本轮熊市至今最大的疑问是比特币价格将于何时何地反弹。最新链上数据显示,当前熊市的价格底部或许有了新答案。

为何4万美元可能成为熊市关键点位

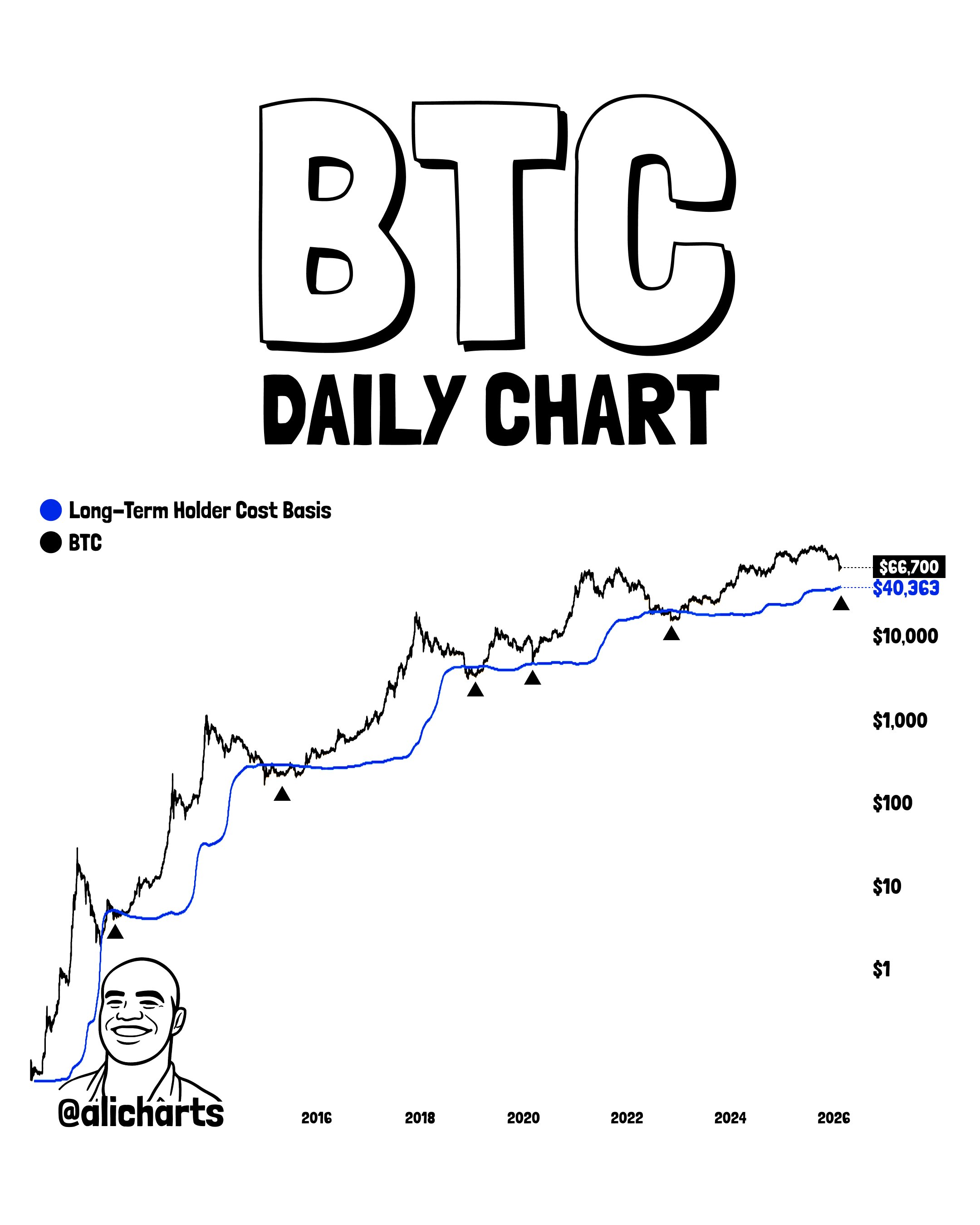

加密货币分析师阿里·马丁内斯在X平台最新发文中指出,4万美元关口可能成为比特币当前市场阶段的潜在底部。该预测基于被称为「长期持有者(LTH)」的资深投资者群体成本基础。

需要说明的是,长期持有者成本基础指的是持币155天以上的比特币投资者购入时的平均价格。该价格水平之所以重要,是因为长期投资者通常被视为「钻石手」,他们在下行波动期间抛售的可能性较低。

此外,长期持有者成本基础往往在熊市期间充当终极支撑位,因为即便在熊市最严峻时期,多数长期投资者通常仍处于盈利状态。因此当比特币价格跌至该支撑位时,长期持有者会加倍增持头寸。

来源:@ali_charts on X

如上图所示,长期持有者 renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity renewed buying activity 极的增持行为将支撑比特币价格维持在其成本基础之上。 highlighted data highlighted data highlighted data highlighted data highlighted data highlighted data highlighted data highlighted data highlighted data highlighted data highlighted data highlighted data highlighted data highlighted data highlighted data highlighted data highlighted data highlighted data highlighted data highlighted data highlighted data highlighted data highlighted data highlighted data highlighted data highlighted data highlighted data highlighted data highlighted data highlighted data highlighted data highlighted data highlighted data highlighted data highlighted data highlighted data highlighted data highlighted data highlighted data highlighted data highlighted data highlighted data highlighted data highlighted data highlighted data highlighted data highlighted极的增持行为将支撑比特币价格维持在其成本基础之上。据重点数据显示,当前LTH成本基础约为40,363美元,较现价低约40%。

若比特币价格面临进一步下行压力并逼近该成本基础,很可能获得长期投资者增持形成的支撑。因此该成本基础可能成为当前熊市的底部。

另一方面,若抛压压倒长期持有者的增持势头,比特币市场可能面临更大幅度的回调。

比特币价格概览

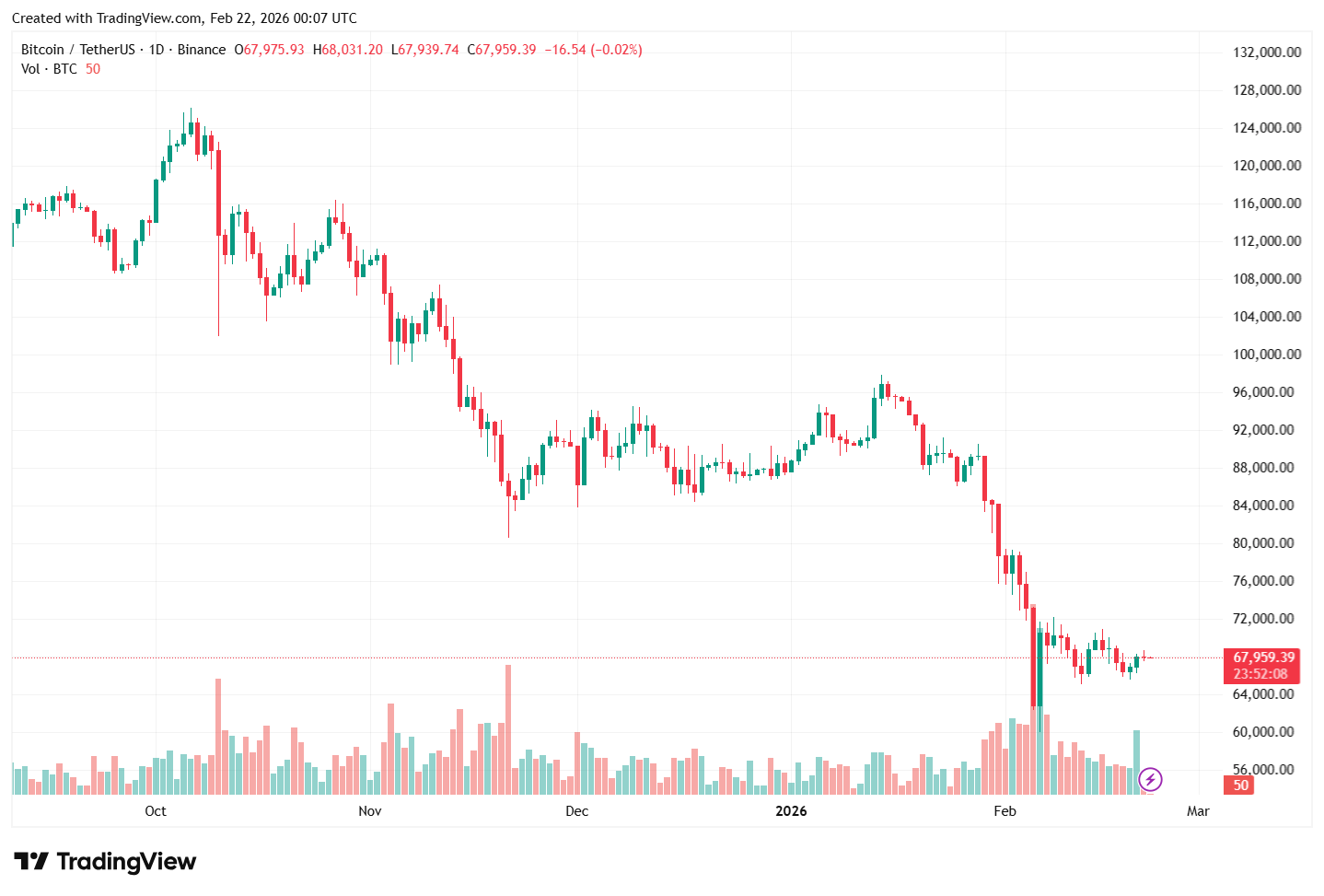

截至撰稿时,BTC价格报68,330美元,24小时内上涨近1%。但这一单日微动难以扭转龙头加密货币过去一周超2%的跌幅。CoinGecko数据显示,比特币当前价格较高点下跌逾45%。

每日时段BTC价格 | 来源:TradingView上的BTCUSDT图表