Original Author: Dom

Original Compilation: Luffy, Foresight News

Bitcoin's price touched $60,000 last week. Under the model of diminishing returns, this is by no means simple noise. The market is touching the most fragile link in the entire four-year cycle and the logarithmic growth framework.

When the gains at the peak of Bitcoin's cycle have been severely compressed, if there is another historically deep correction, the appeal of its classic cycle will be completely lost.

This is not a prediction; it is mathematical law.

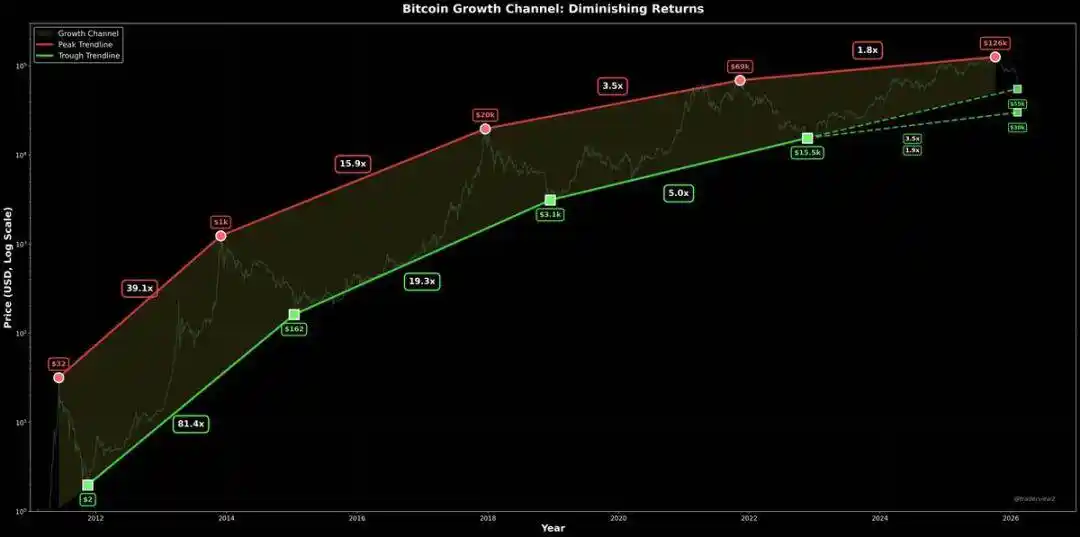

Cycle Peak Gains Are Compressing

Historical peaks of Bitcoin cycles:

- 2013: ~$1,242

- 2017: ~$19,700

- 2021: ~$69,000

- 2025: ~$126,000

Multiples of gains between cycle peaks:

- 1,242 → 19,700 = 15.9x

- 19,700 → 69,000 = 3.5x

- 69,000 → 126,000 = 1.8x (weakest in history)

This 1.8x says it all. Compared to history, the upside potential in this cycle is minimal. This pattern cannot withstand a significant drop; otherwise, Bitcoin's growth will completely flatten.

This 1.8x gain is the core truth of the current market. Relative to historical levels, Bitcoin's upside space is now extremely narrow. This cycle pattern can no longer withstand a major pullback; otherwise, Bitcoin's long-term growth momentum will completely stall.

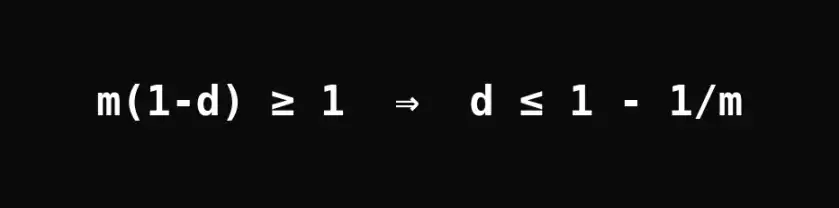

Pure Mathematical Constraint Formula

Definitions:

- m = Cycle peak multiple = Current cycle peak ÷ Previous all-time high

- d = Drawdown from peak (as a decimal)

Then, the bottom level of the next cycle relative to the previous high equals the current peak gain multiple multiplied by the remaining price proportion after the drawdown.

To ensure the bottom of the next cycle is not lower than the previous all-time high, the following condition must be met:

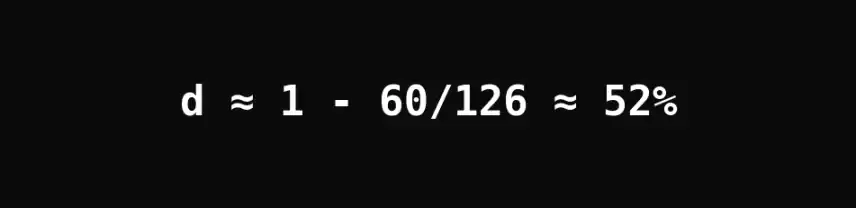

Substituting current cycle data: Previous ATH ≈ $69,000, Current cycle peak ≈ $126,000, we get:

Current peak multiple ≈ 1.8x. To maintain an intact bull market structure, the maximum allowed drawdown is approximately 44%. Currently, Bitcoin's drawdown has broken through this critical value.

Falling from about $126,000 to $60,000, Bitcoin's drawdown has exceeded the 44% "safety limit."

This means that if the previous all-time high was supposed to act as structural support, the current market is forcibly breaking through this support, forcing the market to a final conclusion.

$55,000 is the Key Make-or-Break Line

If Bitcoin falls to $55,000, two key signals will appear:

- A drawdown of 56%, far exceeding the 44% allowed upper limit

- The bottom price will be 20% lower than the previous all-time high ($69,000)

Once the price stays below $55,000, it means the market accepts that in this weak cycle with only a 1.8x gain, the cycle bottom can be significantly lower than the previous all-time high.

The subsequent impact will be: If the next cycle still maintains a 1.8x gain multiple, Bitcoin's price will rise from $55,000 to $99,000, and long-term growth momentum will stagnate. This is essentially a structural failure of the growth model; the market must change.

This is the core contradiction: Bitcoin's profit space has been severely compressed, but its volatility has not decreased proportionally. It's still a highly volatile market, but the peak gains have shrunk drastically. Such a cycle model is simply unsustainable.

Technical Support Near $55,000

From a technical perspective, the mid-$55,000 range has extremely strong structural support, mainly including:

- The 3000-day trendline (spanning over 8 years)

- The Volume-Weighted Average Price (VWAP) of the 2022 cycle low

- Support extension from the previous cycle's all-time high ($69,000)

Let's ponder: Why would an asset whose core belief is "long-term ultra-high returns" break below this triple structural support built up over years? Especially with the formal launch of convenient investment channels like ETFs, such a trend is completely contrary to the long-term growth trajectory.

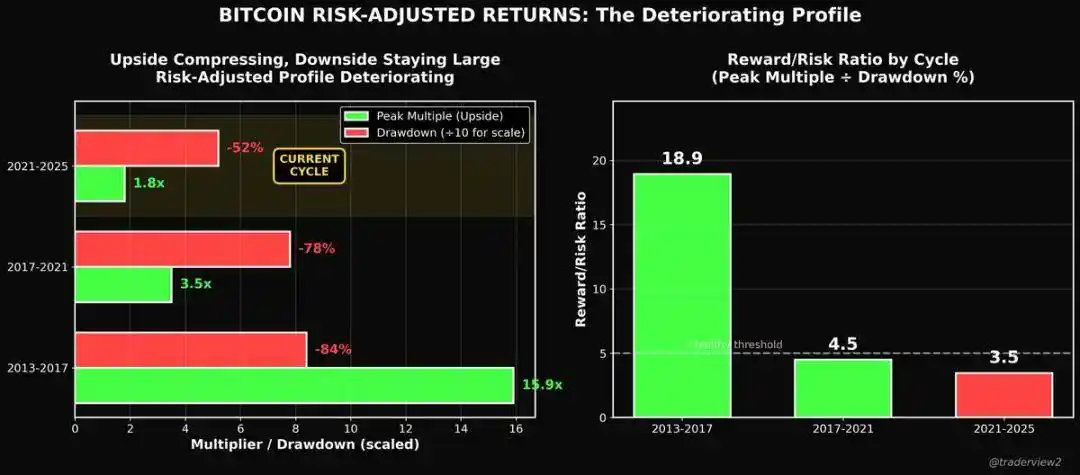

The Cliff of Risk-Adjusted Returns

This contradiction makes Bitcoin's entire cycle logic black and white: If the cycle peak multiple continues to shrink, but the drawdown magnitude does not shrink proportionally, Bitcoin's risk-reward ratio will completely deteriorate:

- The potential upside of the four-year cycle is only 20% to 50%

- The downside risk could still reach 50%

- Cycle trading would completely lose its meaning.

Faced with this dilemma, the market has only three ways out:

- Volatility contracts significantly (Path to Glory)

- The four-year cycle framework completely fails (Path to Ruin)

- A new demand driver emerges, resetting the growth curve and ending the trend of decaying gain multiples

ETFs are the most commonly mentioned potential driver, but they have already been launched. To truly reset the growth curve, three types of power are needed more: large-scale structural capital allocation, adoption at the sovereign national level, or sustained, price-insensitive rigid demand.

The Harsh Reality: Why This Cycle is So Different

When I entered the crypto market in 2017, the entire industry was full of hope and innovative vitality. People firmly believed these blockchain networks could bring real solutions to the world.

Nearly nine years later, it's hard to say that any large crypto ecosystem has truly achieved sustainable mainstream utility value matching the initial promises.

This cycle has harvested countless participants; the vast majority of tokens have performed almost nothing. More and more people are realizing the truth of the market: For the vast majority of crypto assets, this is essentially a PvP game where participants rely on leverage, liquidations, and capital rotation to profit from other participants, not from the value growth of the assets themselves.

The market's selection rule has never failed: In the long run, the vast majority of cryptocurrencies will eventually go to zero. Bitcoin, along with a few quality assets in the crypto space, still has a chance to escape this fate and achieve true value breakthrough.

The Choice Between Glory and Ruin

Path to Glory

Bitcoin achieves "breaking the circle and upgrading": Volatility contracts significantly, drawdowns are far below historical levels, and the previous all-time high region re-establishes itself as solid structural support. Although the cycle peak multiple shrinks, the asset's stability improves significantly, the risk-reward ratio optimizes greatly, and it truly becomes a sustainable long-term investment.

Path to Ruin

The four-year cycle framework completely fails. It's not that Bitcoin itself perishes, but the cycle logic that has sustained it for years no longer holds. Volatility remains at historical highs, but the profit space continues to compress. The previous all-time high no longer acts as a bottom support. The past growth channel becomes a historical relic. Bitcoin may still experience阶段性上涨 (periodic rises) in the future, and may continue to gain adoption, but the former cycle规律 (laws) will no longer be the dominant rules of the market.

Path to Reset

A全新的 (brand new) demand driver强势出现 (forcefully emerges), completely breaking the model of decaying gain multiples and reshaping Bitcoin's growth curve. This could come from large-scale structural capital allocation, widespread adoption by sovereign nations, or passive buying by institutional funds forming long-term support.

Additional Hidden Danger: The Long-Term Test at the Protocol Layer

This is not a core factor affecting the current market, but it is worth long-term attention: In the long run, Bitcoin must prove that it can evolve at the protocol layer, especially possessing quantum resistance. The core of the quantum issue concerns the security of Bitcoin ownership and protocol upgrade coordination, not mining itself. The security of early Bitcoin (like Satoshi's holdings) is the real potential threat.

If Bitcoin hopes to become a long-lasting asset, it must ultimately pass the test of "completing protocol upgrades without破坏市场信任 (destroying market trust)". This is like a background timer, not yet triggered, but始终是 (always is) an important hidden danger for Bitcoin's long-term development.

Simple Judgment Criteria

If, after the washout, Bitcoin reclaims and holds firmly above $69,000: The cycle structure is preserved, and the path to glory remains highly possible.

If Bitcoin's price remains in the $55,000 to $69,000 range: The market is under maximum pressure, and the cycle model faces its final test.

If Bitcoin's price stays consistently below $55,000: Against the backdrop of a weak cycle with a 1.8x peak multiple, a structural breakdown occurs, and the market structure is highly likely to undergo a fundamental change.

Conclusion

Bitcoin cannot long-term possess two traits simultaneously: low-gain asset, high-drawdown asset. If risk-adjusted returns still have meaning, the two cannot coexist long-term.

Bitcoin's touch near $60,000 is the market testing this life-and-death boundary in real time. Once the price falls below the $50,000 range, all debates will end, and the market will deliver its final verdict, either走向荣耀 (heading towards glory) or坠入毁灭 (plunging into ruin).