- Индекс страха и жадности снизился до 10 пунктов — уровень «экстремального страха».

- Текущее значение — одно из самых низких за последние девять месяцев.

- За месяц показатель упал на 18 пунктов.

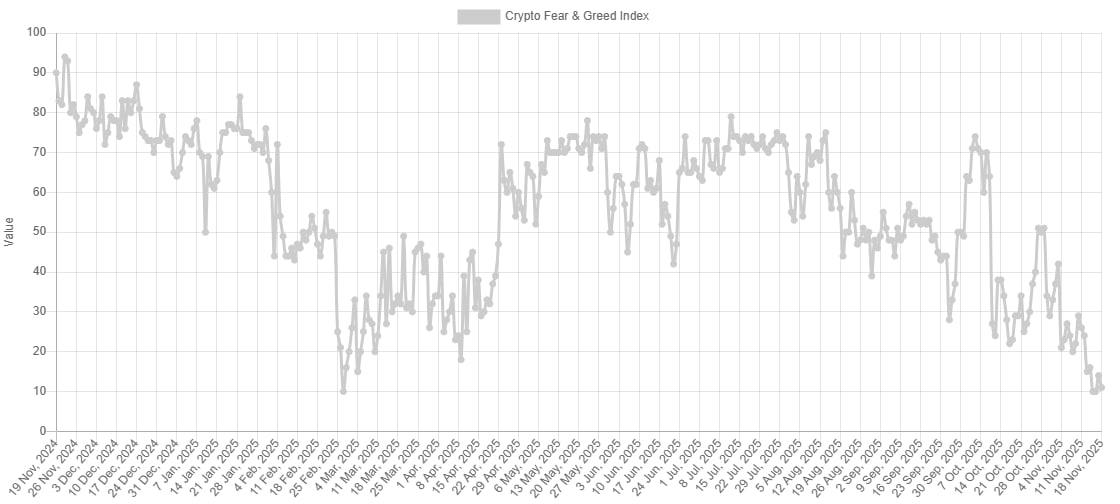

18 ноября 2025 года индекс страха и жадности опустился до 11 пунктов — это одно из самых низких значений за последние девять месяцев. Падение индикатора свидетельствует об «экстремальном страхе» трейдеров на рынке.

За последнюю неделю индекс снизился на 15 пунктов, а за месяц — на 18. Для сравнения: в начале октября он находился на уровне 74, что соответствовало «умеренному уровню жадности».

15 и 16 ноября показатель составлял 10 пунктов. Последний раз такие значения наблюдались в феврале 2025 года, когда биткоин обвалился ниже $80 000.

Отметим, сейчас падение показателя происходит на фоне обвала биткоина ниже отметки в $90 000.

В Alternative подчеркнули, что экстремальный страх может указывать на хорошую возможность для покупки активов, тогда как чрезмерная жадность, наоборот, свидетельствует о риске коррекции.

Примечательно, портал CoinMarketCap приводит несколько иные данные. Согласно им, по состоянию на 18 ноября 2025 года индекс страха и жадности находится на уровне около 15 пунктов.