Author: Chloe, ChainCatcher

Last week, Open Standard launched the dollar stablecoin OpenUSD (OUSD), unveiling an impressive roster of over 140 endorsing companies, ranging from Visa, Mastercard, Stripe, American Express, to BlackRock, BNY, Standard Chartered, and further to Google, Shopify, Samsung, Coinbase, Solana, and Ripple. The news caused Circle's stock price to drop that same day. However, within just a few days, cracks began to appear in this dazzling list.

Multiple Korean Companies Distance Themselves

OUSD is led by Zach Abrams, co-founder of Bridge (which was acquired by Stripe in 2024). It highlights three key differences from existing stablecoins: zero fees for minting and redemption, no transaction volume caps, and the sharing of most of the revenue generated from reserve assets with partners driving adoption, rather than keeping it all for the issuer. In terms of governance, it has no single controlling entity; instead, decisions are made collectively by a board composed of partners, resembling the structure of payment networks like Visa and Mastercard. It plans to launch first on Solana, Polygon, Aptos, and Stellar chains.

However, according to a report by the Korean media 'Chosun Biz' on July 3rd, multiple companies among the 13 Korean firms listed have distanced themselves. Samsung Electronics stated that no formal negotiations have taken place, and the company is not even clear on what role it is supposed to play in the alliance. Shinhan Financial Group, Dunamu (parent of Upbit), and K Bank gave nearly identical statements: Open Standard merely asked if they 'were willing to participate,' and their response was simply 'we will evaluate it,' yet their names directly appeared on the official member list. More awkwardly, some companies said they only discovered their listing through local news reports, and their initial response was merely 'we would consider it if things go well,' expressing shock at being written into the alliance.

This skepticism is not limited to Korea. Gabor Gurbacs, founder of the US-based OpenAssets, said that several of his clients on the list told him they have never signed or agreed to anything, speculating that 'either the media has severely distorted this, or this participant list is misleading.' Objectively speaking, the list is not entirely fictitious; executives from companies like Mastercard, Stripe, Visa, Coinbase, BlackRock, BNY, and Adyen have indeed given named endorsements, with Stripe even stating its intention to make OUSD the default stablecoin for its platform merchants.

The real controversy lies in OUSD's model of sharing reserve yields. Being listed as a partner implies having economic interests, which makes the question of formal participation no longer just a matter of PR wording but a tangible commercial and reputational issue.

Stacking Reputation as a Marketing Habit: Past 'All-Star Alliances' Have Fallen from Grace

Stacking the reputation of giants to build momentum is a long-standing marketing habit in the crypto industry.

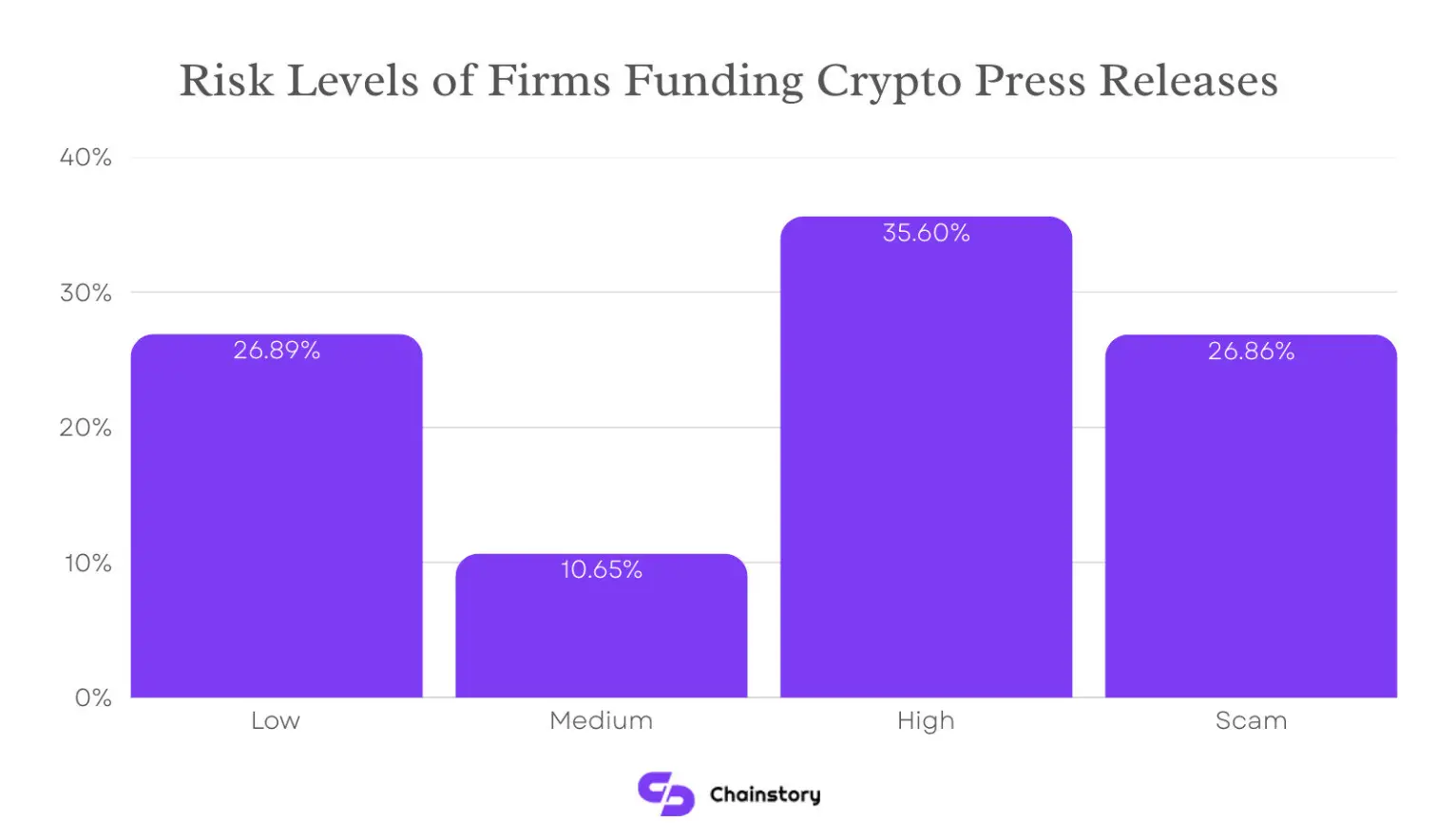

Chainstory analyzed nearly three thousand crypto press releases from the second half of 2025. Projects rated as high-risk accounted for 35.6% of all announced projects, and those marked as scams accounted for 26.9%. These suspicious categories combined made up over 62% of the total press releases. Meanwhile, low-risk projects accounted for only about 27% of the total press releases.

When it comes to how 'all-star alliances' can fall from grace, the most classic and fitting parallel is Facebook's Libra.

In the summer of 2019, Facebook announced with great fanfare, accompanied by a white paper, its intention to launch the stablecoin Libra. The lineup was unprecedentedly star-studded: on the payments side, there were Visa, Mastercard, PayPal, Stripe; in e-commerce, eBay and Shopify; in the crypto space, Coinbase; and even top-tier VCs like a16z were listed. Nearly half of Silicon Valley seemed to be cheering for it.

Later, a congressional hearing shifted its fate. Governments worldwide were concerned about threats to sovereign currencies and the dollar's dominance. France was the first to oppose it, while the U.S. Congress relentlessly questioned Facebook's past privacy and data scandals, challenging 'why should this company be the one to do this.' Regulatory pressure quickly spread to its allies. On October 4, 2019, PayPal was the first to withdraw; just a week later, Stripe, Visa, eBay, and Mastercard collectively exited. All this happened just days before Libra's first council meeting was scheduled to take place—before the first meeting even convened, the whole group was almost disbanded.

What followed was a series of desperate measures to survive: rebranding to Diem, moving its headquarters from Switzerland back to the U.S., pegging its value solely to the U.S. dollar, operating independently from Facebook, and the departure of key figures. By 2022, the entire project sold its assets to Silvergate for approximately $200 million, marking its official end.

The lesson of Libra is not about an erroneous currency issuance strategy, but that an alliance roster, no matter how dazzling, is not equivalent to a functioning product, let alone established real-world channels. Coincidentally, Visa, Mastercard, and Stripe, which abandoned Libra back then, are now the marquee names on the OUSD list. The same giants, in a different alliance—whether the story will be different remains to be seen.

Circle CEO Welcomes Competition with Open Arms

Facing the aggressive entry of OUSD, Circle CEO Jeremy Allaire stated that he welcomes competition and directly pointed out what he sees as the nature of this business: stablecoin networks are a business of platforms and network effects, where market structure tends towards winner-take-all, and building such networks takes a very long time.

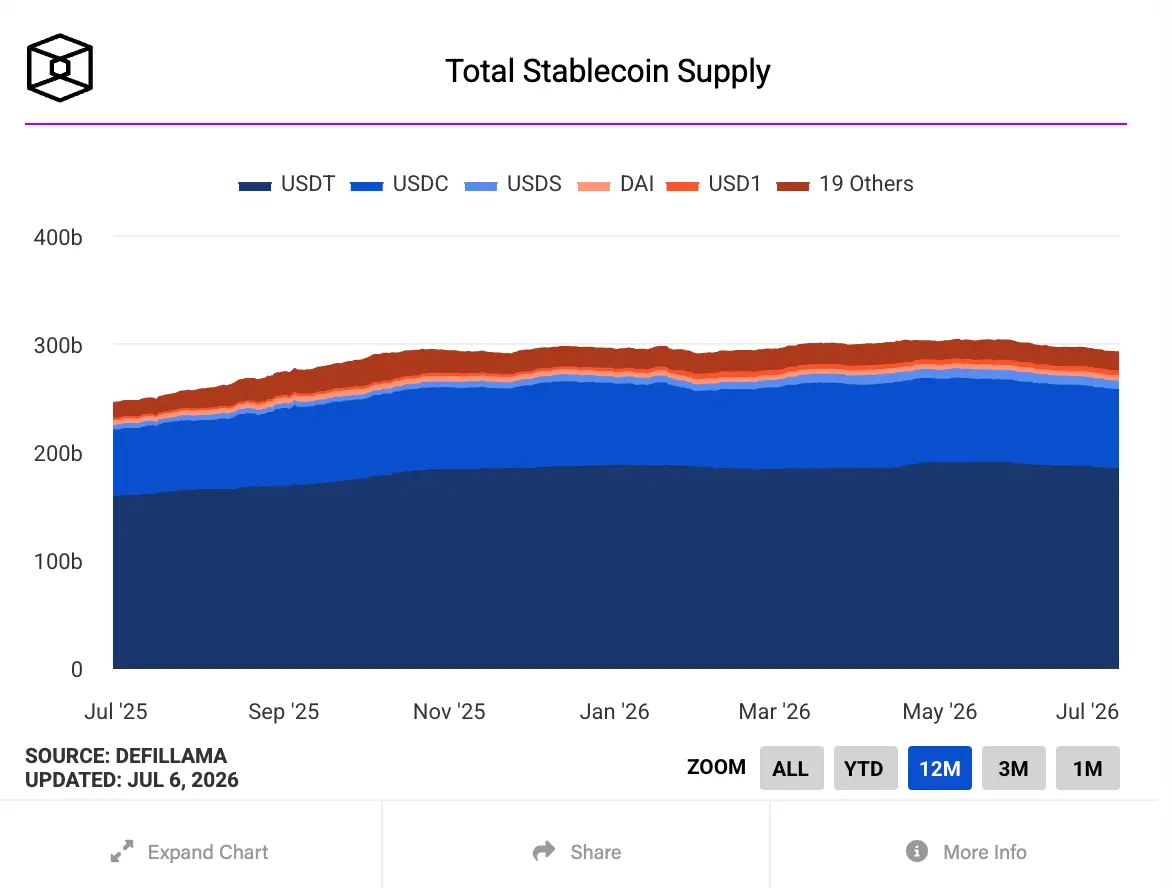

According to data from The Block's dashboard, the total market capitalization of USD-pegged stablecoins exceeds $291 billion, with Tether's USDT accounting for approximately $184.3 billion and Circle's USDC over $73 billion.

Furthermore, regarding OUSD's 'zero-fee minting and redemption' selling point, he believes market realities often force projects to adjust their approach; Circle handles it through contractual mechanisms rather than a blanket zero-fee policy. Regarding 'sharing revenue with everyone,' he bluntly stated that distributing all revenue is equivalent to 'starving the infrastructure,' leading to systemic underinvestment and preventing the platform from ever scaling up.

Additionally, there is his view on the 'alliance model.' Allaire believes consortium-type products have a historically poor track record in achieving scale, product-market fit, or even basic agility. 'A big group of big companies coming together, poor coordination, misaligned incentives, slow progress, and often, they all have their own agendas and 'starve' the consortium itself.' He also observed that when such alliances are formed, everyone is eager to put their logo on the list, endorse it, and loudly proclaim its openness, but in the end, each company's business units will still make optimal decisions for their clients.

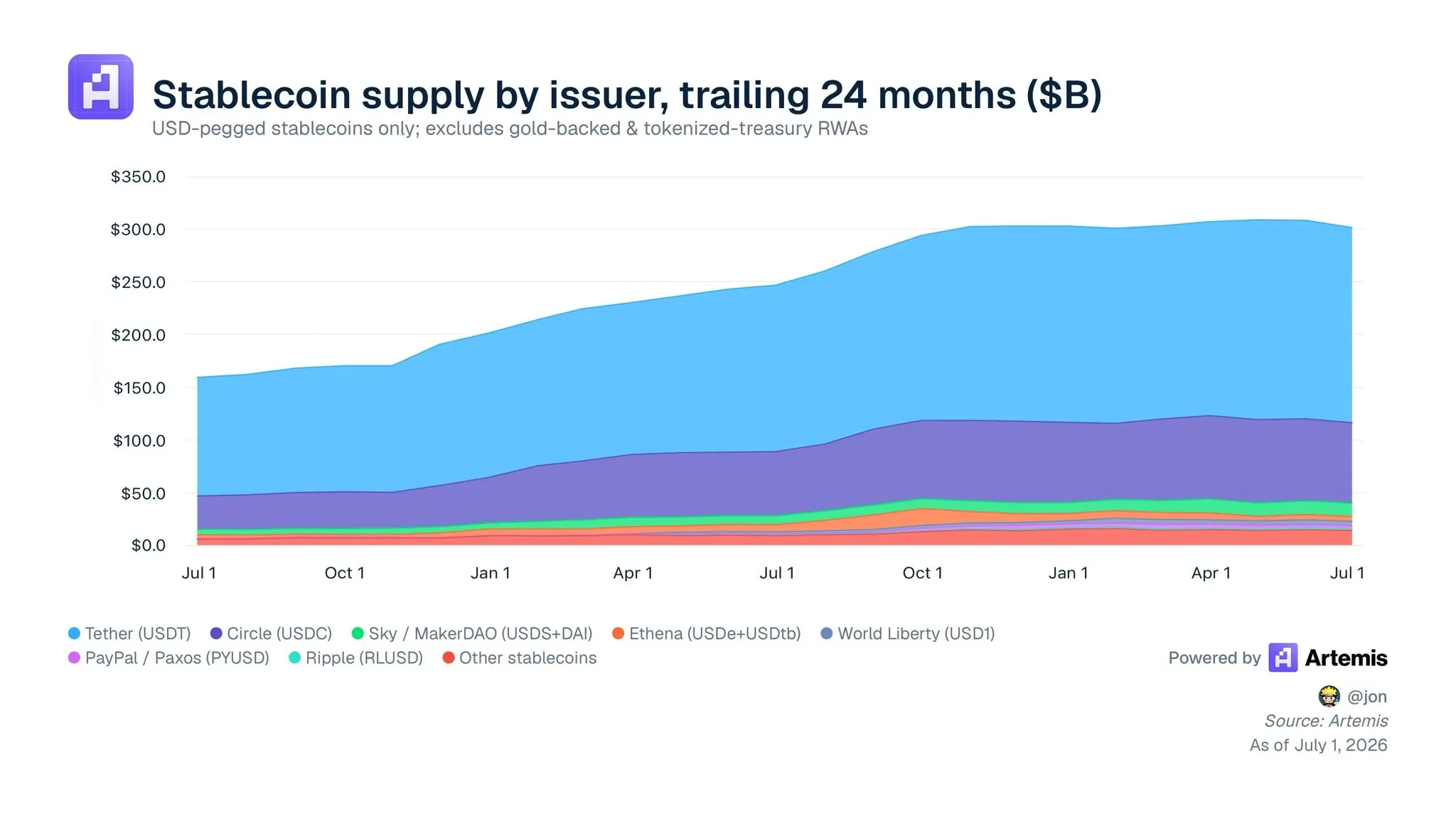

According to statistics from the third-party institution Artemis, as of July 2026, the total supply of USD stablecoins is approximately $3 trillion, with USDT around $1.8 trillion and USDC around $780 billion, together accounting for nearly 90%; all new entrant stablecoins combined total about $40 billion, just a tiny sliver at the bottom of the stacked chart. Allaire believes many stablecoins may have circulating supply, but most of it comes from promotions and incentives, with extremely limited real usage because liquidity and network utility cannot sustain them.

Conclusion

It can be said that the success of a stablecoin does not rely on assembling a group of alliance members for marketing purposes, but depends on whether it has real use cases and real users, including in specific scenarios such as B2B payments, merchant settlements, cross-border payroll, etc.

However, we cannot yet determine the final outcome for OUSD. It does have genuine heavyweight endorsements and a product model distinct from the existing market landscape, and it may not necessarily follow Libra's path. Yet, what this controversy reveals is a recurring issue in the crypto industry: a giant alliance can give a project immense momentum even before launch, but the positions of USDT and USDC are built upon real application scenarios in exchanges, DeFi, payments, and cross-border flows. Before achieving that, is OUSD merely issuing empty promises to the market? The market will provide its own answer.