Original | Odaily Planet Daily (@OdailyChina)

Author | Azuma (@azuma_eth)

In the early hours of December 16, stablecoin giant Circle officially announced the signing of an agreement to acquire the core talent and technology of Interop Labs, the initial development team behind the cross-chain protocol Axelar Network. This move is intended to advance Circle's cross-chain infrastructure strategy and help achieve seamless, scalable interoperability for core products like Arc and CCTP.

This seemed like another classic case of an industry giant acquiring a high-quality team, appearing to be a win-win situation. However, the key issue lies in the fact that — Circle explicitly stated in the acquisition announcement that the transaction only involves the Interop Labs team and its proprietary intellectual property, while the Axelar Network, the Axelar Foundation, and the AXL token will continue to operate under community governance. The other contributing team to the original project, Common Prefix, will take over the relevant activities previously handled by Interop Labs.

In simple terms, Circle has taken the original development team of Axelar Network but has explicitly discarded the Axelar Network project itself and its AXL token.

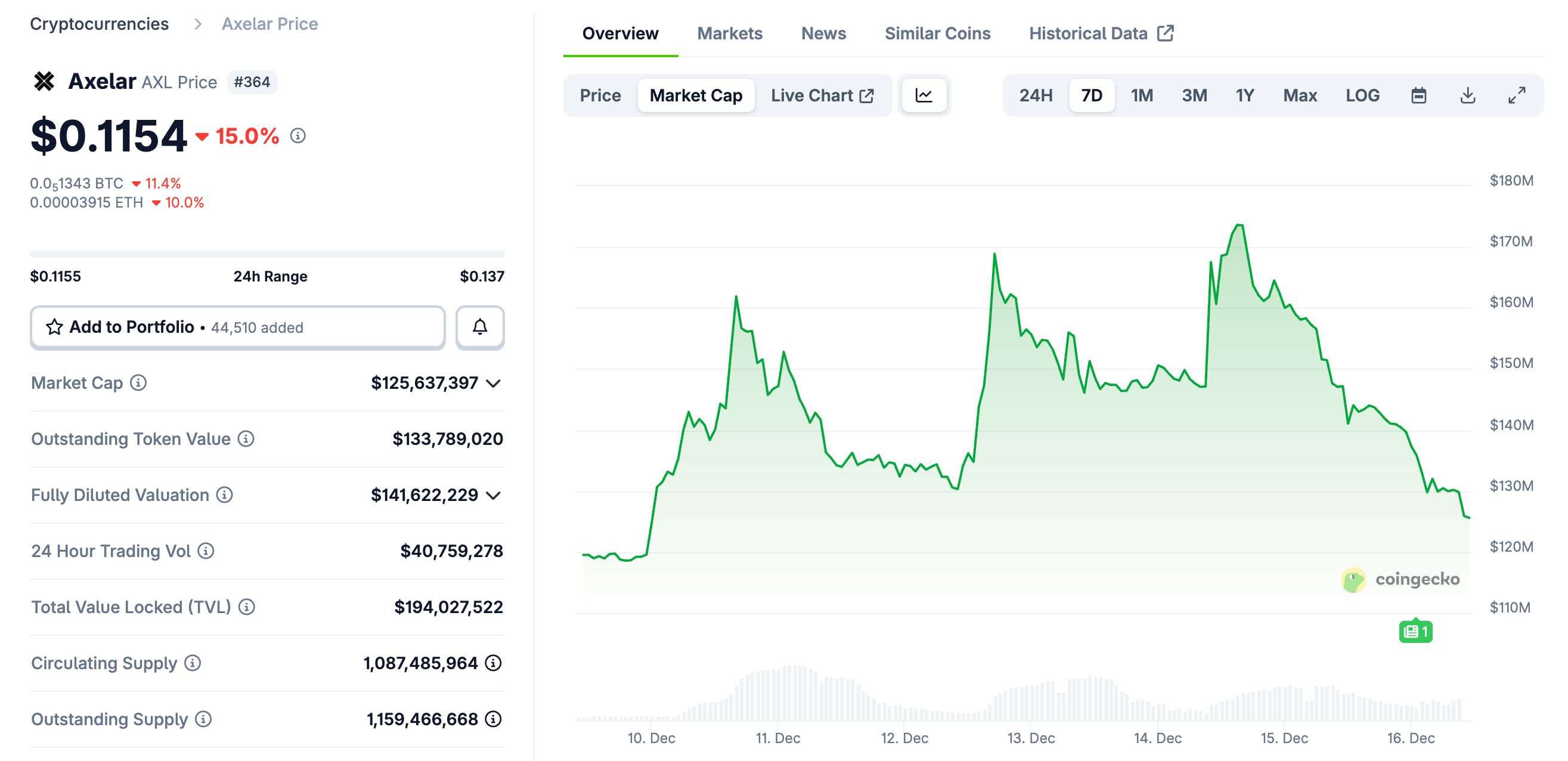

Affected by this sudden news, AXL experienced a sharp short-term drop, trading at around $0.115 as of 10:00 AM today, marking a 24-hour decline of 15%.

Simultaneously, the unique "take the team, not the token" nature of the acquisition and the ensuing debate over "equity vs. token" issues have sparked extensive discussion within the community, with supporters and opponents of this acquisition model arguing their respective points.

Opposing Views: De facto Rug Pull, Circle's Misstep, Only Token Holders Get Hurt......

The core of the opposition consists of some VCs, which is understandable — "I invested real money in the project's token, holding a bunch of tokens. Now you've taken the working team away, what use are these tokens to me?"

Moonrock Capital founder Simon Dedic commented on this: "Another acquisition, another rug pull. Circle acquires Axelar but explicitly excludes the Foundation and the AXL token. This is practically criminal. Even if not illegal, it violates ethics. If you are a founder wanting to issue a token: either treat it like equity, or get lost."

The Block co-founder and 6MV founder Mike Dudas commented: "For everyone thinking this is a token vs. equity issue, let me be clear, this is entirely Circle's doing. There are rumors that Circle's VP of Corporate Development once told an Axelar co-founder 'I don't care about your investors,' and 'bought' the CEO and IP out from under the investors without paying them any consideration, even though this IP and team are crucial for Arc's launch."

<2>Lombard Finance founder posted a chart of AXL's price movement and predicted: "Axelar's core team has been bought by Circle, AXL might be worthless now. It's been over three years since the token was issued, the team's equity has long been fully vested. But this outcome feels very uncomfortable: the team and/or investors sell tokens for profit, while token holders can only pin their hopes on a distant dream."ChainLink community figurehead Zach Rynes stated: "This once again the token vs. equity conflict of interest plaguing the crypto industry. The development team behind the protocol gets successfully acquired, while the token holders who funded that team get nothing. So-called continued independent operation under community governance is no different than the development team abandoning its users for better prospects. If we want to attract real capital, this is the primary issue the industry urgently needs to solve."

SOAR Ecosystem Lead Nicholas Wenzel stated: "Axelar token is going to zero, thanks for playing. Yet another acquisition where token holders get nothing and equity holders get paid."

Supporting Views: Normal Market Behavior, Tokens Are Naturally at the Bottom of the Capital Stack

If the opposition focuses more on the unfair treatment of token holders, the supporters focus more on the rules of financing and M&A markets.

Arca Chief Investment Officer Jeff Dorman believes Circle's approach is not problematic and explained at length the capital structure of corporate financing and the naturally disadvantaged position of tokens.

Companies raise capital through different tiers of the capital structure, and these tiers themselves have a clear order of priority—some tiers are inherently senior to others — Secured Debt > Unsecured Senior Debt > Subordinated Debt > Preferred Stock > Common Stock > Tokens.

History is full of examples where gains for one type of investor come at the expense of another.

- In bankruptcies, creditors win at the expense of equity investors;

- In Leveraged Buyouts (LBOs), equity holders often profit at the expense of creditors;

- In take-unders, creditors are usually prioritized over equity holders;

- In strategic acquisitions, usually both creditors and equity holders benefit (but not always);

- And tokens are often at the very bottom of the capital stack......

This doesn't mean tokens have no value, nor does it mean tokens necessarily need some form of "protection," but the market needs to recognize the reality: when someone acquires a company whose value is low and whose issued token is also nearly worthless, token holders don't magically receive a dividend. In such cases, gains for equity often come at the expense of the token.

Electric Capital co-founder Avichal Garg also commented: "This is normal. If all future value is created by the team, no company will want to pay returns to investors."

Core Contradiction: What Exactly Is a Token?

Surrounding the "take the team, not the token" acquisition storm involving Axelar and Circle, both sides of the debate seem to have their points.

The anger of the opposition is real: Token holders bore the risk when the project was at its most difficult, needing liquidity and narrative support the most, yet were completely excluded at the critical moment of value realization. From the result, the core team and intellectual property achieved value realization, while the token was left in the vacuum narrative of "community governance." The market voted most directly with the price, which is indeed deeply frustrating for all who believed in the token's value.

The judgment of the supporters is also reasonable in a practical sense: From a strict capital structure perspective, tokens are neither debt nor equity and naturally lack priority in the context of M&A and liquidation. Circle did not violate existing commercial rules; it just冷静地 chose the assets most valuable to itself.

The true core of the contradiction is not whether Circle acted morally, but lies in a question the industry has long deliberately avoided: What exactly is a token in the legal and economic structure?

When prospects are bright, tokens are tacitly assumed to be "quasi-equity," imbued with the imagination of a claim on future success; but in practical scenarios like acquisitions, bankruptcy, and liquidation, they are quickly reduced to their original form of a "rights-less instrument." This narrative equity-like treatment combined with structural subordination is the root cause of recurring conflicts.

The Axelar acquisition may not be the last similar controversy, but hopefully it can serve as an opportunity for the industry to further contemplate the positioning and meaning of tokens — Tokens do not inherently possess rights; only institutionalized, structured rights are acknowledged at critical moments. The specific form of implementation still requires all practitioners to explore and practice together.