Author: Alex Immerman & Santiago Rodriguez

Compiled by: Deep Tide TechFlow

Deep Tide Introduction: a16z uses Revolut's 2025 annual report to dissect how a company achieved a 76% CAGR in a mature financial market. The numbers themselves are astonishing, but what's even more worth reading is the underlying growth logic: not relying on interest spreads for profit, an ROE 3-4 times that of traditional banks, and user NPS more than double the industry average. Put together, this is no longer just a challenger bank story.

Full Text Below:

As growth investors, we often say that great companies speak through their numbers. Revolut, as a UK company, is required to disclose annual financial data mandatorily. Its numbers are outliers, and that's an understatement:

Revenue grew 46% to £4.5 billion

Pre-tax profit grew 57% to £1.7 billion, with a 38% margin

Retail customers grew 30%, adding 16 million in 2025

Revolut has penetration across Europe, with no single country accounting for more than 25% of fee income

Revenue is distributed across 6 business segments, with no single category exceeding 22%

11 product lines each generated over £100 million in revenue

Return on Equity (ROE) reached 35%, a record-breaking level among peers (despite being over-capitalized)

Revolut continues to grow rapidly and efficiently—its "Rule of 75%" (revenue growth rate + net profit margin) places it in the highest tier among modern and mature financial institutions.

More importantly, we believe Revolut still has ample room for both customer growth and monetization in its existing markets. Not to mention potential new markets it hasn't even touched yet—Revolut just applied for a US banking license, showing true global ambition.

This is not your grandmother's neobank. Revolut has the potential to become one of the largest banks globally. There's still a long way to go to get there, but we believe the foundation is laid.

Enough said, let's get started.

I. One of the World's Fastest-Growing Financial Institutions

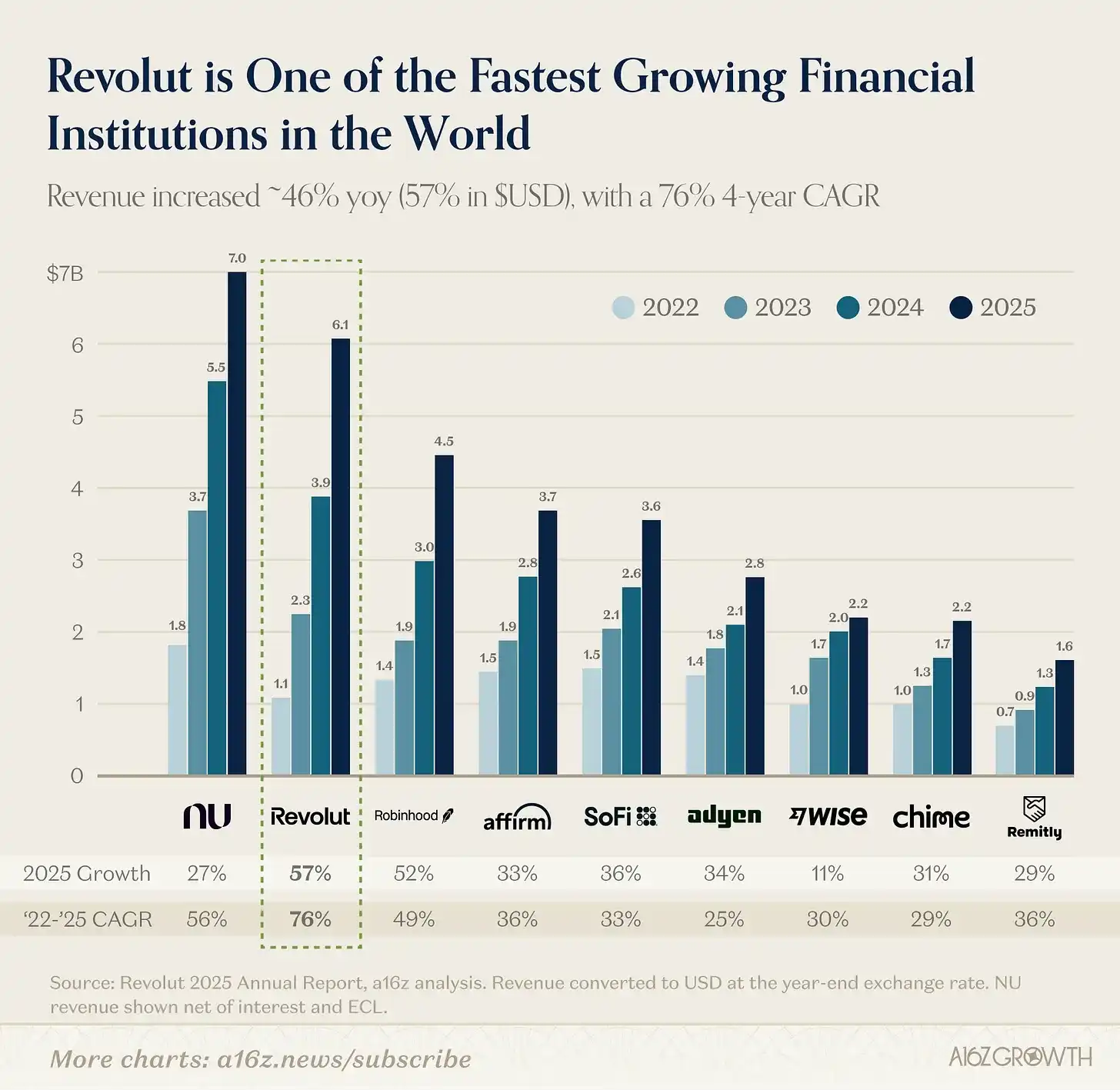

Let's start with revenue. Revolut's revenue growth is astounding.

Alongside NU (Nubank), they stand in a league of their own compared to other companies in the consumer fintech industry (see chart below). Since breaking the $1 billion revenue mark in 2022, Revolut has compounded at an astonishing 76% CAGR (70% in GBP terms) over the subsequent four years, making it one of the fastest-growing companies post the $1 billion revenue milestone. This growth is particularly notable given that Europe's consumer banking market is highly mature (unlike NU's emerging market).

Chart: Revenue converted to USD at year-end exchange rates. NU revenue is net of interest and expected credit losses (ECL).

Source: Revolut 2025 Annual Report

For perspective: In 2022, Revolut's revenue was either less than or similar to that of Robinhood, Affirm, Sofi, Adyen, Wise, or Chime. Now, its revenue is 33% to nearly 3 times greater than any of these well-known consumer fintech companies.

II. Deconstructing Revolut's Growth Algorithm: Six Horses Running Simultaneously

A key differentiator for Revolut is that it is no longer a one-trick pony. It has multiple revenue drivers firing at once.

Revolut started by addressing a real pain point for Europeans: foreign exchange fees. With Revolut, Europeans traveling within or outside the Eurozone, or sending money overseas, no longer had to face payment delays or the 5% fees charged by banks.

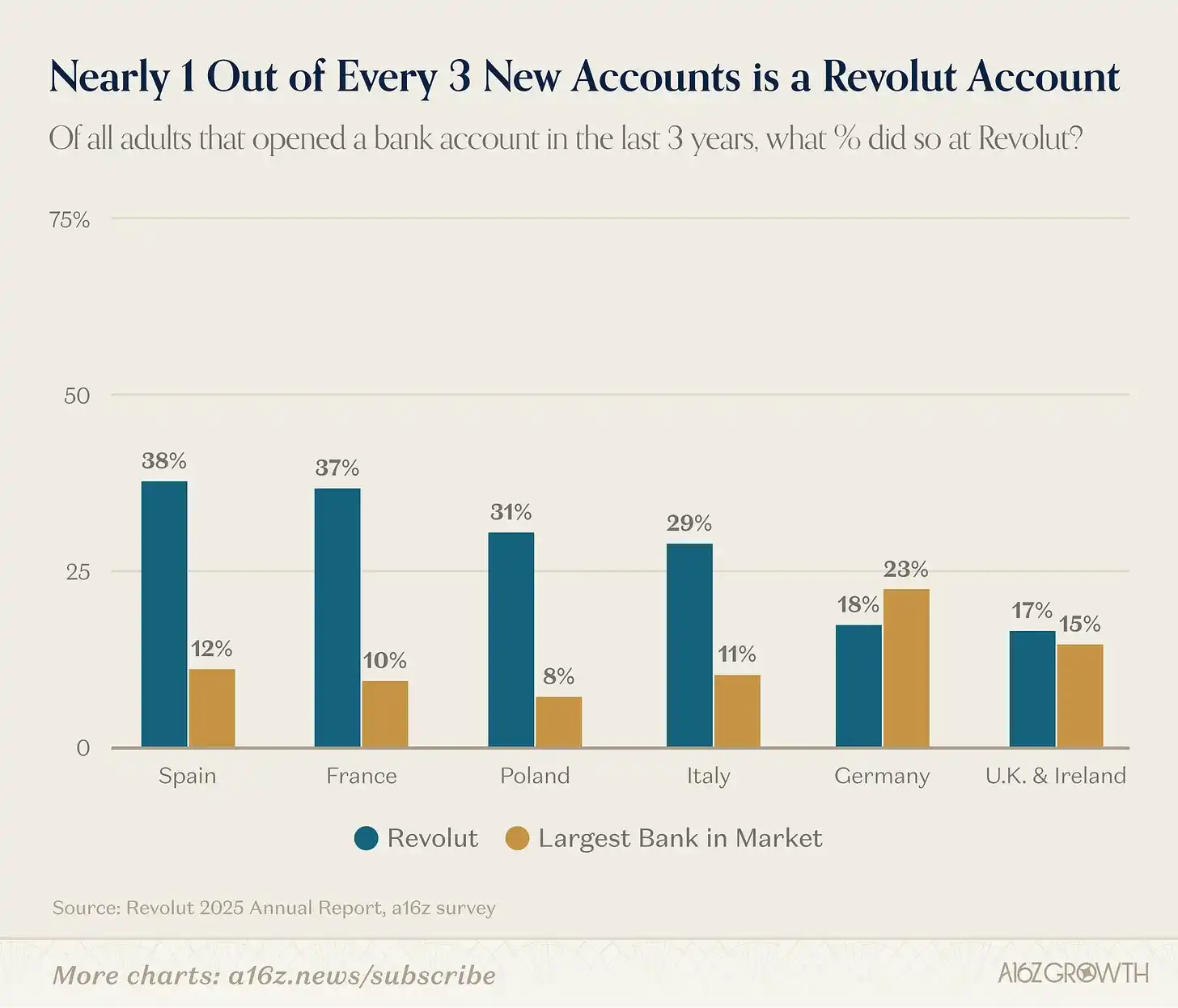

From a once single-product, geographically concentrated painkiller, Revolut has grown into a fully-featured personal and business bank. Now, approximately 1 in 3 new accounts opened in Europe (Revolut's primary operating region) chooses Revolut:

Chart: Survey conducted in key markets using a sample of the general adult population. Respondents indicated where they opened accounts and the timing of each account opening.

Source: a16z European Banking Survey, July 2025 (N = 3500)

1 in 5 working-age people in Europe use Revolut. Revolut's appeal across the diverse Eurozone markets demonstrates the company's exceptional product iteration speed and execution.

Revolut has launched a complete suite of personal and business banking features, driving growth across diverse European markets. Importantly, Revolut's product suite is increasingly attracting users within the Eurozone who are indifferent to the initial FX value proposition. We might say Revolut's platform is "feature complete," though that might be an understatement as Revolut keeps launching new features.

It's not just the quantity of features and products, but the quality of execution. Users love it. The company reported in 2024 that 65% of new users came through organic acquisition or referrals from existing users. Our research also shows that Revolut's user NPS is more than double the industry average.

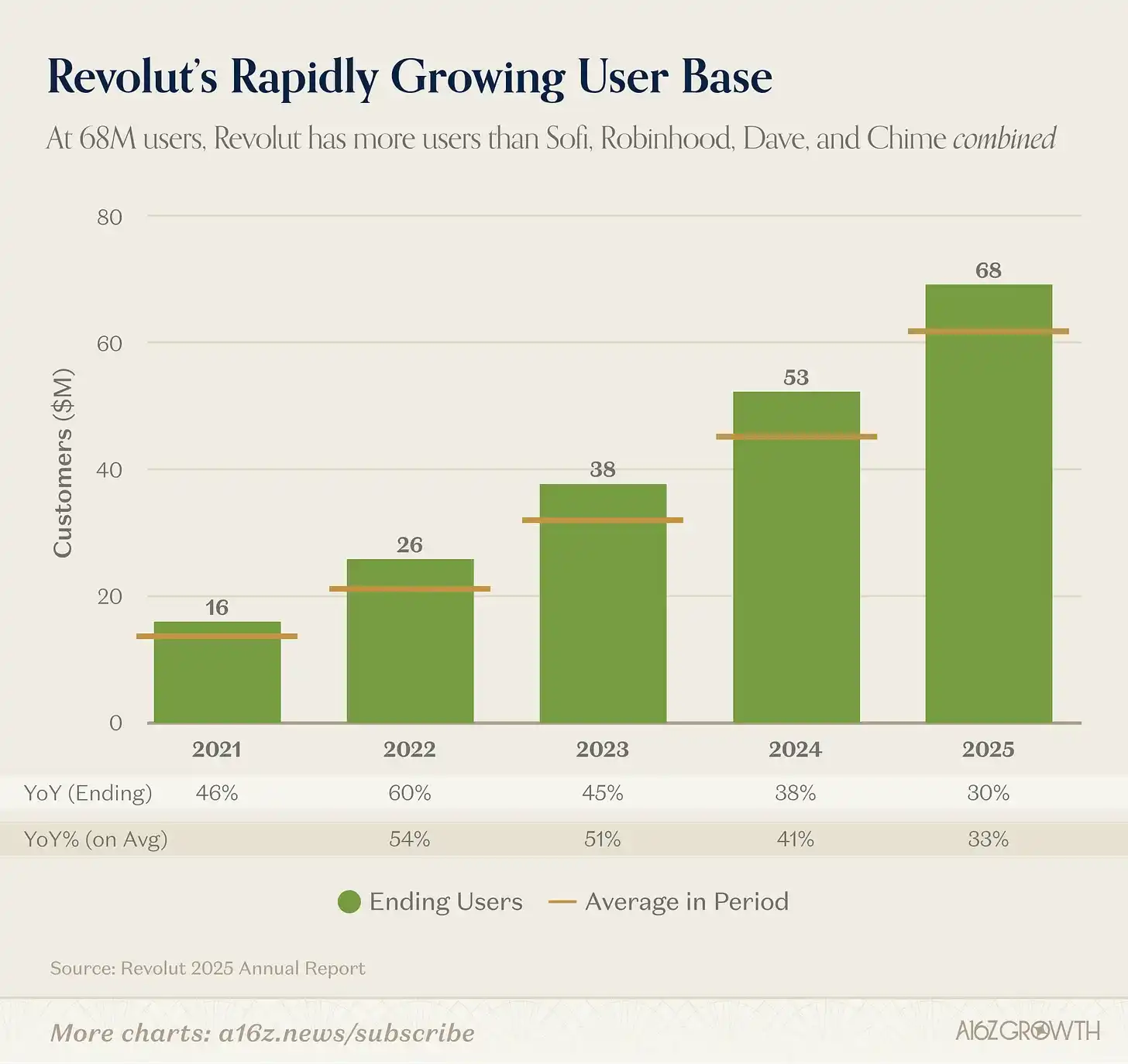

Overall, the user base continues to grow at a 30% CAGR, reaching 68 million by the end of 2025.

Source: Revolut Annual Report

To put 68 million users into perspective: JPMorgan Chase—the world's largest bank outside China—has about 85 million consumer customers (over 70 million of whom are considered "digitally active").

Admittedly, JPMorgan's total AUM makes its scale far exceed Revolut's, but from a pure user coverage perspective, Revolut is no longer just a "challenger"; it's a real competitor. Revolut has more users than Sofi, Robinhood, Dave, and Chime combined.

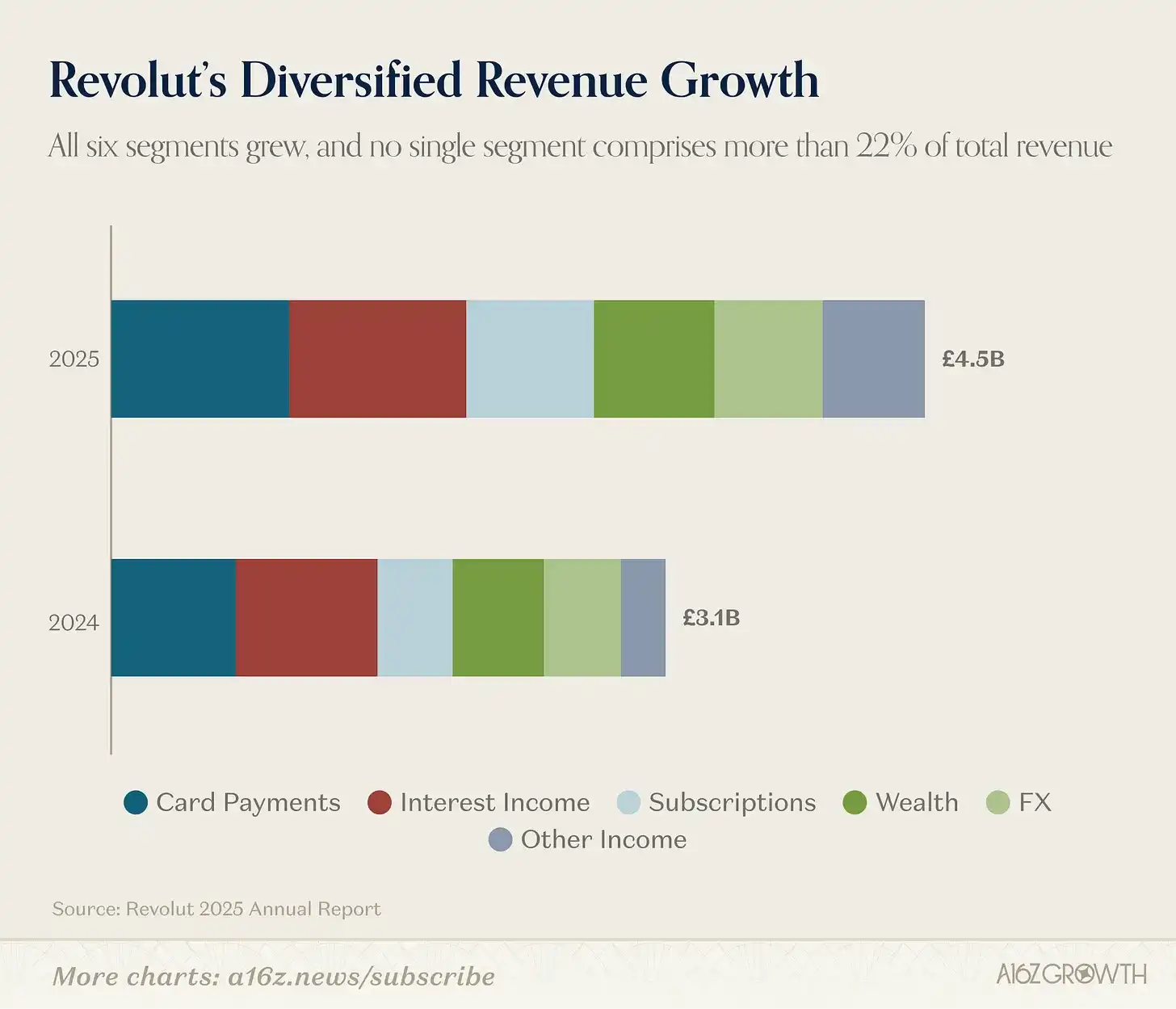

The complete product suite not only continues to attract more customers but also creates an increasingly diversified revenue structure:

Source: Revolut Annual Report

The company publicly discloses 6 main revenue sources:

Interest Income

Card Payments

Subscriptions

Other Income

All six segments grew year-over-year, with no single segment exceeding 22%.

The business is even more diversified than this disclosure suggests, as each revenue stream likely contains multiple sub-products (e.g., the Wealth segment includes both public stocks and crypto assets). In 2025, 11 product lines each generated over £100 million in revenue.

Importantly, 76% of revenue came from fees, up over 4 percentage points from 2024, while interest income accounted for just under 22%. This is the opposite of mature banks, which derive over 70% of their income from interest, and is one reason Revolut can achieve high ROE (more on this later).

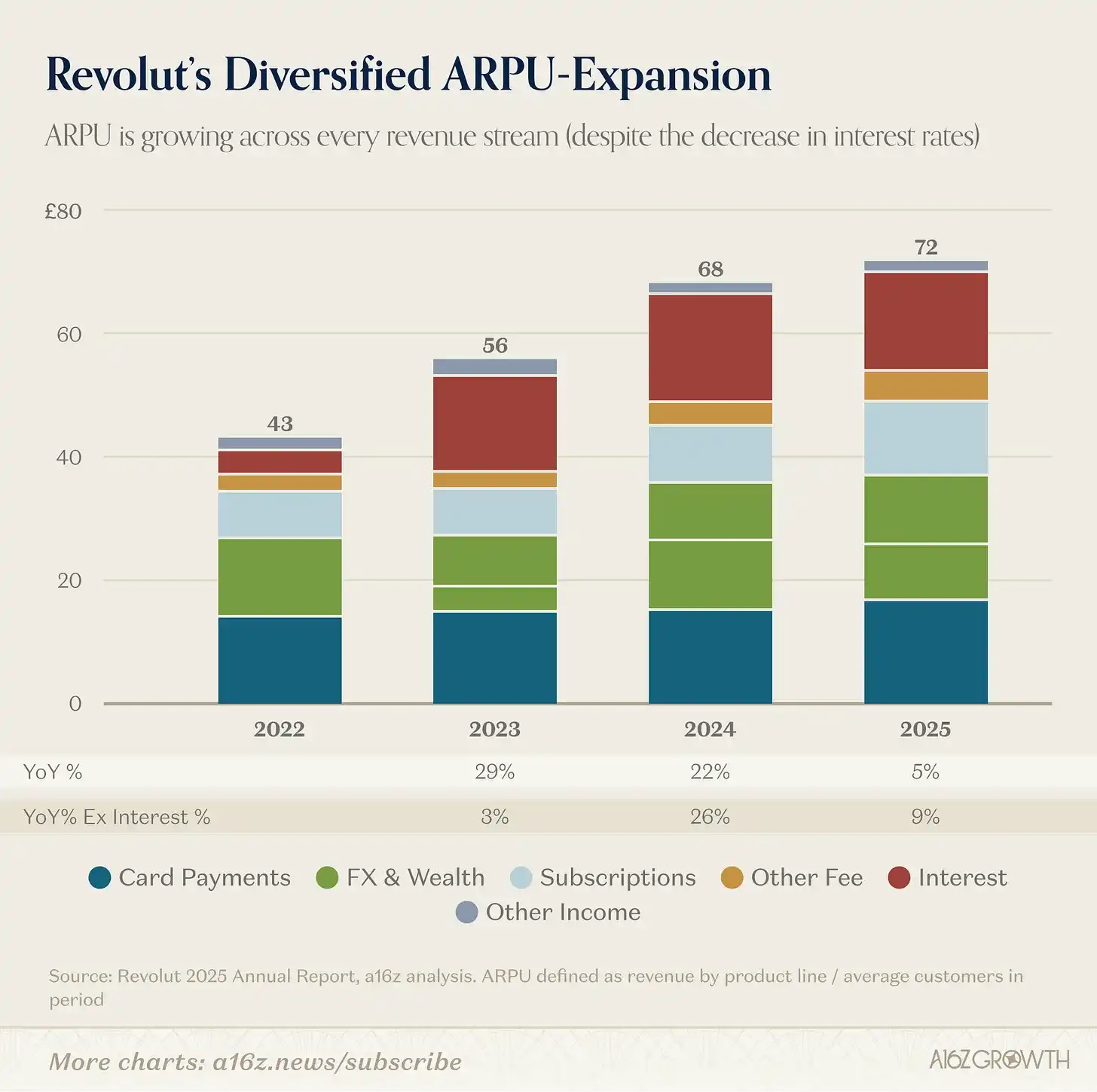

Unsurprisingly, the diversified revenue structure has also led to diversified ARPU growth.

Chart: ARPU defined as segment revenue / average number of customers during the period.

Source: Revolut Annual Report

Since 2022, each disclosed revenue stream has grown, and overall ARPU has increased by approximately 65%, representing an 18% annualized CAGR.

The importance of diversification is that it supports sustained compounding and builds resilience. In any given year, some product lines may boom while others face headwinds (like last year's rate decreases). But overall, strong ARPU growth can still be driven by new product additions and continued wallet share gains in core businesses.

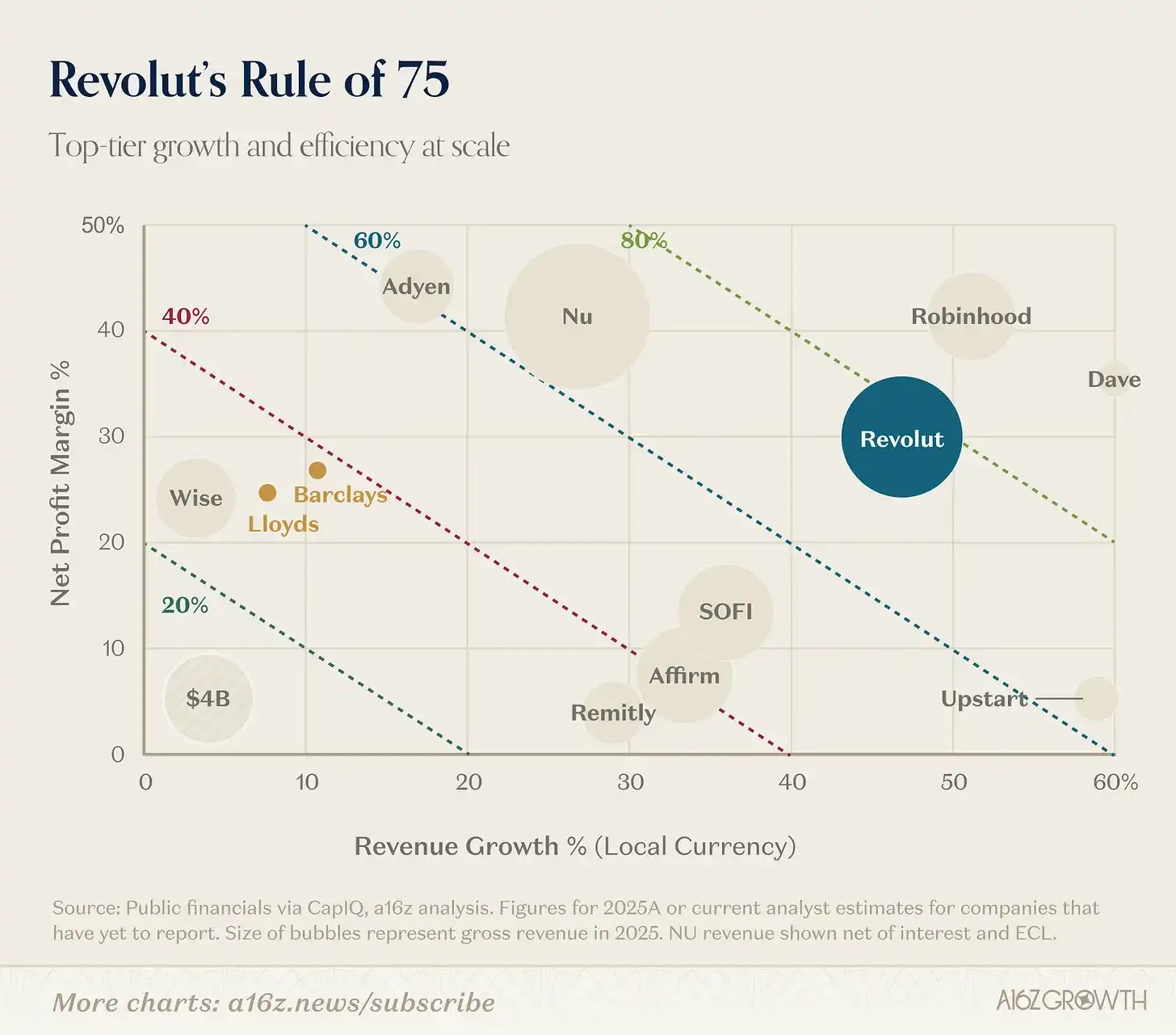

III. Top-Tier Efficiency

Revolut demonstrates rapid user growth,极强的 product iteration speed, and diversified revenue. The efficiency we promised is also delivered.

In 2025, Revolut achieved 46% revenue growth and a 29% net profit margin, resulting in a "Rule of X" (growth + profit margin) of 75%. The "Rule of 40" is no longer sufficient!

Chart: 2025A data or current analyst forecasts for companies yet to report. Bubble size represents total revenue in 2025. NU revenue is net of interest and ECL.

Source: Public financial data via CapIQ, a16z analysis

This combination of growth and efficiency places Revolut in an extremely rare position—companies achieving a Rule of 75% at over $1 billion in revenue are few and far between in history.

In fact, given that consensus growth expectations for Robinhood and Dave next year are both below 30%, Revolut might soon stand alone at the top of the podium.

Efficiency is ingrained in Revolut's DNA. Building its own banking infrastructure, highly organic growth, and strict cost control combine to achieve a 29% net profit margin. Coupled with minimal physical branches, Revolut now has a meaningful cost advantage over traditional banks, an advantage that will compound as scale continues to grow.

AI is further enhancing operational leverage. Take customer service as an example:

In 2024, Revolut's smart assistant chatbot reduced issue resolution time by 80%. In 2025, this improvement continued—resolution time decreased by over 40% for retail and over 50% for business, while user NPS increased by nearly 12 percentage points year-over-year. Revolut's smart assistant now resolves over 75% of customer inquiries.

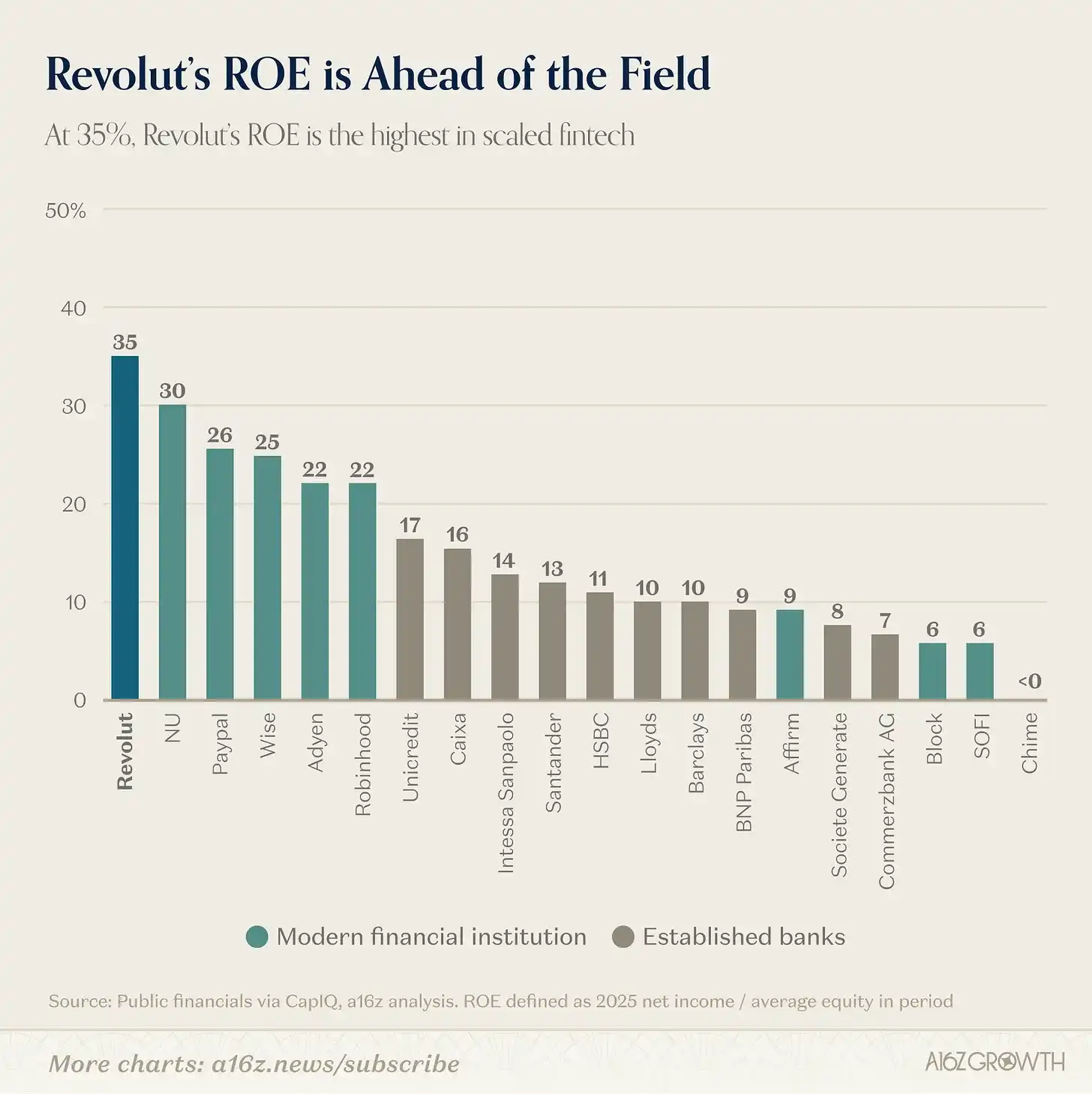

This efficiency enables Revolut to achieve the highest ROE we've seen among scaled fintech companies (and it's still improving). We've written before about the importance of ROE for bank valuation; Revolut is a paradigm of scale efficiency.

Chart: ROE defined as 2025 net income / average equity during the period.

Source: Public financial data via CapIQ

Revolut's 35% ROE is significantly higher than other leading consumer fintech companies and about 3-4 times that of mature banks. Note that Revolut is in an "over-capitalized" state (i.e., reported equity is higher than required by banking capital requirements), meaning its "true" ROE might be even higher.

It's rare to see growth being so capital efficient.

IV. Ample Room for Growth: ARPU × Number of Users

Despite Revolut's impressive 2025 performance, we believe there is still a significant runway ahead. Returning to the company's core revenue growth algorithm (Number of Users × ARPU), both variables still have considerable room for expansion.

More Users to Acquire

The company reported 68 million users at the end of 2025. As mentioned, this is a significant number, but it represents less than 15% of Europe's (excluding Russia) approximately 450-500 million adult population. This doesn't even include Australia and Singapore (existing markets), Mexico and Brazil (newly entered markets), the US (just applied for a banking license), and more regions yet to be explored.

Revolut has many more potential users to acquire.

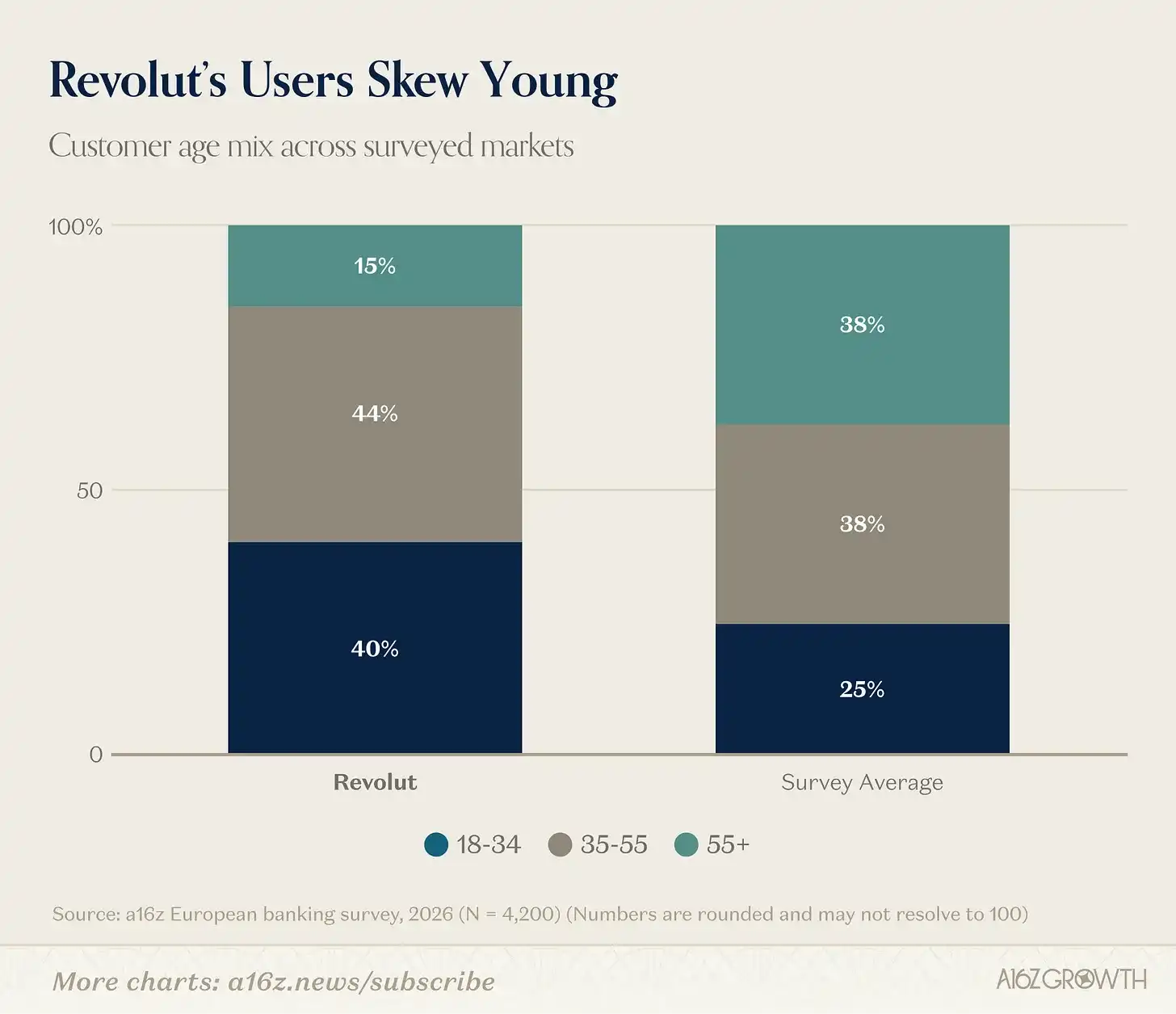

Moreover, the current user composition suggests the future won't be like the present. Unsurprisingly, Revolut's users skew younger and are more digitally native—we believe these users represent the future demands of the majority of the population.

Chart: Surveyed markets include UK, Ireland, France, Spain, Italy, Germany, and Poland.

Source: a16z European Banking Survey, February 2026 (N = 4200)

As Revolut continues to capture a large share of first-time account openers (and convinces older demographics that banking can be enjoyable), its market share should continue to grow.

Importantly, our research shows that about 25% of Revolut users under 35 use Revolut as their primary account. This alone will have a profound impact on future bank market shares in Europe as this user base ages.

More Room for ARPU Expansion

The other growth dimension, ARPU, has even more room.

Wallet share shifts in financial services typically happen over decades, not years. Revolut continues to win user trust: primary account users (per company definition) grew 45%, exceeding the overall user growth rate of 30%.

The rapid growth of primary account users is crucial because, in terms of ARPU, the "primary account" user is the grand prize:

Our research shows that mature customer relationships in traditional banking institutions can push their "primary account" share to over 60%.

Revolut primary account users self-report spending and saving about twice as much on their primary account compared to any other account they use—and spending amounts increase with age.

In short, more (and increasingly mature) primary account users can translate into higher ARPU, and if traditional banking ceilings are any guide, Revolut's rising "primary account share"上限 is quite high.

Another aspect of primary relationship growth is the lending revenue opportunity that Revolut has yet to fully tap:

As mentioned, 76% of Revolut's current revenue comes from fees, while the typical proportion for mature banking institutions is about 30%;

At the end of 2025, Revolut's Loan-to-Deposit Ratio (LDR) was only about 6%, compared to 70-90%+ for mature banks (or about 4% if calculated on total customer balances). Loan balances grew about 2x in 2025 and can continue to compound for many years.

Of course,稳健的 loan growth takes time. But if traditional banking ceilings are any reference, Revolut has ample opportunity to significantly expand ARPU by utilizing its balance sheet and offering better loan products to customers. For comparison, a simple estimate puts Barclays UK Consumer and Business Banking segment ARPU at around £435, about 6 times Revolut's current level.

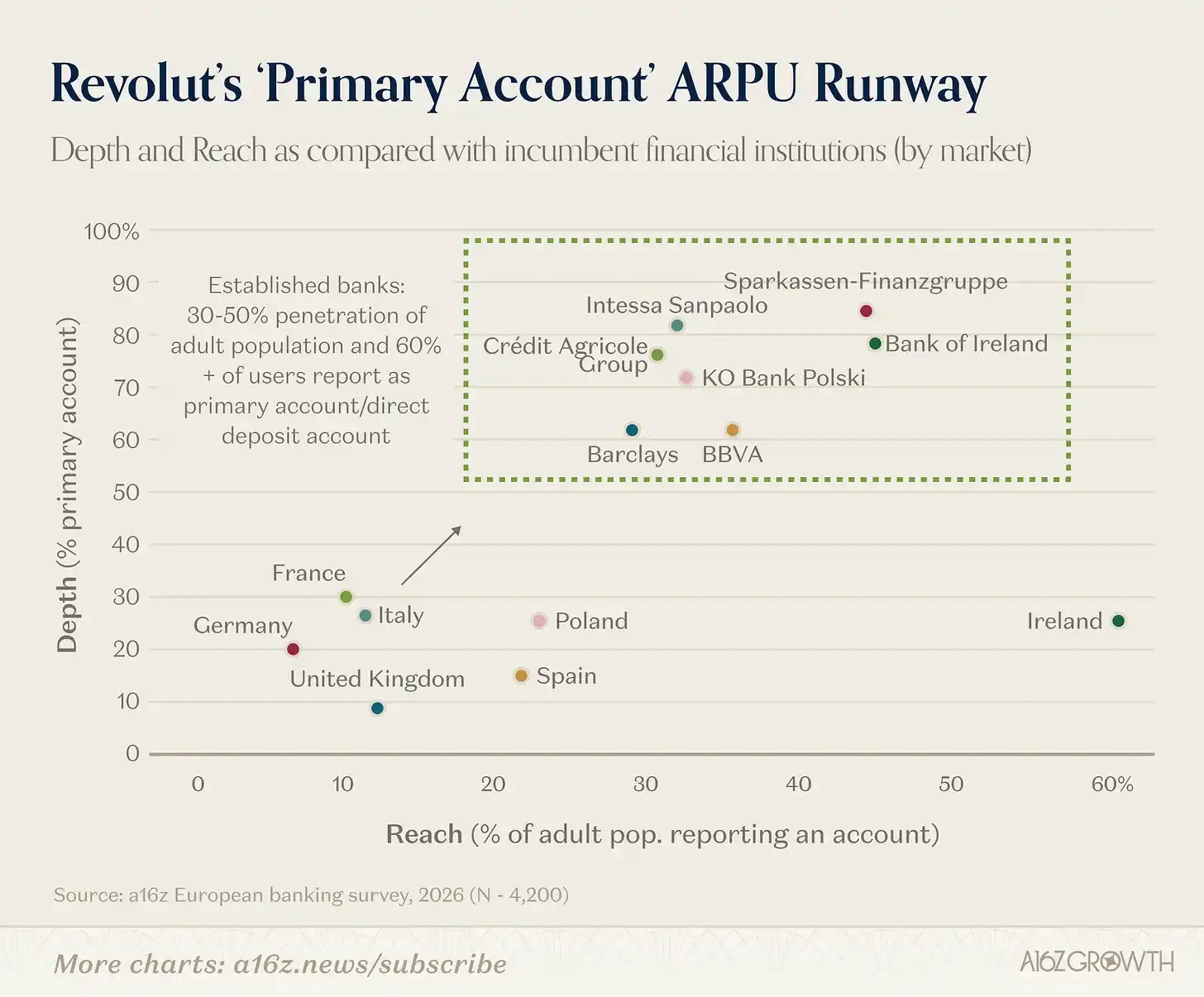

Here is where Revolut currently stands in terms of breadth (penetration) and depth (primary account share) of coverage:

Source: a16z European Banking Survey, February 2026 (N = 4200)

Revolut has ample runway to continue moving up and to the right (Ireland's case is mainly upward), both by expanding its user base and by deepening more relationships into "primary accounts." The latter should happen organically as the younger user base matures.

V. Conclusion: More Than Just a Challenger

Revolut's 2025 numbers are important not only because they are impressive but also because they paint a complete picture of a financial institution, not just a "challenger" bank.

User growth remains excellent, monetization continues to broaden, primary account adoption is rising, and profitability is strengthening even as the company continues to invest and expand rapidly. This combination is extremely rare in financial services (or any industry).

Execution challenges remain ahead—especially in lending, regulation, and entering new markets—but after reading this annual report, we feel the focus has shifted from "Can Revolut become a scaled banking platform?" to "How big can this platform become?"

The company's publicly stated long-term goal is "100 million daily active users in 100 countries." This journey is already underway.