In the face of heightened bearish performance and volatility, Solana is showing notable strength in the derivatives market. While SOL’s price has fallen sharply lately, bullish momentum is returning, and the monthly perpetual futures volume is experiencing one of its most significant growths ever.

Monthly Perps Volume on Solana Surges Past Previous Peak

Solana is experiencing sharp growth in some crucial areas even while the altcoin has fallen strongly, with its price retesting the $75 support level. In areas such as the derivatives market, SOL has reached a new landmark, breaking past previous record levels in monthly perpetual futures volume.

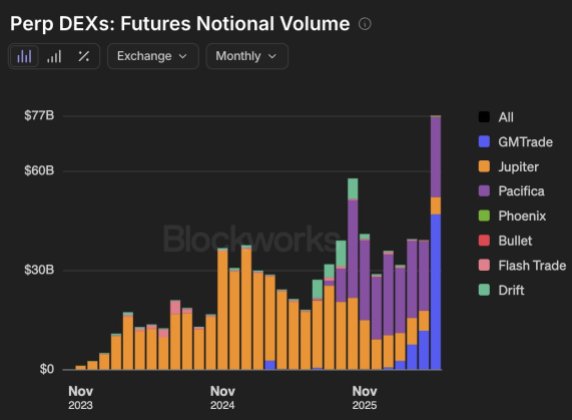

David Alexander, a crypto pundit, reported that SOL has shattered its previous monthly perpetual futures volume record by processing over $76.7 billion in May 2026 alone. This figure represents approximately 34% increase above the previous high of $57 billion set in November 2025.

The spike indicates a significant uptick in speculative activity and trader engagement throughout the Solana ecosystem, highlighting the network’s expanding impact on the cryptocurrency trading space. After this notable growth, the perps volume is now showing a 97% rise in month-over-month.

A rise to a new high in this metric is typically seen as an indication of heightened market interest, more liquidity, and more active participation from institutional and retail players. “Perhaps more interestingly, is what’s being built underneath,” Alexander stated. As the market evolves, perps are quietly becoming one of the most important financial primitives, both within the on-chain economy and extending into the legacy financial system.

Currently, the battle for dominance has become more intense than ever before. Meanwhile, Solana is portraying itself as the only network with actual price discovery powered by two-sided flow and 100% on-chain execution, as opposed to off-chain or synthetic matching.

This implies that each order, oracle update, match, cancellation, and settlement occurs on-chain. However, SOL perps in the next generation are resolutely designed to route revenue back to the network at the protocol level from launch.

A Massive Surge In Stablecoin Activity On The SOL Network

The Solana network is receiving fresh attention due to a significant increase in stablecoin activity, which highlights its expanding role as a hub for on-chain liquidity and digital finance transactions. Zensei, a market researcher, stated that the network’s stablecoin activity continues to operate at a scale most networks can only dream of.

In a one-week time frame, the SOL network processed over $79.9 billion in stablecoin transaction volume. Billions of dollars are seen being moved within the network every single day, indicating robust network health and economic participation. “When people choose to move money on-chain, the numbers keep showing they choose Solana,” Zensei added.

Users increasingly turning to SOL for payments, trading, and Decentralized Finance (DeFi) points to rising interest and demand for fast and low-cost transfers, which the network seems to offer.