作者:Nikka / WolfDAO( X : @10xWolfdao )

在2026年初加密市场持续回调的背景下(BTC徘徊89,000-90,000美元,ETH约3,200美元),企业级囤币策略已成为市场最重要的叙事之一。本文章将分析Strategy(前MicroStrategy)和Bitmine Immersion Technologies两家代表性公司的囤币行为,揭示其战略差异、财务模型及对市场的多维度影响。

第一部分:囤币行为深度解读

1.1 Strategy (MSTR):杠杆式信念注入

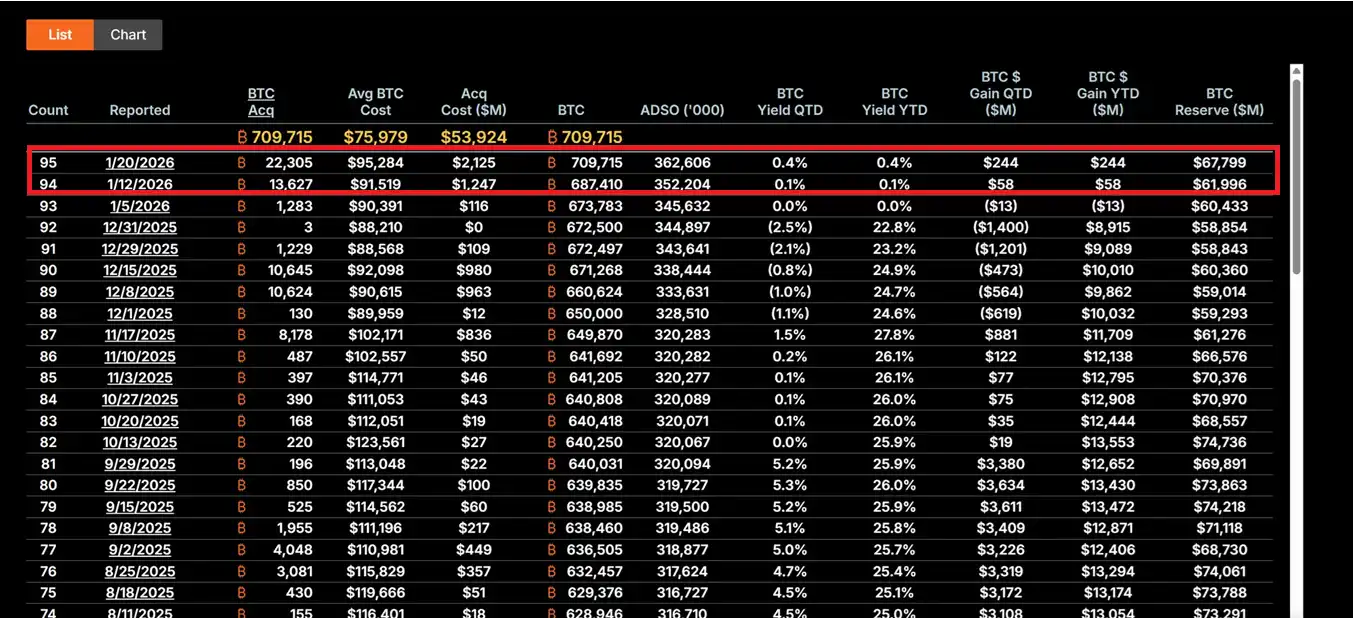

Strategy在CEO Michael Saylor的领导下,已将公司完全转型为比特币持有载体。2026年1月12-19日期间,公司以平均约95,500美元的价格购入22,305枚BTC,总价值21.3亿美元,这是过去九个月最大规模的单次买入。截至目前,MSTR总持仓达709,715枚比特币,平均成本为75,979美元,总投入近539.2亿美元。

其核心策略建立在"21/21计划"之上,即通过股权融资和固定收益工具各筹集210亿美元,用于持续购买比特币。这种模式不依赖运营现金流,而是利用资本市场的"杠杆效应"——通过发行股票、可转换债券和ATM(At-The-Market)工具,将法币债务转换为通缩性数字资产。这一策略使MSTR股价波动性通常是比特币价格波动的2-3倍,成为市场上最激进的"BTC代理"工具。

Saylor的投资哲学根植于对比特币稀缺性的极度信心。他将BTC视为"数字黄金"和通胀对冲工具,在当前宏观不确定性环境下(包括Fed利率政策摇摆、关税贸易战和地缘风险),这种逆势加码展现出机构级的长期主义。即使公司股价从高点回撤62%,MSTR仍被价值投资者视为"极端折扣"的买入机会。

若比特币价格回升至150,000美元,MSTR持仓价值将超1,064亿美元,股价在杠杆放大效应下可能产生5-10倍弹性。但反向风险同样显著:若BTC跌破80,000美元,债务成本(年化利率5-7%)可能触发流动性压力,迫使公司调整策略甚至面临清算风险。

1.2 Bitmine Immersion Technologies (BMNR):质押驱动的生产力模型

BMNR在Tom Lee的领导下采取了截然不同的路径。公司定位为"全球最大Ethereum Treasury公司",截至1月19日持有4.203百万枚ETH,价值约134.5亿美元。更关键的是,其中1,838,003枚ETH参与质押,按当前4-5%的年化收益率计算,每年可产生约5.9亿美元的现金流收入。

这种"质押优先"策略使BMNR具有内在价值缓冲。与MSTR的纯价格敞口不同,BMNR通过网络参与获得持续收益,类似于持有高息债券但附加以太坊生态增长红利。公司在2025年Q4至2026年Q1期间新增质押581,920枚ETH,显示出对网络长期价值的持续承诺。

BMNR的生态扩展战略同样值得关注。公司计划于2026年Q1推出MAVAN质押解决方案,为机构投资者提供ETH管理服务,构建"ETH per share"增长模型。此外,1月15日对Beast Industries的2亿美元投资以及股东批准的股份限额扩展,都为潜在并购(如收购小型ETH持有公司)铺平道路。公司还持有193枚BTC和Eightco Holdings 2,200万美元股权,总加密及现金资产达145亿美元。

从风险管理角度,BMNR的质押收益提供了下行保护。即使ETH价格在3,000美元区间震荡,质押收益仍能覆盖部分机会成本。但若ETH网络活动持续低迷导致质押APY下降,或者价格跌破关键支撑位,公司NAV折价可能进一步扩大(当前股价约28.85美元,较高点已跌超50%)。

1.3 策略对比与演化

两家公司代表了企业囤币的两种典型范式。MSTR是进攻型、高风险高回报的杠杆模型,完全依赖比特币价格升值实现股东价值。其成功建立在对BTC长期供应稀缺性和宏观货币贬值趋势的信念之上。BMNR则是防御型、收益导向的生态模型,通过质押和服务构建多元化收入来源,降低对单一价格波动的依赖。

值得注意的是,两者都吸取了2025年的教训,转向更可持续的融资模式。MSTR避免过度股权稀释,BMNR则通过质押收益减少对外部融资的依赖。这种演化反映出企业囤币从"实验性配置"向"核心财务战略"的转变,也标志着2026年"机构主导而非散户FOMO"时代的到来。

二:对市场的多维度影响

2.1 短期影响:底部信号与情绪修复

MSTR的巨额买入往往被市场解读为比特币底部的确认信号。1月中旬21.3亿美元的购买行为推动了比特币ETF的单日流入达8.44美元,显示机构资金正在跟随企业囤币的步伐回流。这种"企业锚定"效应在散户信心脆弱时期尤为重要——当恐慌与贪婪指数显示"极度恐惧"时,MSTR的持续买入为市场提供了心理支撑。

BMNR的以太坊积累同样产生催化作用。公司的策略呼应了BlackRock等传统金融巨头对以太坊在RWA(现实世界资产)代币化领域主导地位的看好。这可能引发"ETH Treasury第二波",SharpLink Gaming、Bit Digital等公司已开始跟进,加速质押采用和生态并购趋势。

投资者情绪正从恐慌向谨慎乐观转变。这种情绪修复在加密市场具有自我强化特性,可能为下一轮上涨周期播下种子。

2.2 中期影响:波动放大与叙事分化

然而,企业囤币的杠杆特性也放大了市场风险。MSTR的高杠杆模型在比特币进一步回调时可能触发连锁反应。由于其股价beta系数是BTC的2倍以上,任何价格下跌都会被放大,可能导致被动抛售或流动性危机。这种"杠杆传导"效应在2025年曾引发过类似的清算潮,当时多家杠杆持仓者在快速下跌中被迫平仓。

BMNR虽有质押收益缓冲,但也面临挑战。以太坊网络活动低迷可能导致质押APY下滑,削弱其"生产力资产"优势。此外,若ETH/BTC比率持续疲软,可能加剧BMNR的NAV折价,形成负面反馈循环。

更深层的影响在于叙事分化。MSTR强化了比特币作为"稀缺避险资产"的定位,吸引寻求宏观对冲的保守投资者。BMNR则推动以太坊的"生产力平台"叙事,突出其在DeFi、质押和代币化领域的应用价值。这种分化可能导致BTC和ETH在不同宏观场景下表现脱钩——例如在流动性紧缩环境下,BTC可能因"数字黄金"属性表现更强;而在科技创新周期中,ETH可能因生态扩展获得溢价。

2.3 长期影响:财务范式重塑与监管适应

从长期视角看,MSTR和BMNR的行为可能重塑企业财务管理范式。如果美国CLARITY Act成功落地,明确数字资产的会计处理和监管分类,将大幅降低企业配置加密资产的合规成本。该法案可能推动Fortune 500公司配置超1万亿美元的数字资产,使企业资产负债表从传统的"现金+债券"组合转向"数字生产力资产"。

MSTR已成为"BTC代理"的教科书案例,其市值与净资产价值(NAV)的溢价机制被称为"反射飞轮"——通过溢价发行股票购买更多比特币,提升每股BTC持有量,进而推高股价,形成正反馈循环。BMNR则为ETH Treasury提供了可复制的模板,展示了质押收益如何为股东创造持续价值。

这也可能引发行业整合浪潮。BMNR已获股东批准用于并购的股份扩展,可能收购小型ETH持有公司,形成"Treasury巨头"。弱势囤币公司可能在宏观压力下被迫出售或并购,市场呈现"优胜劣汰"格局。这标志着加密市场从"散户主导"向"机构主导"的结构性转变。

然而,这一进程并非没有风险。若监管环境恶化(如SEC对数字资产分类采取强硬立场)或宏观经济意外恶化(如Fed因通胀反弹而加息),企业囤币可能从"范式转变"变为"杠杆陷阱"。历史上,类似的金融创新在监管打击或市场逆转时往往导致系统性危机

三:核心问题探讨

3.1 企业囤币:新黄金时代还是杠杆泡沫?

这一问题的答案取决于观察视角和时间尺度。从机构投资者角度,企业囤币代表着资本配置的理性演化。在全球债务膨胀、货币贬值担忧加剧的背景下,将部分资产配置于稀缺的数字资产(具有战略合理性。MSTR的"智能杠杆"并非赌博,而是利用资本市场工具将股权溢价转化为数字资产积累,这在股权市场充分认可其策略时是可持续的。

BMNR的质押模型更进一步证明了数字资产的"生产力"属性。年化5.9亿美元的质押收益不仅提供现金流,还使公司能够在价格波动中保持财务稳健。这类似于持有高息债券但附加网络增长红利,展示了加密资产超越"纯投机工具"的潜力。

然而,批评者的担忧也并非空穴来风。当前企业囤币的杠杆率确实处于历史高位,94.8亿美元债务和33.5亿美元优先股的融资规模在宏观逆风下可能成为负担。2021年零售泡沫的教训犹在眼前——当时许多高杠杆参与者在快速去杠杆中遭受重创。如果当前的企业囤币浪潮仅仅是将杠杆从散户转移至公司层面,而没有根本改变风险结构,那么最终的结果可能同样惨烈。

更平衡的观点认为,企业囤币处于"制度化过渡期"。这既不是简单的泡沫(因为具有基本面支撑和长期逻辑),也不是立即的黄金时代(因为监管、宏观和技术风险仍然存在)。关键在于执行——能否在监管明朗化前建立足够的市场认可?能否在宏观压力下维持财务纪律?能否通过技术和生态创新证明数字资产的长期价值?

结论与展望

MSTR和BMNR的囤币行为标志着加密市场进入新阶段。这不再是散户驱动的投机狂潮,而是机构基于长期战略的理性配置。两家公司虽采取截然不同的路径——MSTR的杠杆化信念注入与BMNR的质押驱动生产力模型——但都展现出对数字资产长期价值的承诺。

企业囤币本质上是一场关于"时间"的豪赌。它赌的是监管明朗化快于流动性枯竭,赌的是价格上涨先于债务到期,赌的是市场信仰强于宏观逆风。这场游戏没有中间地带——要么证明数字资产配置是21世纪企业财务的范式革命,要么成为又一个过度金融化的警示案例。

市场正站在十字路口。向左是机构主导的成熟市场,向右是杠杆崩溃的清算深渊。答案很将在未来12-24个月内揭晓,而我们都是这场实验的见证者。