原文作者:Franklin Templeton Digital Assets

原文编译:Alex Liu,Foresight News

对区块链而言,质押奖励是成本吗?

在加密货币社区中,关于质押奖励是否应被视为网络成本的问题一直存在争议,因为这些代币激励措施增加了代币总供应量(从而稀释了被动持有者)。这一争议进一步复杂化,因为各方对「成本」的定义并不统一,存在对「成本」的不同理解。这篇研究文章的目的是从我们的角度定义质押奖励是否是分布式网络的成本。

什么是质押奖励?

质押奖励是提供给那些选择在权益证明(PoS)网络上质押其代币的代币持有者的。这个过程涉及锁仓数字资产,以帮助验证交易并保护区块链网络。这些质押的代币作为验证者的抵押品,承诺以诚实的方式行事。如果验证了欺诈性交易,将会失去(slashing)这部分抵押品。这些抵押品是以区块链的原生资产计价的(以太坊使用 ETH,Solana 使用 SOL)。

质押奖励导致代币供应量的通货膨胀,因为奖励是通过新铸造的代币分发给诚实的验证者的,验证者质押其资本以此保障网络安全。例如,截至 2024 年 9 月 18 日,ETH 和 SOL 的年化通货膨胀率分别约为 0.8% 和 5.0% ,这完全是由质押奖励产生的。

争议:

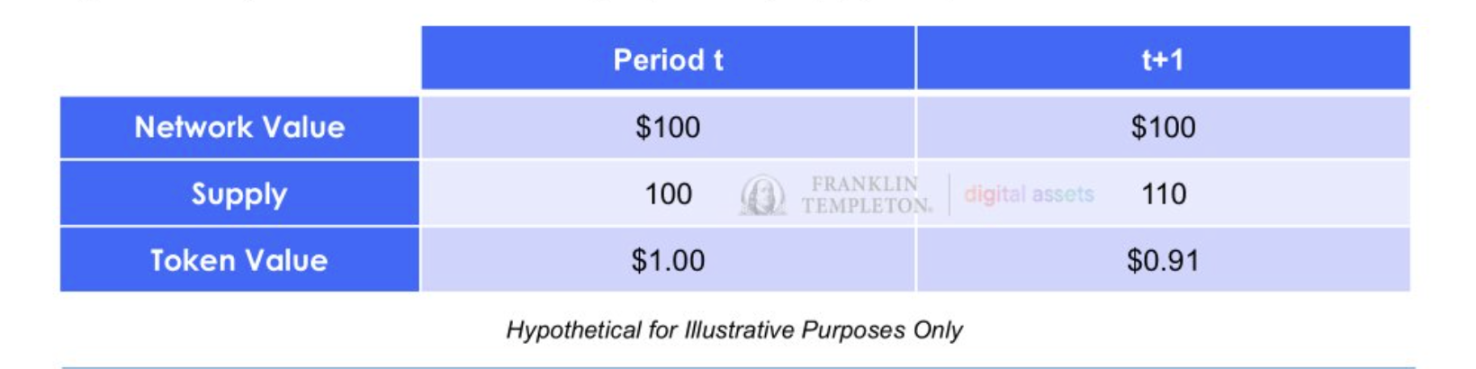

从一个角度看,网络价值受代币数影响,质押奖励引入了新的供应量,将相同的价值分配给更多的代币,从而降低了代币价格。相反,另一种观点认为网络价值是以市值定义的,因此质押奖励并不是网络的成本,因为它们纯粹是非质押者向质押者的价值转移。我们的观点是,这两种看法都是正确的,只是从不同的角度来看待问题。质押奖励对代币价格来说是一种成本,因为供应量在增加;但它并不是网络价值的成本,因为代币供应影响的是代币的总数,而不是总价值。下表说明了从 t 期到 t+ 1 期供应量变化对代币价值的假设动态:

我们认为,关键点在于,尽管整个网络价值保持不变,但代币供应量的增加导致每个代币的价值下降。我们不认为增加供应会改变网络价值。而如果认为代币价值不会因供应量增加而受到影响,就像是相信钱会从天上掉下来一样。

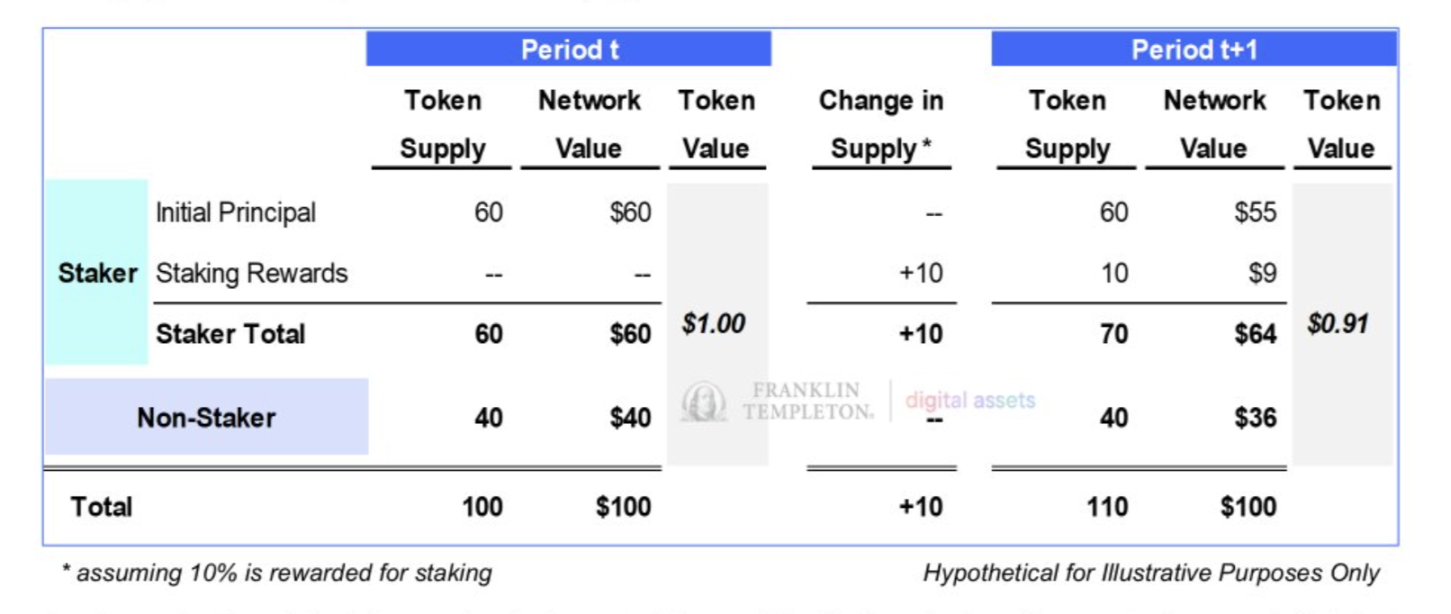

从质押奖励只是非质押者向质押者的价值转移这一角度来看,我们在下图中进一步阐述了这一点。图中展示了 PoS 网络中从 t 期到 t+ 1 期代币价格和价值转移的过程。我们假设 60% 的代币供应被质押,通货膨胀率为 10% (通过质押奖励)。可以看到,网络价值保持不变,因为在这两个时期中唯一重要的变量是代币供应量。

如表所示,代币价值受到了约 9% 的稀释,进一步证明了我们认为质押不会影响网络价值,但会稀释代币的价值。非质押者的网络价值变化与整体代币价值的变化百分比相同。对于质押者来说,质押的初始本金与非质押者一样被稀释;然而,质押者通过质押奖励获得的收益多于因稀释所造成的损失。投资者可以通过链上数据或第三方质押指数(如 CESR 指数 —— 综合以太坊质押收益率)来监控这些奖励的质押收益率,该指数跟踪以太坊链上的此类收益。

那么,质押奖励是否是网络的成本?我们认为,质押奖励并不是网络整体价值的成本。然而,质押奖励确实代表着在当前时刻代币持有者的的一种支出。