submitted by the Boards of Directors of the Federal Reserve Banks of New York, Philadelphia, St. Louis, and San Francisco to set this rate.

Twitter:https://twitter.com/BitpushNewsCN

Bitpush TG Discussion Group:https://t.me/BitPushCommunity

Bitpush TG Subscription: https://t.me/bitpush