Written by: Coinbase

Compiled by: Chopper, Foresight News

For decades, the path to wealth accumulation for Americans has remained almost unchanged: find a good job, buy property, invest in stocks, and wait for the power of compound interest to yield returns. However, our latest "Cryptocurrency Industry Report" shows that the younger generation of investors no longer believes in this traditional path and is adjusting their investment behavior accordingly.

To understand how different generations respond to the market and the role cryptocurrency plays in their investment portfolios, Coinbase partnered with Ipsos to conduct a specialized survey. A total of 4,350 American adults were interviewed, including 2,005 investors with investment accounts. The core findings of the survey are as follows: younger investors, such as Gen Z and Millennials, are more inclined to actively manage their investments, more open to non-traditional assets, and more likely to view cryptocurrency as a core component of their financial future than any previous generation.

A Generation Shut Out of the Traditional Wealth Ladder

Younger investors are far more optimistic about the economy than older generations, but they believe the existing financial system is not designed for them. Survey data shows that nearly seven out of ten (73%) young people believe it is more difficult for their generation to accumulate wealth through traditional means compared to their parents' generation. In contrast, only 57% of older generations share this view.

They have witnessed soaring housing costs, overwhelming student debt, and sluggish wage growth. In this context, more and more young people are seeking alternative ways to accumulate wealth beyond the traditional model of "home equity + stock portfolio."

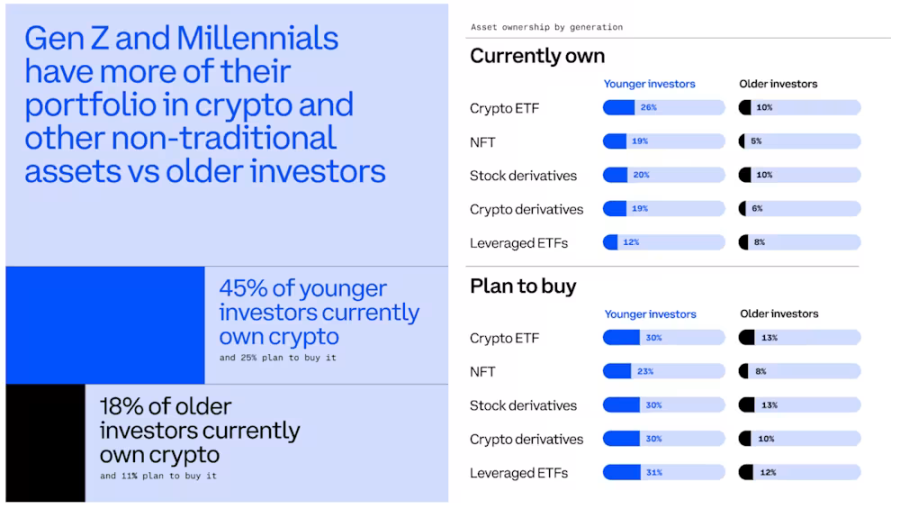

Non-Traditional Asset Allocation Three Times Higher Than Older Generations

This anxiety is directly reflected in their asset allocation strategies. The survey shows that younger investors allocate 25% of their portfolios to non-traditional asset classes such as cryptocurrencies, financial derivatives, non-fungible tokens (NFTs), and other emerging products. This is three times the proportion allocated by older investors, who only allocate 8% to non-traditional assets.

The proportion of stock holdings is roughly similar across generations, but the key difference lies in the fact that younger investors diversify their portfolios beyond stocks. They are more actively seeking opportunities for returns beyond traditional stock dividends and are more willing to experiment with new investment tools and emerging markets to narrow the wealth gap.

Cryptocurrency Is Not a Side Investment but a Core Allocation

This generational shift in investment philosophy is most evident in the acceptance of cryptocurrency. The report shows that 45% of younger investors already hold cryptocurrency, compared to only 18% of older investors. Additionally, nearly half (47%) of younger investors want to gain exposure to new crypto assets before the general market, while only 16% of older investors share this desire.

In the eyes of the younger generation, cryptocurrency is not merely a form of speculative trading but an important tool to help them catch up in wealth accumulation. Eighty percent of young people believe that cryptocurrency provides their generation with more financial opportunities outside the traditional financial system. At the same time, another 80% are convinced that cryptocurrency will play a significantly larger role in the future financial system. Among older investors, only about 60% share this view.

The younger generation's enthusiasm for exploring emerging markets extends beyond spot cryptocurrencies; they are also eager to engage with more non-traditional assets. Data shows that 80% of younger investors are willing to try new investment opportunities ahead of others, while less than half of older generations share this attitude. Younger investors consistently show strong interest in emerging non-traditional products such as cryptocurrency derivatives, prediction markets, 24/7 stock trading, early token offerings, altcoins, and decentralized finance lending.

The Impact of This Trend on Future Markets

The younger generation of investors has already demonstrated distinct characteristics: they trade more frequently, are willing to take greater risks for higher returns, and are shifting a significant portion of their portfolios to non-traditional assets, with cryptocurrency at the core. At the same time, they are driving the entire financial industry toward a transformation that better meets the needs of the internet-native generation, creating platforms that operate around the clock and support diverse asset trading.