来源:深潮TechFlow

原文链接:https://mp.weixin.qq.com/s/6KtPQ1hshCU6fK7NoRZ3JA

在香港 Bitcoin Asia 活动期间,币安创始人 CZ、特朗普之子 Eric Trump 相继登场……这场会议本应只属于精英和币圈大咖。

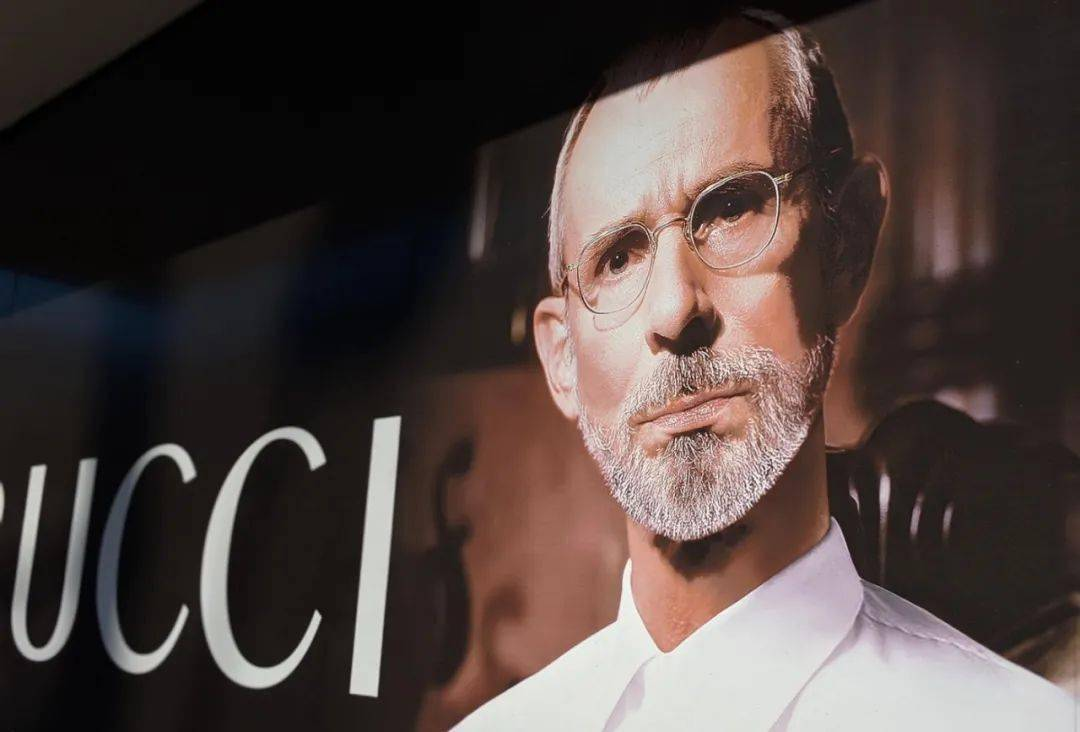

然而,真正抢镜的,却是一件白色 T 恤,上面印着四个汉字:“老外站台”。

穿着它的人,是一张西方面孔。

当他在人群中与赵长鹏并肩合影时,镜头下的问题扑面而来:

他是谁?“老外站台”又是一门怎样的生意?

老外在币圈

这位引人注目的老外名字叫 Dane,币圈 Agency 4am global 创始人。

从牛津大学计算机专业毕业后,一次旅行让他与中国结缘,此后一待就是十三年。用他的话来说:“如果我不喜欢这里,早就滚回去了。”

和众多中国大学毕业生一样,Dane 曾经也是一名北漂,在北京的科技与互联网公司做“洋牛马”,多年的生活不仅让他中文流利,更熟悉中国的人情世故,甚至迷上了《甄嬛传》《回家的诱惑》等电视剧。

2017 年底,ICO 带火加密货币大牛市,Dane 也正式踏入中文币圈。

所谓“老外站台”,是币圈里一种特殊的服务模式:为中国区块链项目提供外籍代表,以提升国际形象和可信度。在英文语境中,这类服务被称为 White Monkey。但在 Dane 看来,这远不止是一张“白人面孔”,而是一套包含国际化包装、资源对接与市场沟通的完整服务。

“很多人以为我们只做‘老外站台’的包装,但事实上我们是一个纯外籍团队,80%的客户来自欧美项目。”他说。

这门生意的起点,源于他 2018 年为中国公链做海外 BD 时亲自站台的经历。随着对行业的深入,Dane 意识到:中国项目资金充裕、技术不弱、交易所资源丰富,但缺乏的是国际形象、市场嗅觉和跨文化沟通能力。

加上国内对加密行业的监管长期收紧,自 2017 年禁 ICO、关交易所,到 2021 年全面叫停加密交易和挖矿,许多创始人更不愿抛头露面,于是“找一个外国专家来代表发声”成了刚需。

于是,“老外站台”的业务应运而生。Dane 回忆,在香港的一次大会上,就有不少中国项目主动找他寻求服务,“大概至少 50% 的中国项目方都有这样的需求”,甚至还有大型交易所邀请他出任 CEO。

“当时我觉得很荒唐,但深入研究后发现,这个需求其实合理。”

White Monkey

日光之下无新事。

十年前,在中国房地产行业最火热的年代,租赁“西方面孔”的服务就已盛行。《纽约时报》当时写道:“在偏远的建筑里塞满外国人面孔,哪怕只是一日,也足以证明这里‘国际化’。”

慕思床垫凭借一张英国模特的脸,编织出“源自 1868 年法国设计师 DeRucci”的故事,把千元床垫卖到上万元。直到上市前夕,证监会才揭开底牌:这不过是一份 2009 年的肖像权买卖协议,所谓法国血统子虚乌有。

这种包装在西方有个固定称呼:White Monkey。

这种行业存在了半个世纪,只要是白人,几乎不需要任何技能,就能出现在舞台、办公室或广告中,扮演“外企高管”“公司发言人”“洋专家”的角色。

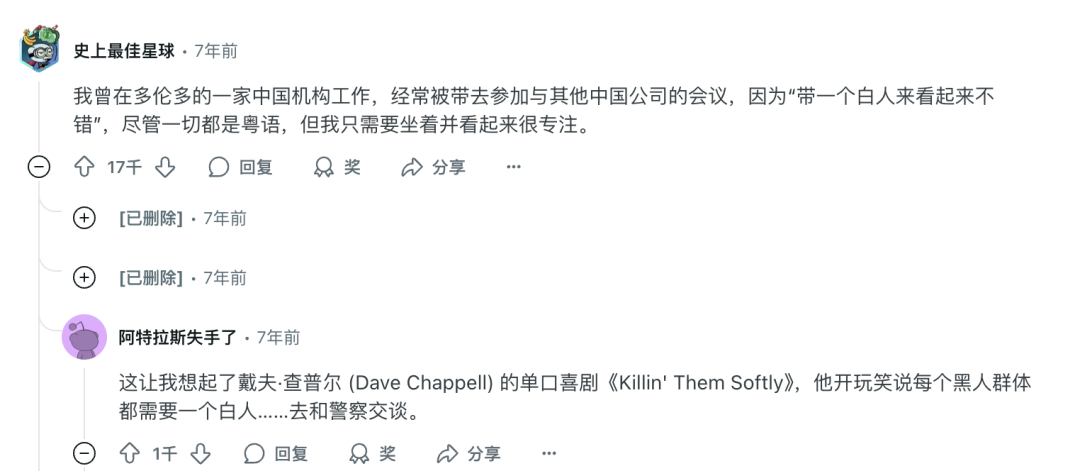

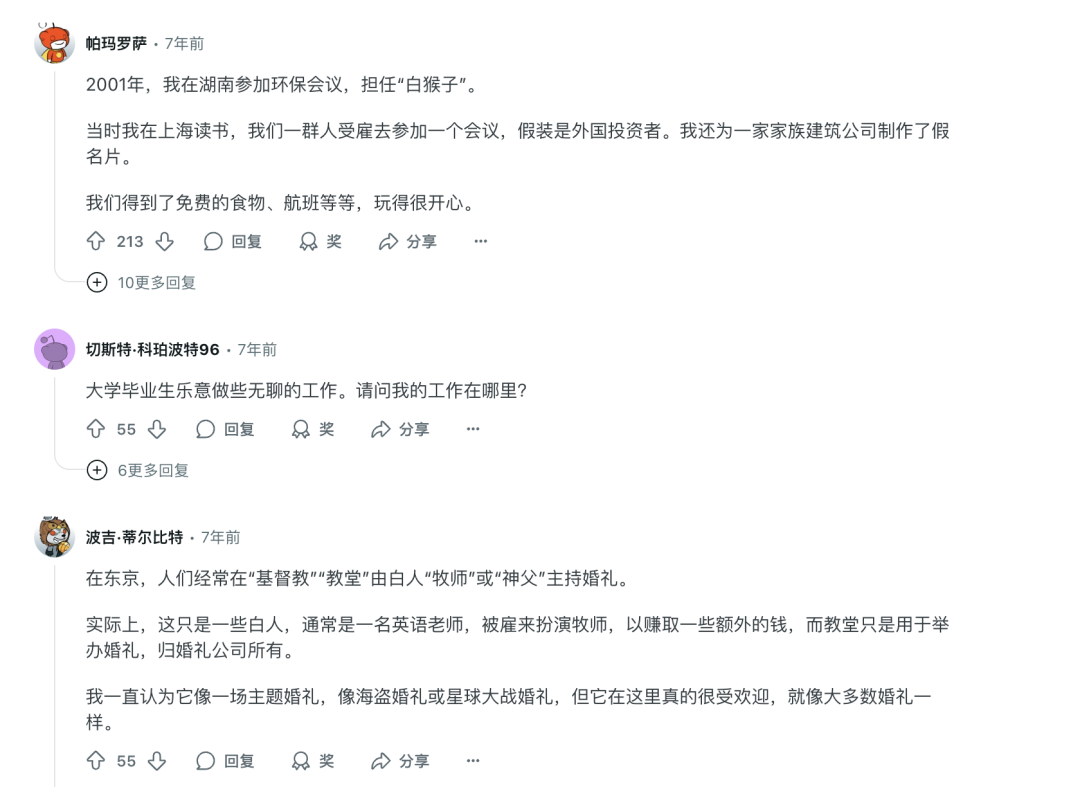

在论坛 Reddit 上,一众老外交流曾经在东亚做 White Monkey 的经历:

正如《The Spectator》在 2022 年报道中所说:“白人男女甚至可以被雇佣为办公室职员,他们没有实际职责,只是为了营造一种更精致的国际氛围。”

这种“氛围经济”在加密行业同样盛行。

2017 年 ICO 大牛市,项目方只需一份白皮书就能讲故事募资。Alex 所在的团队不仅代写白皮书,还能“找老外演员”。“那时在‘北外’、‘北二外’门口,随便找个白人留学生来当 CEO,就能轻松募资上万个以太坊”,他至今仍感慨那段岁月的疯狂。

甚至出现过,华人团队聘请上海夜场的白人男模为 CEO,结果男模反客为主,以 DAO 之名抢夺了项目控制权,将原团队踢出局,此后在中东资本的帮助下,该项目市值一度高达 70 亿美元。

不仅是素人。

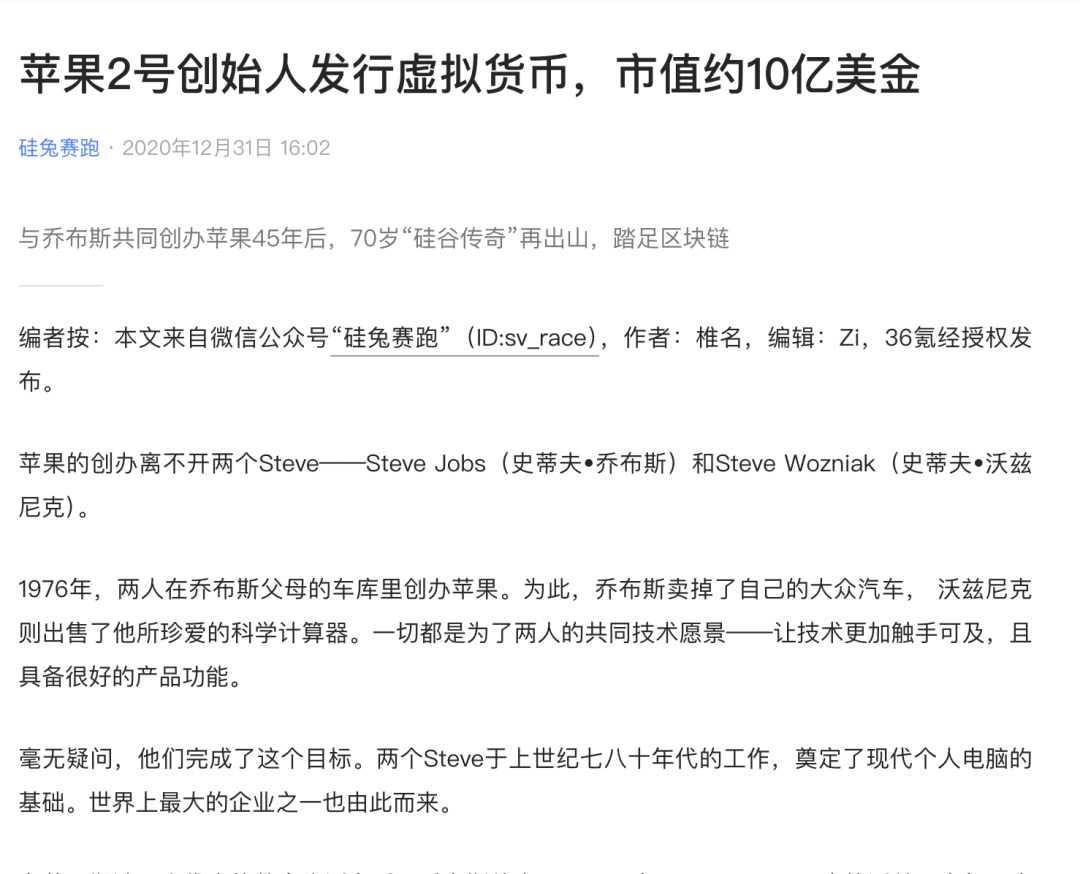

2020 年,苹果公司联合创始人史蒂夫·沃兹尼亚克(Steve Wozniak) 曾受雇于某华人团队,发行加密货币 WOZX,市值一度高达 10 亿美元,如今市值仅为 100 万美元,几乎归零。

2025 年,塞尔维亚前总统鲍里斯·塔迪奇在 X 平台发文确认其为某代币基金会的 CEO,据知情人士披露,该代币幕后团队位于香港。

阿根廷总统米莱今年 2 月因在社交媒体转发 $LIBRA 代币宣传而深陷丑闻,随后紧急撇清关系,《经济学人》将此称为他任期内的“第一起大丑闻”。

在 Alex 看来,“老外站台”也在不断迭代升级。

最初只是拍照、录视频,糊弄一下就行,但随着 ICO 泡沫破裂,散户不再那么好骗,站台模式开始进入 2.0 阶段:真正的大老板依旧是华人,但 CEO 等高管位置由老外担任。这些人不再是纯粹的演员,至少具备演讲、BD(商务拓展)等能力,可以带来更强的市场背书,“中西搭配,大家一起赚钱”。

至于原因,Alex 直言,最重要的还是监管和合规压力迫使创始人隐身,另一方面则是散户的滤镜。

在中日韩,民众普遍认为欧美面孔意味着“国际化”,而本土项目则容易被打上“资金盘”“土狗”标签。对很多项目而言,没有体面的国际形象,就意味着很难获得 VC 和交易所投资,也难以获得散户认可。

此种滤镜下,Dane 见过不少荒唐场景:疫情期间,很多资金盘和土狗项目会随便找一个留学生当 CEO,到处巡回路演。下一个城市,再换一个新“老外”接班。

“一个城市一个 CEO,荒唐至极。如果项目有干货,就该找一个真正有干货的老外。”他直言。

真正深入业务之后,Dane 才发现“老外站台”远非请一个洋人拍照那么简单。语言障碍、文化差异、时差问题、关系维护……比起单纯套用头像和代言,更需要专业中间人持续撮合与管理,才能撑得起所谓的国际化。

当中介不容易

在币圈做“老外中间人”,Dane 直言挑战远比想象大。语言障碍、文化差异和时差,让中国团队与外国人才之间很难直接理解彼此。

第一步永远是“需求匹配”。一些项目希望找到熟悉 DeFi、RWA 的专家,有的则要求候选人常驻某个国家或城市。Dane 必须在双方条件之间不断斡旋。“有些要求合理,有些则天方夜谭——条件太多时,我们真的没办法。”

三年来,Dane 跑遍全球会议,积累了庞大的人脉。大约八成的情况能找到合适人选,但剩下两成往往只能遗憾收场。理论上,他可以只做“猎头”,介绍完人就抽身离场,但现实中走得通的项目不到 5%。对 95% 的项目而言,中间人必须同时扮演翻译、协调者、甚至活动保姆的角色。

“如果不在中间持续做这种沟通,双方很快就会出现矛盾,甚至不愿继续合作。文化差异是最大的挑战。”

除了撮合,更关键的是关系维护。Dane 会定期和欧美人才聊天、开户,或者在大会现场见面叙旧。“很多欧美从业者并不缺钱,真正重要的是关系感。老外站台的服务,核心就是维系长期信任。”

然而,这门生意也衍生出乱象。有人把一个 3000USD/月的“西方人才”转手炒到上万,三倍差价让 Dane 摇头不已:“我觉得他们迟早会砸牌子,但不能否认的是,这样的人有很多。”

一件衣服,四个汉字,让 Dane 获得了很多关注,也收到了不少“粗暴直接、明目张胆”的评价。作为团队里唯一懂中文的人,他的员工甚至看不懂“老外站台”的含义。

但不可否认的是,英语语境中被称为 White Monkey 的这项业务确实需求不小,他也曾经帮助中国项目顺利获得 500 万美元的融资。相比措辞上的冒犯,他更在意的是获得市场的关注。

展望未来,他甚至打算将业务拓展到 Web2 上市公司,“在传统行业,这种需求只会更大。”