Author: Ma He, Foresight News

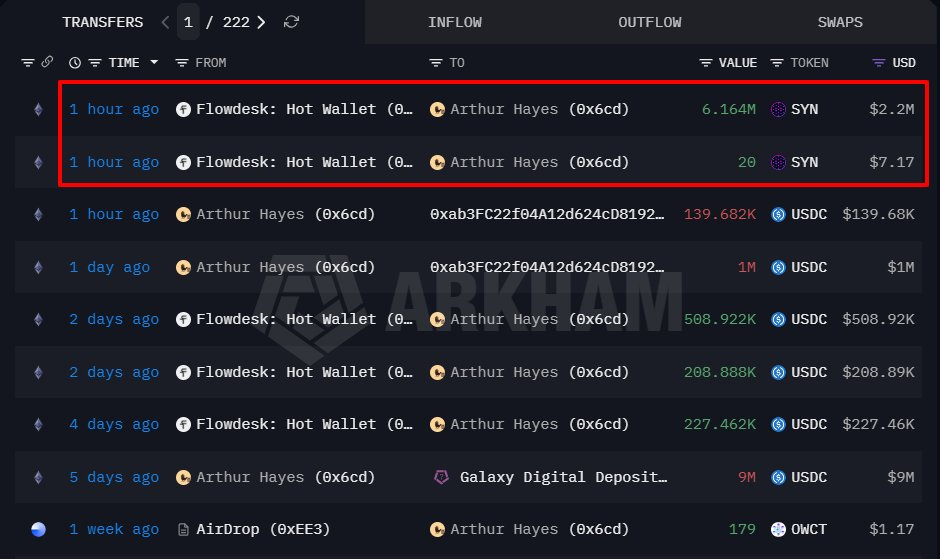

On June 29, an address associated with BitMEX co-founder Arthur Hayes purchased approximately 6.16 million SYN tokens via the OTC platform Flowdesk, with a transaction value of about $2.2 million at an average buy price of around $0.3573 per token.

Subsequently, Arthur Hayes posted on the X platform stating that SYN is one of the most asymmetric investments he has seen since HYPE and explicitly declared, "Now is the time for options DEX to officially challenge Deribit, and Hypercall is that challenger."

Currently, SYN is trading at $0.436, up over 40% in 24 hours. Since June 2026, the price of SYN has experienced explosive growth, increasing more than 10x in a single month, with an FDV of approximately $110 million.

Synapse: From Cross-Chain Infrastructure to On-Chain Options

Synapse Protocol was established in 2021, initially positioning itself as a universal cross-chain messaging and liquidity network. It allows developers to transmit arbitrary data between different blockchains, including smart contract calls and NFTs, going beyond simple asset bridging.

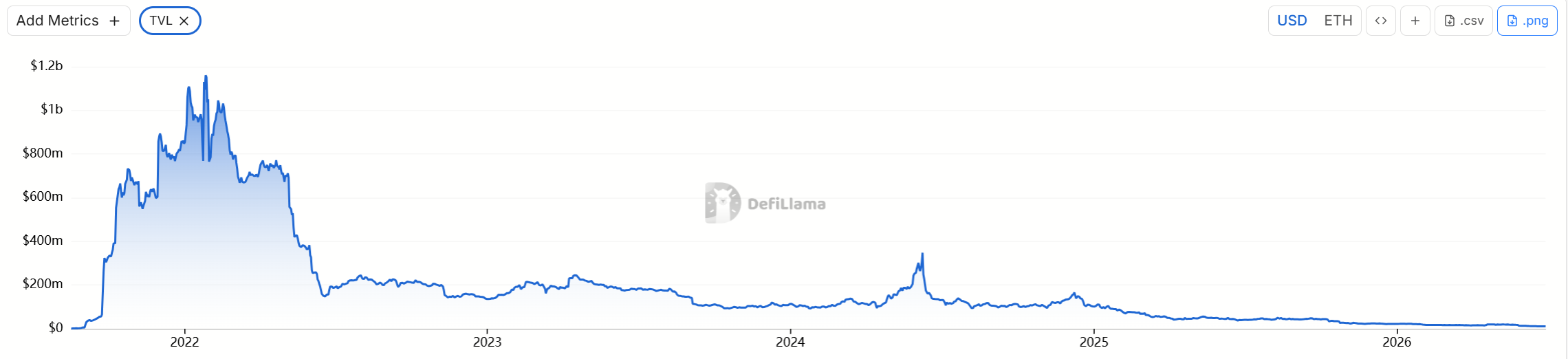

Early on, Synapse gained a foothold in the multi-chain ecosystem with its cross-chain AMM liquidity pools and low-slippage stablecoin swaps. During the 2021-2022 bull market, its TVL once exceeded $1 billion, making it a major player in the cross-chain bridge sector alongside projects like Wormhole, LayerZero, and Axelar. However, the competition in cross-chain connectivity is fierce, and compounded by the bear market impact, the protocol's TVL declined significantly.

According to the latest data from DefiLlama, as of June 2026, Synapse TVL is approximately $11.1 million, primarily concentrated on chains like Ethereum and Canto.

The SYN token, serving as the governance token, reached a high of around $5 in October 2021 but has remained subdued for a long time since.

Hypercall is an on-chain options trading protocol built by the Synapse team, deployed on HyperEVM within the Hyperliquid ecosystem. Its core proposition is to create "an options exchange that can trade any asset."

Unlike traditional centralized options platforms or early on-chain options protocols, Hypercall's official documentation states it supports trading at any scale, with contracts divisible down to the dollar or up to million-dollar levels. Additionally, the maximum loss on an option is limited to the premium paid, with no liquidation or cascading liquidation risks. It also supports 24/7 trading.

Currently, Hypercall's Mainnet Alpha is live, allowing users to connect their wallets to trade SpaceX (SPCX) options. BTC puts and NVDA spreads have also appeared as available underlyings. The team previously claimed its product has processed over $55 billion in cumulative trading volume.

Deribit: The Centralized Options Dominator

Founded in 2016, Deribit has long held an absolute dominant position in the crypto options market. According to industry data, its market share in BTC and ETH options is around 85%, making it the preferred platform for institutional traders, market makers, and quantitative funds.

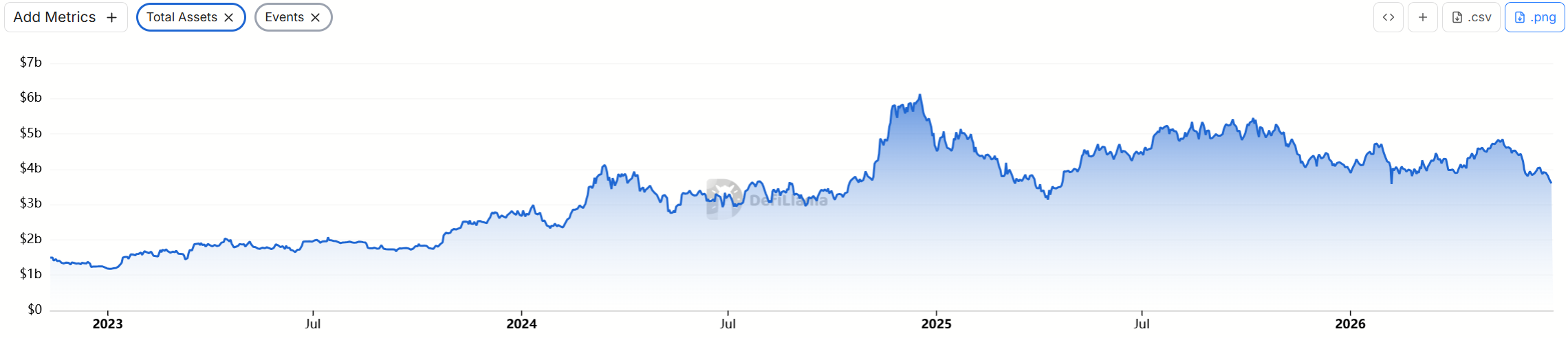

Currently, data from DeFiLlama shows its total asset value is $3.588 billion.

Deribit's advantages lie in its deep liquidity and professional tools: support for portfolio margin, block trading, and low-latency multicast data feeds. Furthermore, it has a long track record of stable operation. However, centralization brings inherent limitations: custodial risks, KYC barriers, regulatory uncertainty, and relative unfriendliness towards small retail users and DeFi natives. The complexity of options trading and the margin mechanism further amplify these pain points.

Arthur Hayes's call taps into the industry's core logic—as on-chain perpetual DEXs like Hyperliquid have demonstrated high performance, composability, and capital efficiency, the demand for on-chain options, as "precise tools for expressing volatility and direction," is accumulating.

Hypercall's potential advantages include: decentralization, permissionlessness, no KYC, and transparency. Moreover, deep integration with the Hyperliquid settlement layer promises a trading experience close to centralized platforms while retaining on-chain transparency. However, the protocol is still in its early Mainnet Alpha stage, with liquidity depth far inferior to Deribit. Initial underlying assets include SpaceX for testing; coverage of mainstream crypto options will take time. Historically, on-chain options protocols (like early versions of Hegic, Opyn) have made many attempts but often struggled to scale due to insufficient liquidity.

Deribit's network effects are difficult to replace in the short term. Hypercall is more likely to act as a "complement and differentiated competitor" rather than a direct replacement—especially in the DeFi-native and emerging asset (e.g., RWA, AI-related) options space.

What Game is the King of Shilling Playing?

Arthur Hayes's recent "shilling" track record shows significant divergence.

Previously, he was highly bullish on HYPE, predicting a price target as high as $150, but chose to liquidate all his HYPE holdings in early June. He also liquidated his holdings in previously shilled NEAR and WLD. On June 16 and 23, on-chain tracking data showed he repurchased a total of 91,000 HYPE tokens via an exchange.

On June 24, the release of a CARDS (Collector Crypt) in-depth research report by Arthur Hayes's family office, Maelstrom, also sparked controversy. The report set a price target of $4 by the end of summer.

Just 4 days later, CARDS's market cap had fallen approximately 22% since Maelstrom set the target price.

Currently, its price is $0.2437, with a market cap of $100 million and an FDV of $487 million.

On-chain detective ZachXBT previously criticized Arthur Hayes on X, tweeting, "How much exit liquidity has your fanbase created for you over the last few days?" Arthur Hayes responded that he was just trading normally, prices can go up or down, and stated, "Happened to get this one right."