作者:Frank,PANews

3月8日,Pump.fun累计收入突破10亿美元,是Solana上首个达到这一里程碑的平台,也稳坐MEME赛道最醒目的印钞机。但在热潮退去之后,问题已经不只是“谁赚得最多”,而是这些靠MEME起家的平台,如今到底还剩下多少生意。

沿着Pump.fun、GMGN、Four.meme、Axiom,以及Photon、BullX、BONK这些头部生态项目看下去,答案其实已经越来越清楚:MEME并没有消失,只是生意越来越向头部集中,链与链之间、平台与平台之间的分化也越来越明显。

Pump.fun:跨越牛熊的“绝对寡头”,上亿利润却难沉淀

如果说上一轮MEME热潮是一场昼夜不停的淘金潮,那么Pump.fun无疑是这座淘金镇里最赚钱的收费站。公开数据显示,截至2026年3月,Pump.fun累计总收入已经突破10亿美元。其中,2024年贡献了约3.21亿美元,2025年进一步放大到约6.64亿美元。2026年开始,MEME行业遭遇严重的滑坡,但Pump.fun的影响似乎不算太大,至今也仍有约9830万美元收入。

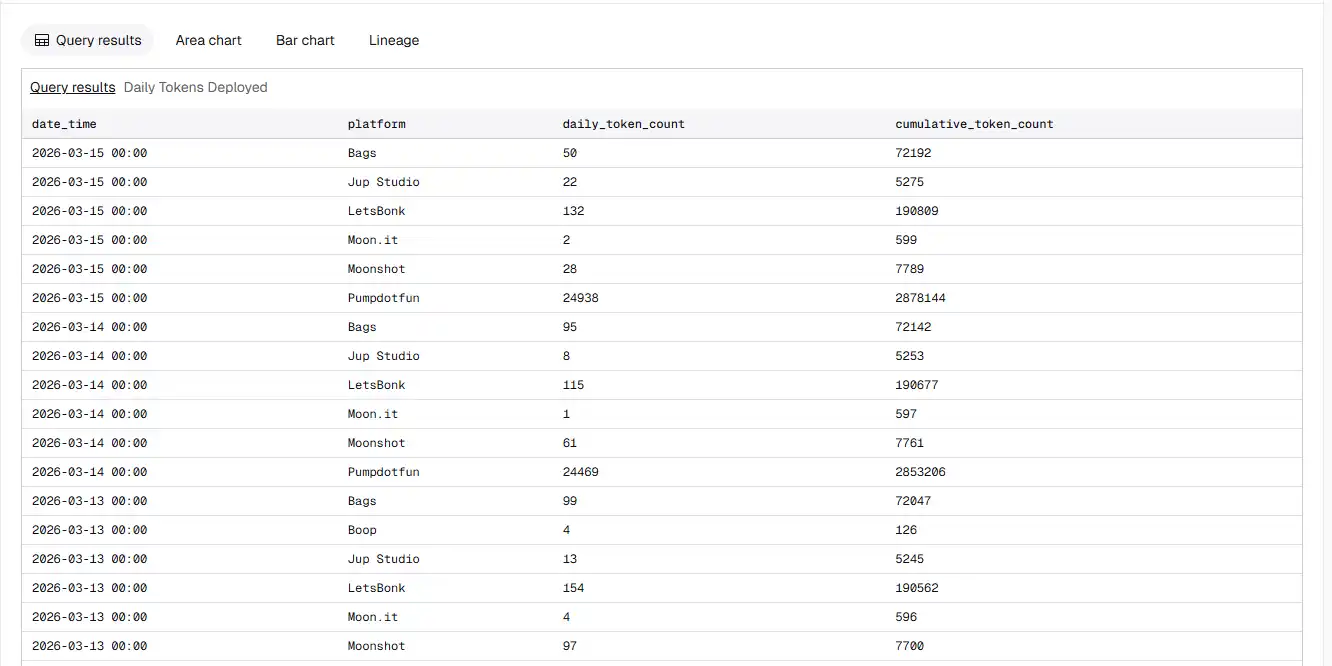

从市场格局上来看,Pump.fun在Solana生态的统治地位进一步得到了加强。以3月15日的数据为例,Pump.fun代币创建数量占比达到了99.1%,毕业代币比例为94.8,单日的交易量占比约为93%。当天,Pump.fun发币24938个,而LetsBonk只有132个,Bags为50个,Moonshot为28个,其他的代币发射平每日的数据量已经完全无法和Pump.fun进行竞争。

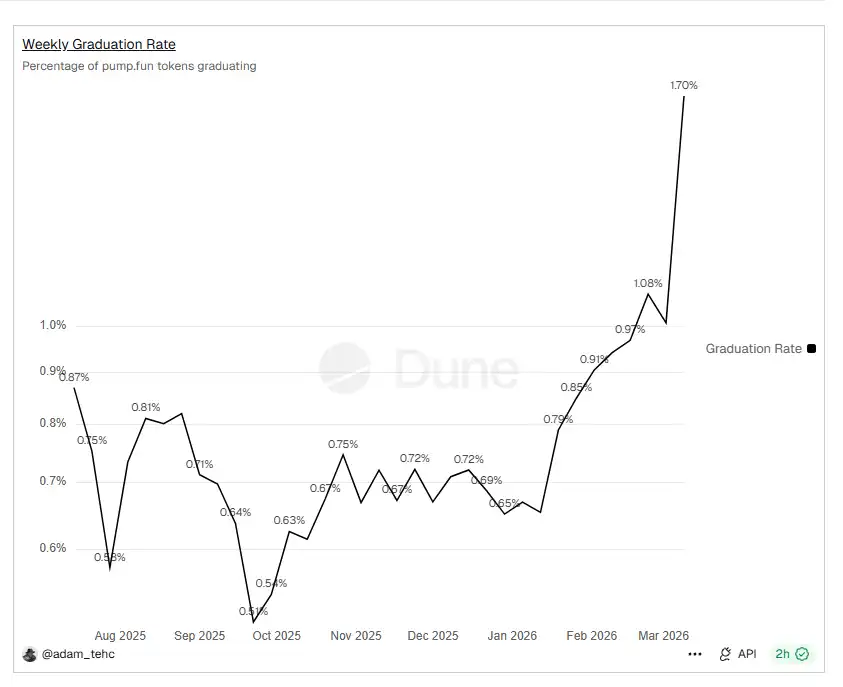

而回看Pump.fun本身的数据,也十分奇特的维持了一定的高水准,最近两周可见数据粗算,Pump.fun当前日均发币量约为2.97万个,日均活跃钱包约为15.77万个,日均成交额约为9365万美元,日均收入约为87万美元。与此同时,长期被视为平台软肋的毕业率也出现了修复迹象,最近甚至一度冲到1.70%左右。虽然这个短期高点还未能确定背后具体的原因,但Pump.fun的毕业效率确实在回暖。

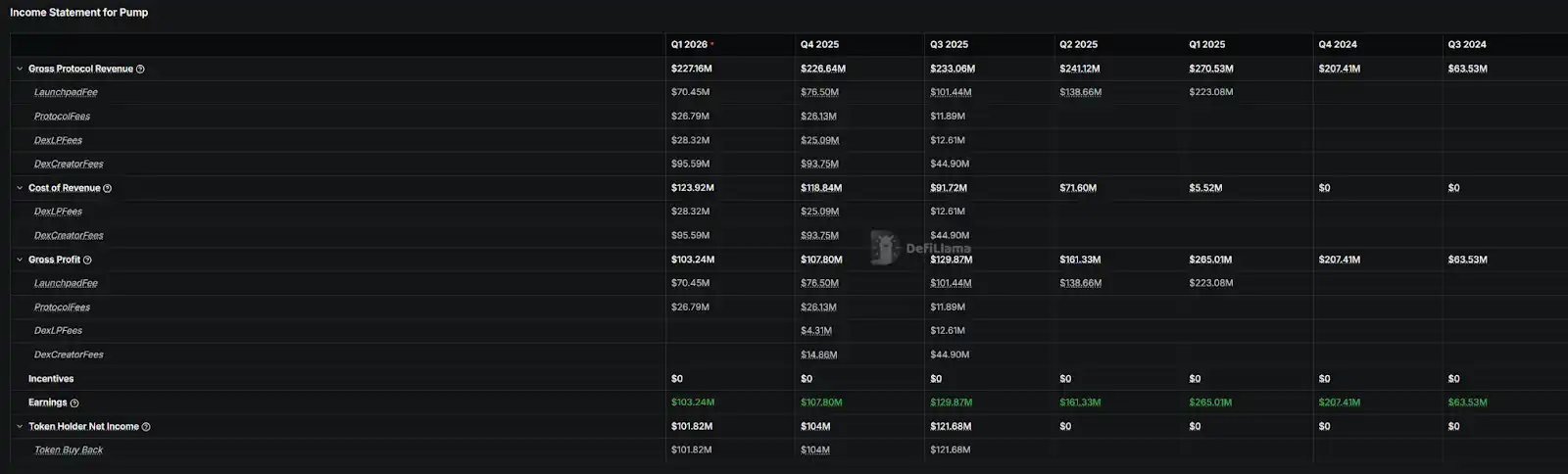

不过,虽然费用产生情况依旧稳健,但对Pump.fun来说,但并不意味着这些收入都能完整沉淀成协议利润。首先,是一多半的的费用都让渡给创作者和LP。其次,在创作者收入之外,剩余的收入也都用于代币回购。2026年第一季度,Pump.fun共产生费用达到2.27亿美元,其中1.23亿美元分给了创作者和LP,剩余的1亿美元也几乎全部用于代币回购。

但问题在于,回购并没有自动转化成币价上行,截至3月16日,PUMP价格约为0.002美元,较其历史高点0.0088美元仍低了约76.21%。这里更合理的解释是,回购只能起到托底和维持叙事的作用,却不足以逆转整个MEME板块估值压缩的趋势。换句话说,Pump.fun的现金流机器仍在高速运转,但市场已经不再愿意像上一轮热潮里那样,单纯因为“会赚钱”就给它更高的估值倍数。

总结一下,对Pump.fun来说,市场格局仍旧相对稳健,虽然整个meme币赛道迎来下滑,但死掉的基本是对手,反而让Pump.fun的统治力越来越强。如果这个市场再次能迎来爆发,Pump.fun可能将吸收到更大的红利。

GMGN:单季收入环比增长五倍,BSC成“流量新贵”

GMGN的收入在2026第一季度迎来了又一次爆发式增长。2026年第一季的总收入达到2531万美元,相比2025年第四季度的564万美元,增长接近5倍。这一季度收入也成为GMGN历史上第二高的单季度收入(仅低于2025年一季度的4081万美元)。

仔细拆分这个收入结构来看,主要得益于BSC链,2025年10月开始,GMGN在BSC链上的交易量开始明显超过Solana,到2026年这一趋势已经趋于稳定。截至目前,在GMGN上BSC链的交易占比已经接近Solana链的3倍。

从整体的交易量来看,2026年第一季度GMGN的用户活跃度与交易量都有了一定提升,不过这一提升幅度并不像收入变化所显示的那么高。因此,从这个角度来看,2026年的一季度的GMGN收入提升的确存在,但爆发式增长则很有可能是defilama的统计问题(2025年10月前BSC链的收入数据为空)。

不过,这种增长主要源于1月份的BSC链上MEME交易量激增,当月产生全链收入达到1634万美元,到2月这个数字降为518万美元,3月截至目前约为377万美元。今年一季度总体水平和2025年同期接近。

Four.meme:BSC上的“门面担当”,日收入仅为峰值零头

如果说Pump.fun几乎吃下了Solana发射平台的大部分流量,那么在BSC上,最接近类似角色的就是Four.meme。

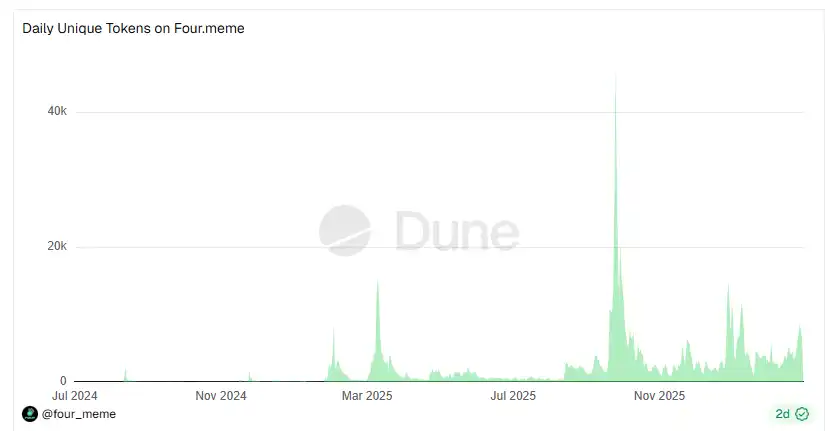

DeFiLlama数据显示,截至3月16日,Four.meme 2026年第一季度协议收入已经达到1600万美元,明显低于2025年第四季度的5424万美元,但从今年每月收入变化来看,仍有小幅回升。

按Dune追踪的最近10天的可见数据,Four.meme日均发币约4858个,日均用户约5749个,日均真正上线 DEX Pancake的代币只有25.7个,短期毕业率进一步压到0.53%左右。这些数据变化上来看,当前的Four.meme也正处在低位运行的状态,与2025年10月的最高日均422万美元收入相比,目前的收入已经降至20~30万美元水平。

作为对比,Pump.fun最近两周的数据估算,其日均发币量仍有约2.97万个,日均成交额约9365万美元。显然,作为Solana和BSC这两条链MEME币的主阵地,Four.meme和Pump.fun在规模和代币质量上有着较大差距,背后折射的也是两条链的MEME发展情况。

Axiom:告别高增长,持续陷入缩量泥潭

如果说GMGN在2026年第一季度的增长更像是吃到了BSC轮动的红利,那么Axiom的情况几乎相反。

按DeFiLlama数据显示,截至目前,协议在2026年第一季度的收入约为2903万美元,高于GMGN同期的2531万美元。

不过,Axiom当前的问题在于其业务处于一种持续下滑的状态。按DeFiLlama的季度收入数据,Axiom在2025年第二季度和第三季度的协议收入曾分别高达1.33亿美元和1.50亿美元,但到了2025年第四季度回落到6066万美元,而2026年第一季度截至目前为2903万美元。和去年最疯狂的阶段相比,业务体量已经明显收缩。这一点和GMGN进行对比后可以发现,虽然都是高峰后的下滑阶段,但GMGN收入时不时仍有阶段性反弹,而Axiom的状态却似乎未能再次振作。

对Axiom来说,它已经不再是一个单纯依赖MEME热潮爆发的工具,而更像是一台经历过多轮行情检验的成熟交易机器。相比还在讲增长弹性的GMGN,Axiom想象空间似乎正在萎缩。

Photon、BullX与BONK:潮水退去后的“掉队者”

相比仍有反弹的GMGN和仍维持头部规模的Axiom,Photon、BullX和BONKbot的收入曲线在2026年都更明显地进入了下行区间。

按DeFiLlama截至3月16日的数据,Photon累计收入约4.38亿美元,但单季度收入已经从2025年第一季度的1.228亿美元,依次下滑到第二季度的3231万美元、第三季度的1899万美元、第四季度的529万美元,2026年第一季度截至目前仅为452万美元,呈现出近乎阶梯式坠落的趋势。

BullX的累计收入约2.03亿美元,但同样出现快速收缩,单季度收入从2025年第一季度的8737万美元降到第二季度的1425万美元、第三季度的386万美元、第四季度的87.8万美元,2026年第一季度截至目前仅为49.1万美元。

BONKbot的下滑幅度相对没那么陡,但同样已经明显退潮。按DeFiLlama数据,其累计收入约9357万美元,2025年第一季度单季收入还有1261万美元,之后回落到第二季度的340万美元、第三季度的285万美元、第四季度的185万美元,2026年第一季度截至目前为184万美元。

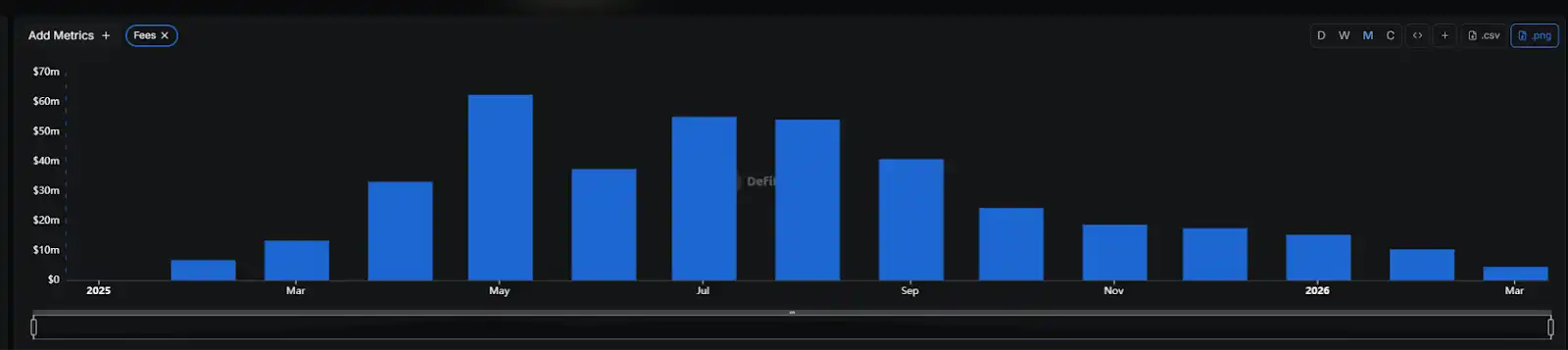

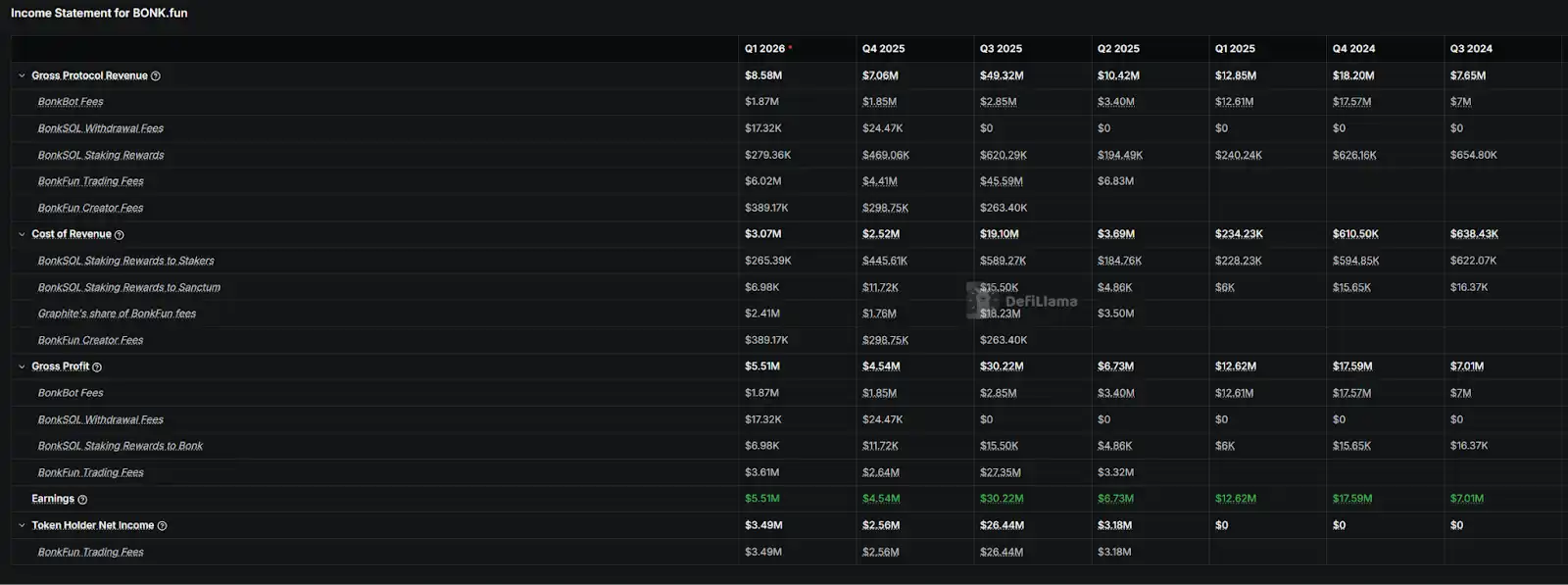

不过,BONK生态本身并没有同步熄火。截至目前,BONK.fun 2026年第一季度协议收入约851万美元,已经高于2025年第四季度的706万美元。其中,当前季度约有600万美元来自Bonk.Fun,约184万美元来自BonkBot。

纵观这场MEME币大逃杀,我们不难得出一个结论:MEME赛道并没有走向消亡,只是草莽竞争的时代已经彻底终结,洗牌速度远超所有人的想象。

潮退去之后,真正留下来的平台,不再只是跑得快的那批人,而是那些已经把发射、交易、流动性和收费链路做成完整闭环的玩家。如果下一轮MEME行情再次启动,最先吃到红利的,大概率也还是它们。